Included in the TMS catalog are songs Someone You Loved and Before you Go, which were hits for Lewis Capaldi and Don’t Be So Hard On Yourself for Jess Glynne.

The first annual revenue results for a major recorded music market in 2019 are in. They offer some brightly positive news for the entertainment business – alongside one very large, very important, question.

Namely: If streaming revenue growth starts significantly slowing down in the world’s biggest recorded music markets, what will it mean for labels (and their valuations) in the years ahead?

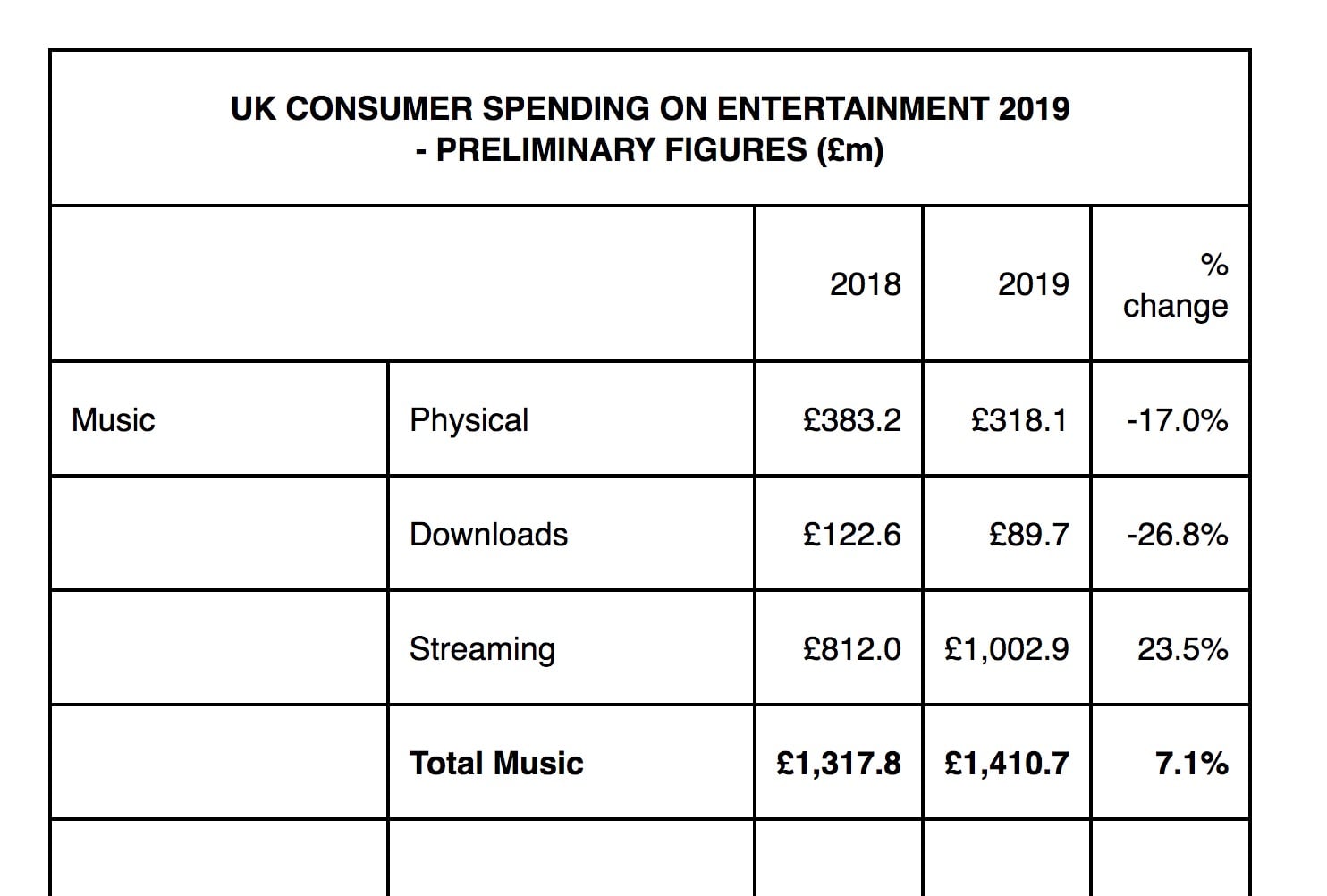

Before all of that, though, here’s the skinny: according to preliminary results from the Entertainment Retailers Association, consumers in the United Kingdom spent £92.9m ($122m) more on recorded music in 2019 than they did in 2018.

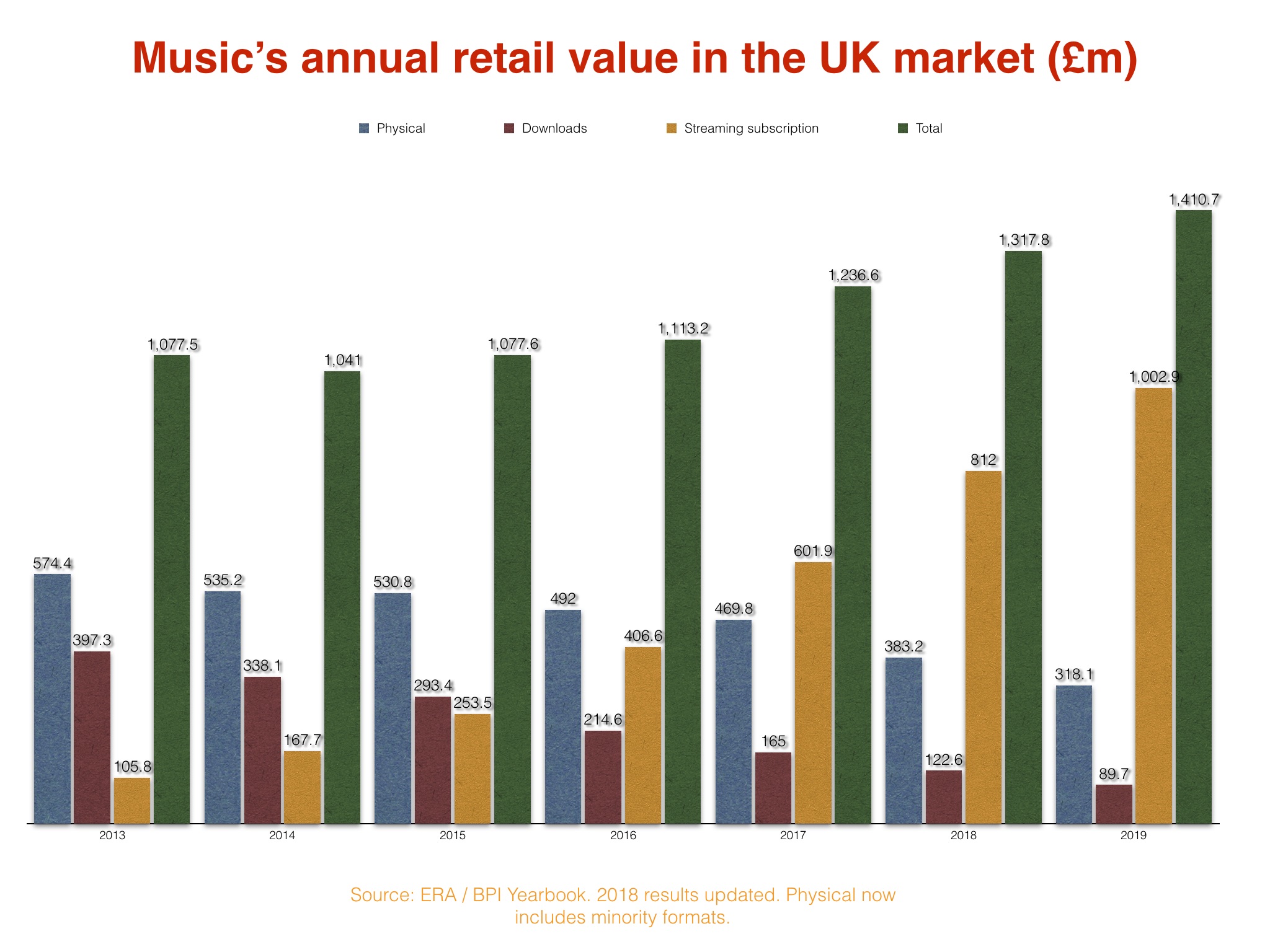

In total, UK music fans spent £1.41bn ($1.80bn) on recorded music across all formats in 2019, up 7.1% on the previous year (2018)’s haul of £1.32bn.

This growth took place despite another painful year for physical product.

The amount of money spent on CD albums in the UK last year fell 24.7% to £217m ($277m), according to ERA‘s figures. That was not only down by £71m ($91m) on the prior year, but it was also less than half the size of the £468m generated by the CD format as recently as four years previously (2015).

Overall, UK consumers spent £318.1m ($406m) on physical formats last year, down 17% on the £383.2m they spent in 2018. (2019’s physical figure was helped by vinyl LPs, which saw annual UK consumer expenditure rise 6.4% to £97.1m.)

Where did all of last year’s industry growth come from? Streaming, obviously – which brings us back to that very large, very important question.

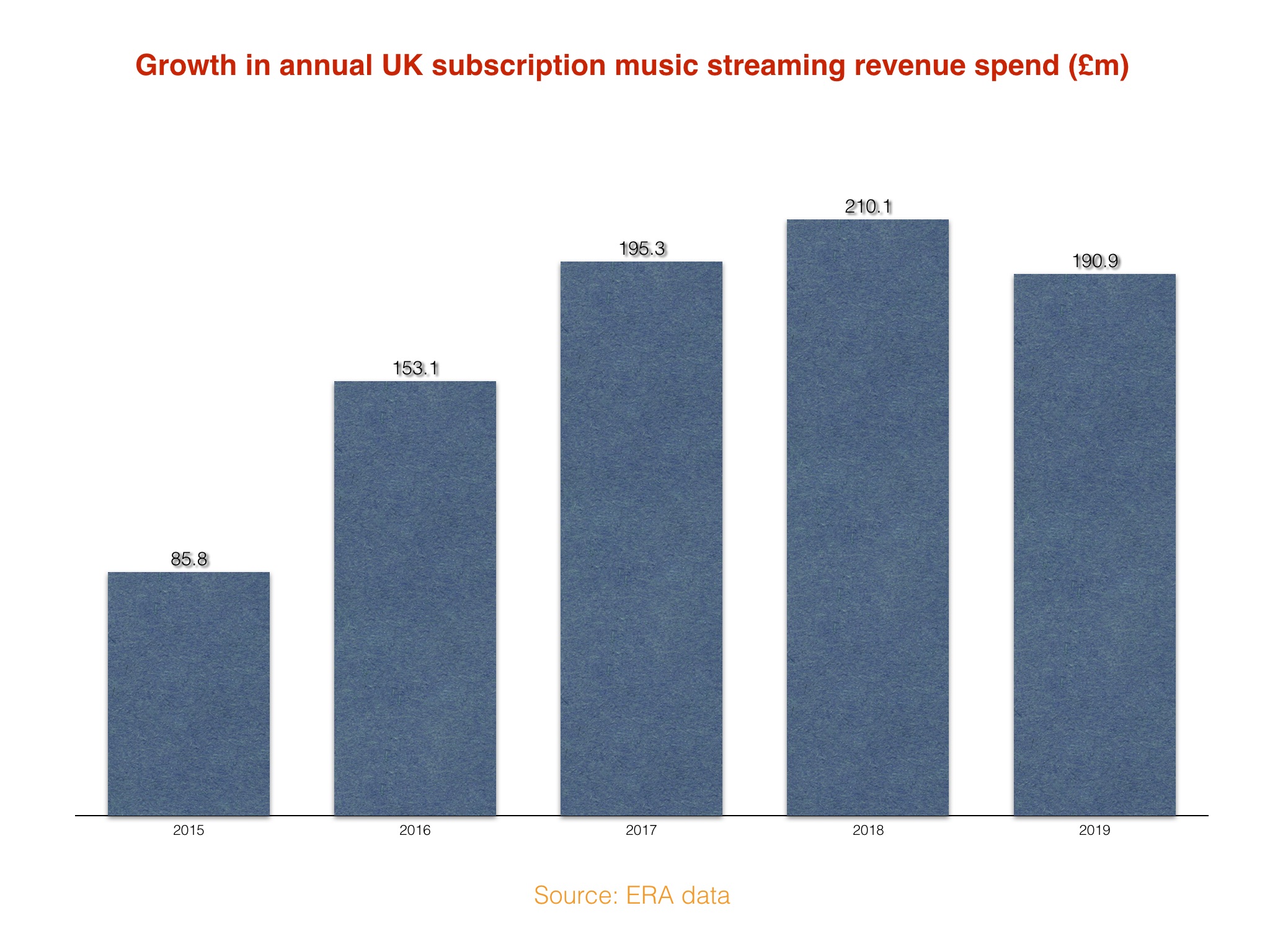

According to ERA’s preliminary stats, UK consumers spent £1.003bn ($1.28bn) on subscription streaming services last year. (ERA’s streaming numbers don’t include additional ad revenue from ‘free’ tiers and platforms.)

That subscription haul was up by a hefty £190.9m on ERA’s equivalent streaming figure from the prior year (£812m).

However, that £190.9m, in turn, represented a significant slowdown in annual streaming revenue growth: by way of comparison, in 2018, UK consumers spent £210.1m more on streaming services than they did in 2017.

In fact, 2019’s streaming growth figure (+£190.9m) was also smaller than the equivalent annual growth number from 2017 (+£195.3m).

On one hand, this slowdown is only natural: as streaming subscription growth matures in key global markets, the industry should obviously expect to see year-on-year gains begin to decelerate in territories like the UK.

This exact point was noted by ERA CEO Kim Bayley when announcing today’s numbers. She said: “As more and more people sign up to streaming services, it obviously becomes a challenge to maintain the same rate of growth, but the fact is UK music fans spent £190m more on subscription streaming services in 2019 than they did the year before – that’s more than twice the value of the entire vinyl market.”

“As more and more people sign up to streaming services, it obviously becomes a challenge to maintain the same rate of growth, but the fact is UK music fans spent £190m more on subscription streaming services in 2019 than they did the year before.”

Kim Bayley, ERA

Yet it’s also true to say that, should the recorded music industry want to regain and surpass the global revenues it enjoyed at its peak (1999), it may now have to look outside its biggest markets, and rely on two unpredictable factors: (i) Growth in traditionally non-dominant global territories such as India, Africa, China and Russia; and (ii) Innovation in the streaming marketplace, potentially bringing new crowds of as-yet-non-paying customers to monetized music.

(It’s worth pointing out that ERA’s figures are all retail numbers; the record labels – and their artists – only get their wholesale payments after ‘retailers’, including streaming services like Spotify and Apple, take their margins.)

Another revelation in ERA’s 2019 figures: download sales in the UK tumbled again last year to just £89.7m, less than half the size they were three years prior (2016).

And, as the eagle-eyed amongst you will have spotted, subscription streaming services (£1.003bn) now generate more than three times the amount of money spent on physical music (CD plus vinyl and other formats) in the UK.

In fact, subscription streaming was responsible for more than two-thirds (71.1%) of the total UK recorded music market last year.

ERA and the BPI have confirmed that the UK’s biggest selling album of 2019 was Divinely Inspired To A Hellish Extent by Lewis Capaldi (pictured), with equivalent sales of around 641,000.