An interesting stat: BMG spent slightly more on music catalog acquisitions last year than Universal Music Group – the largest music rights company on earth.

That fact tumbled out of BMG’s impressive FY 2022 results, published in late March, which showed that the Bertelsmann-owned firm splashed EUR €380 million (USD $400m) to buy 45 music catalogs in the 12 months. (UMG spent €359m, or around $378m, on catalog M&A in the same period.)

If that shows the level of ambition for BMG in 2023, it’s a perspective only compounded by the company’s recent financial performance.

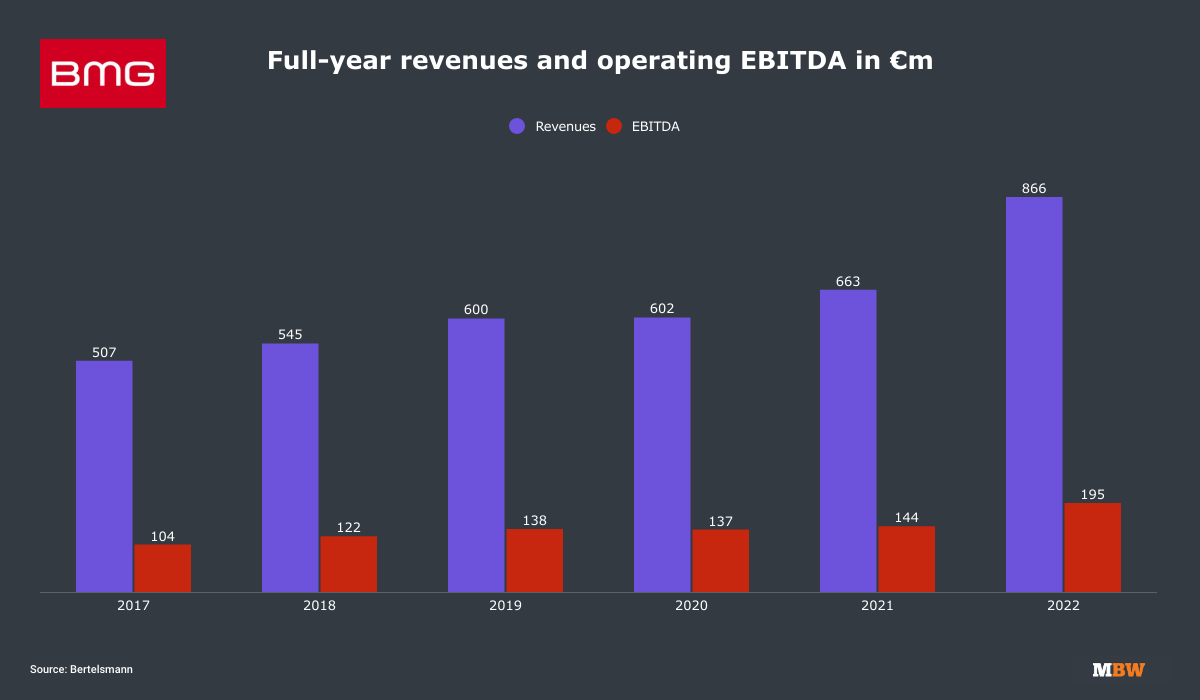

In 2022, BMG generated €866 million ($911m) in total revenues, up 30.6% YoY, as its operating EBITDA rose by over €50 million (+35.4%) YoY to reach €195 million ($205m).

And just last week, Bertelsmann delivered a Q1 2023 update in which it said that BMG “continued its strong growth” in the quarter.

A billion-dollar annual revenue milestone looks firmly on the cards for the music company this year.

We shouldn’t make the mistake of attributing sole causality for these numbers to BMG’s aggressive acquisition policy: The firm says less than 5% of its 2022 revenues came as a result of its past two-year acquisition spree.

Adding intrigue to the BMG growth story: At the close of this year, as confirmed in January, the firm’s long-term CEO, Hartwig Masuch, will step down from the role. He will be succeeded by BMG’s current CFO, Thomas Coesfeld.

MBW sat down with both Coesfeld and Masuch to ask what’s been driving BMG’s growth – and how it can keep it up in the challenging macroeconomic environment of 2023…

There’s a popular narrative that suggests, as streaming growth matures, major music companies are going to grow their revenues by high single-digit percentages annually. Yet amongst the ‘mini-major’ set of companies in music rights, something different is happening: BMG grew by 30.6% in 2022; Believe grew by over 30%; HYBE grew by over 40%. Obviously, you’re working off smaller revenue comps than the majors, but it’s still an interesting trend. What’s your take?

Thomas Coesfeld: People should be in no doubt. The shape of the music market is changing fundamentally. The music industry has never treated artists and songwriters as customers before. Once artists and songwriters have experienced more innovative approaches to market – how they are treated, the services they receive – there’s no going back.

We have set our course, a relentless and granular drive to incrementally improve our service to artists. Some people in the industry might want to return to the olden days, but artists don’t. The floodgates are now open.

“Some people in the industry might want to return to the olden days, but artists don’t. The floodgates are now open.”

Thomas Coesfeld

Hartwig Masuch: I see a healthy market with increasing fragmentation. The question is: do you want to be a hostage to that fragmentation by focusing on frontline signings, or do you focus on a proven body of work that can’t be taken away or fragmented?

When you watch music companies right now, one way or another, that discussion plays a massive role in who’s showing signs of vitality and who’s showing signs of stagnation.

In a BMG infographic sent to staff and clients in March, you pointed out that BMG now boasts a 99.7% auto-match rate of registrations, with 99% of royalties fully accounted within the 2022 period. Why are these technical issues important to you?

Coesfeld: BMG has been built on a different mindset and a different approach – an approach we’ve nailed down to fairness, transparency, and service. That’s not just lip service: The way we construct artist contracts and terms, for example, is really different.

Translating that to the streaming age implies that we have to invest more and more in technology that enables the capabilities to give artists and songwriters what they need. What that means is we are faster at processing [royalties] and the money they receive, we are more accurate in processing and distributing royalties.

We will keep building on our investments in technology and IT spending to provide the best service available.

Is there any advantage to the private ownership structure of BMG – fully owned by Bertelsmann – versus, for example, being publicly traded?

Coesfeld: Obviously, in light of the current turmoil of banks falling apart and interest rate changes, there has been a lot of uncertainty in the market of music rights acquisitions.

For us [under Bertelsmann], we have much more strength and stability, more conviction, which is long-term orientated. That means our balance sheet can be much more competitive than those who are purely financially motivated, because we are a fully-fledged music company. That enables us to be more long-term orientated and to move faster.

I’ll give you an example: We made a decision on an investment on Friday, and the money was out to the seller yesterday [MBW’s interview with Masuch and Coesfeld took place on a Thursday].

You spent more on catalog acquisitions in 2022 than even Universal Music Group. What does that tell us about BMG and your commitment to M&A amid a bumpy time, as Thomas points out, economically?

Masuch: Let’s face it: if you’re the market-leader you don’t need to invest so much to build your catalog. If you look at the body of work the majors have, if they’d have focused much earlier on maximizing the relevance of their catalogs versus building zero-EBITDA-producing, huge-revenue labels, their numbers would look great from a dynamic perspective. I think that’s now dawning on them.

“Universal, in particular, has so much amazing catalog in their vault, that with the exception of absolute iconic artists like Sting, maybe they don’t feel the need to be in every catalog auction at every price. We’re in a different place.”

Hartwig Masuch

Lucian [Grainge] is the smartest guy in the room, so it can’t be lost on him that while it’s nice to dominate the Top 50 of the Billboard chart, those frontline stars come at a high cost. I think you’re seeing a subtle retreat from frontline spending at the majors. And Universal, in particular, has so much amazing catalog in their vault, that with the exception of absolute iconic artists like Sting, maybe they don’t feel the need to be in every catalog auction at every price.

We’re in a different place; at the end of the day, to maintain our ability to keep growing and investing in our global operation, we need to scale up. We can’t sit back.

Spending over $400 million on music rights in 2022 shows a belief in the long-term value of these assets.

Coesfeld: Yes. What happened in the course of 2022, is obviously this big shift in the interest rate environment. It was sudden; faster than everybody had anticipated. So financial players who’d been making cost of capital arbitrage from investing debt into music woke up to the fact that it wouldn’t be enough just to do the financial engineering [and not actively ‘work’ catalog to maximize its value].

“when [some] investors slowed down or stopped their investing in music, it was time for us to double down.”

Thomas Coesfeld

I think there is more understanding now of what’s needed to unlock the true value of music from a cultural standpoint, an artistic standpoint. But also people now recognize where the levers are to really drive monetization, especially in emerging platforms outside of traditional streaming.

Many financial investors have woken up to these factors in the last year. And when these investors slowed down or stopped their investing in music, it was time for us to double down.

Obviously, I want to ask Hartwig about ‘hits’ – his favorite subject! BMG’s 2022 numbers happened despite you not having a single or album in the respective annual Top 50 charts in both the US and UK. What can we glean from that?

Masuch: The more fundamental question: why do so many people still believe in the necessity of having incredibly large infrastructure and investment just to have chart hits?

Yes, we focus our resources mainly on known quantities which were the hits of 10 or 15 years ago. But if everybody sees what we see – that the momentary income relevance of new chart repertoire is becoming less relevant in terms of the overall industry – why in the hell dedicate all those resources to it?

“If everybody sees what we see – that the momentary income relevance of new chart repertoire is becoming less relevant in terms of the overall industry – why in the hell dedicate all those resources to having chart hits?”

Hartwig Masuch

To a large degree, the charts you mention are engineered by whoever has the biggest financial resources anyway; it massively matters how much money you put behind a track to reach or stay at No.1. Why is that not changing? Why are shareholders not becoming more nervous about this narrative?

The fact is, even if nobody spent money on marketing new music you would still have charts, because consumers drive those charts, and consumers would still discover new music.

There has been some evidence of cutbacks on certain areas of frontline cost at the majors recently, though: At Universal, Motown has been FOLDED BACK INTO CAPITOL MUSIC GROUP; at Warner, Parlophone has been SEMI-FOLDED INTO WARNER RECORDS in the UK; at Sony, Arista in Nashville has been SHUTTERED. They’re just some recent examples.

Masuch: Yes. In my view, the coin is beginning to drop on how big the infrastructure should be [in chart-chasing labels], but the coin still hasn’t dropped on how big investments should be.

Think about the demographics: There are more people over 25 years old than under 25 years old in the world – and the over-25s have credit cards.

I think some economic choices in this business are still relatively uneducated.

Final question for both of you: If someone was just glancing at BMG’s 2022 results today, what would be the one message you’d encourage them to take away?

Coesfeld: We are super-active in the market, we are the best home for artists, and we really do care about what happens to their music. We are showcasing what we are able to do. We are all about respecting both an artist’s legacy and their future, and this is why we’ve outgrown the market.

Masuch: I remember sitting with a Sony executive back when we started the new BMG 15 years ago saying, ‘Hartwig, nobody needs another music company’. The years have shown that this industry and its artists needed the flexibility and openness that BMG brought, and that’s an ongoing story.

I hope BMG’s results encourage people to be open for change, because we are just at the beginning of a massive transformation for the traditional business.Music Business Worldwide