The MBW Review is where we aim our microscope towards some of the music biz’s biggest recent goings-on. This time, we get our calculator out and run IFPI‘s latest numbers for the global record industry. The MBW Review is supported by Instrumental.

IFPI, the organization that represents the recorded music industry worldwide, published its annual Global Music Report (GMR) this week – spilling the beans on the official trade revenues for the recorded music industry in 2020. (That’s trade revenues, meaning the money that works its way back to record labels and distributors, and then artists.)

In spite of the pandemic, the headline numbers were upbeat: global recorded music revenues reached $21.6 billion last year, representing an increase of 7.4% versus 2019.

This was the record industry’s sixth consecutive year of growth, and its largest annual haul since 2002 ($22.1bn).

The 2020 uptick was driven primarily by streaming and, particularly, by paid audio subscription streaming revenues, which according to IFPI, increased by 18.5% YoY.

However, behind the celebrations of a growing industry in a pandemic year, you might just hear some record industry grumbles about that old chestnut, Average Revenue Per User (ARPU).

Here, MBW takes a stab at estimating what’s happening to perhaps the most contentious streaming data point in the modern record business.

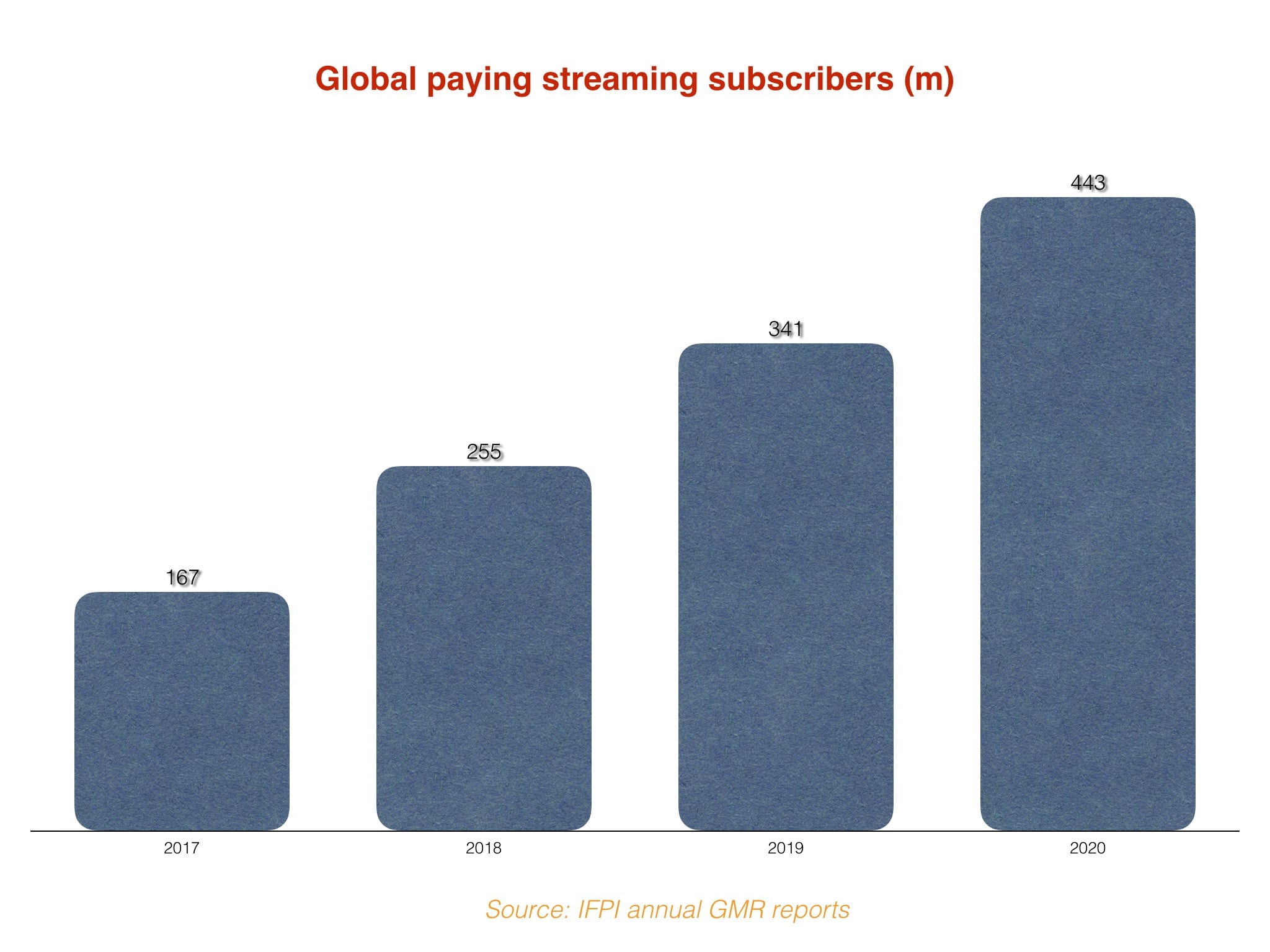

Need to Know Fact #1: The number of global streaming subscribers grew faster in 2020 than it did in 2019

We start off with a very promising trend: IFPI data in the latest GMR shows that there were 443m users of paid subscription music streaming accounts at the end of 2020.

That was up from 341m at the close of 2019 (as previously reported by IFPI), representing a YoY climb of 102m subscribers.

In turn, this 102m rise was a bigger jump than that seen in 2019 itself, when the equivalent YoY increase stood at +86m (also as previously reported by IFPI).

Need to Know Fact #2: Streaming subscription revenue did not grow faster in 2020 than it did in 2019

The preview version of the IFPIs’ new Global Music Report contains a segment of the full, premium book – which is available for a fee through this link. (MBW’s advice: If you’re commercially incentivized to monitor music business trends, and have a hefty stack of corporate dollars to play with, it’s kind of an essential tome.)

The preview GMR doesn’t tell us precisely how much audio streaming revenue was pulled in by the record business during 2020… but it tells us enough to figure it out.

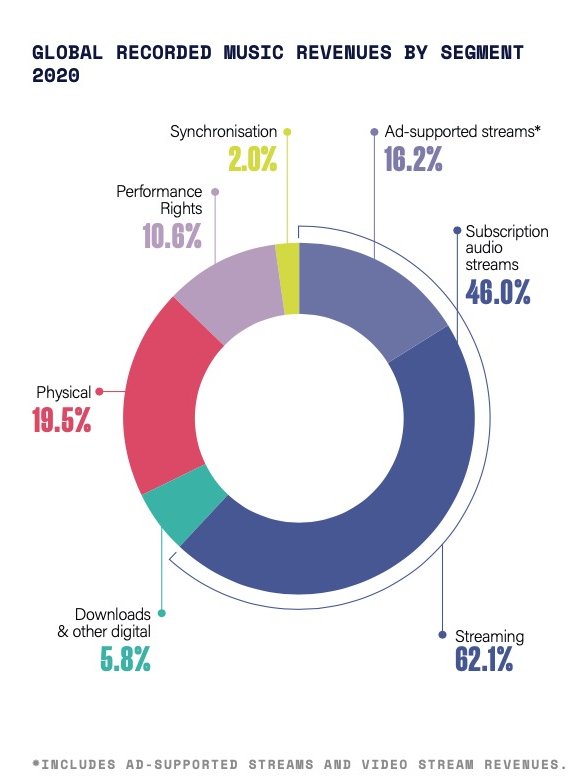

According to IFPI’s breakdown (see inset), audio subscription streaming was responsible for 46.0% of the $21.6 billion total revenue generated by the worldwide record industry last year.

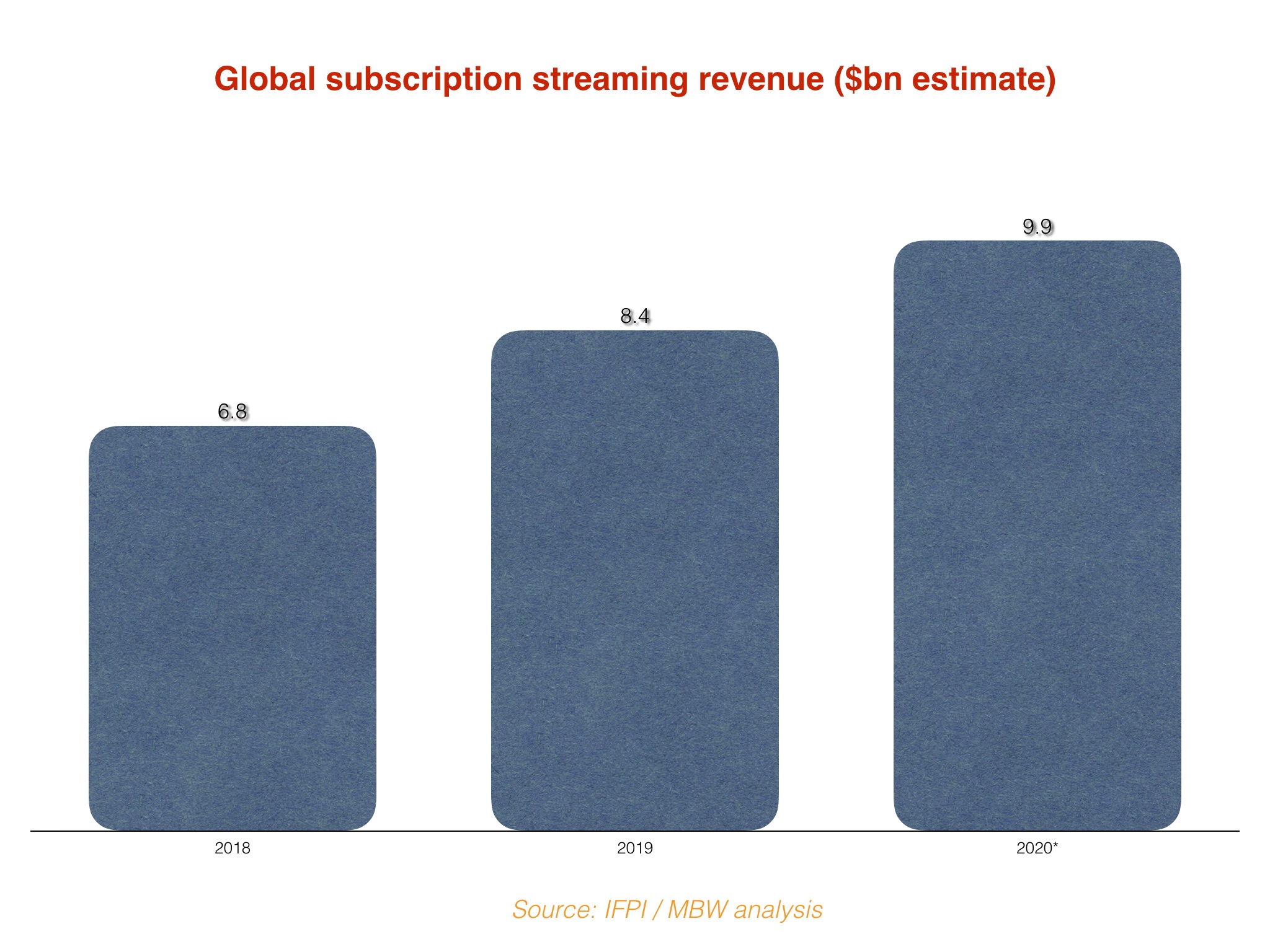

That means approximately $9.94bn in audio subscription revenue was pulled in by the business during 2020. We also know, thanks to the GMR, that this ≈$9.94bn figure was up 18.5% YoY when compared to 2019’s haul.

In turn, this means we can also figure out the approximate global audio subscription revenue figure for 2019 – likely revised since IFPI’s last report – which is $8.39bn.

Nearly there!

Need to Know Fact #3: Streaming subscription ARPU dropped by somewhere around 8.8% YoY in 2020

The above calculations give us enough data to run some important ARPU calculations on subscription streaming worldwide. (Again, remember, this concerns trade revenues – so the money paid out per user by the likes of Spotify to recorded music rightsholders, rather than the amount paid to Spotify by each user).

Here goes:

In 2020, the music industry was receiving approximately $22.44 per audio streaming subscriber worldwide annually – or $1.87 per month. (The math: $9.94bn / 443m people / 12 months.)

In 2019, the music industry was receiving approximately $24.60 per audio streaming subscriber worldwide annually – or $2.05 per month. (The math: $8.39bn / 341m people / 12 months.)

Therefore, according to MBW’s estimates based on IFPI data, global subscription streaming trade annual ARPU fell by just over $2 per head in 2020, or by 8.8%.

The driving factors behind the ARPU decline we’ve calculated here are the same as ever, most notably: (i) Streaming subscriptions growing in countries with a low USD-equivalent subscription cost – especially so-called emerging markets; and (ii) The continued prevalence of discounted subscription deals, Family Plans, Student Deals and telco bundles – all of which bring down the average per-subscriber spend on streaming subscriptions.

It will be interesting to see how Spotify’s recent expansion into over 80 new countries affects point (i) here as 2021 plays out. It certainly seems likely that Apple Music‘s own expansion into 52 new markets in April 2020 would have affected last year’s industry ARPU numbers.

The erosion of music industry ARPU – as we’ve noted recently – leads on to a natural discussion about streaming companies and whether they should now be charging higher prices for subscriptions in mature markets like the UK and US.

If companies like Spotify could successfully adjust prices in these markets upwards, it would arrest the fall in ARPU we’ve laid out here. But it’s not without risk: don’t forget that the number of global subscribers grew faster in 2020 than it did in 2019. Would a price rise scare off new consumers and slow this growth right down?

Expect this debate to roll on. And on. And on.

(A footnote: One crucial number within our calculations – the total number of streaming subscribers in 2019, which we have down at 341m – could have moved up or down slightly if IFPI has now restated the figure it originally published in last year’s GMR. However, this wouldn’t make a material difference to our estimated ARPU % decline.)