The MBW Review gives our take on some of the music biz’s biggest recent goings-on. This time, we take an in-depth look through Spotify‘s filings for signs that it may one day be able to become a profitable company. The MBW Review is supported by FUGA.

On the face of it, it ain’t good news for Daniel Ek.

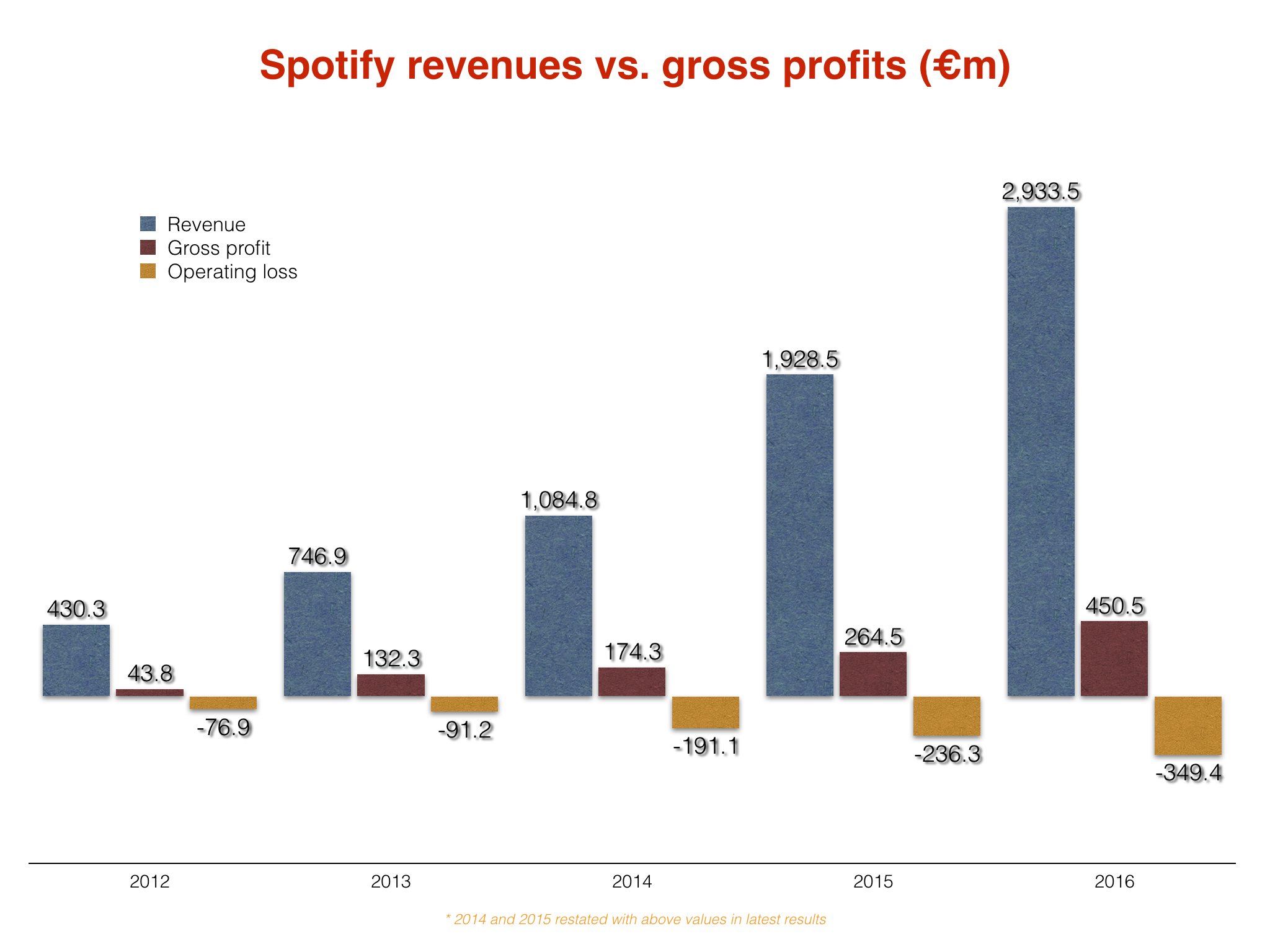

Spotify’s annual results, filed last month in Luxembourg, portray a business whose losses are far outpacing its revenue growth – with 2016’s sales up 52% to $3.3bn but net losses widening 133% to nearly $600m.

The first apparent conclusion from this data is one of a faltering business model – where every additional Spotify subscriber is further damaging the company’s bottom line.

As VICE pithily put it: “Spotify’s users are loving it to death.”

Such headlines are unhelpful for Daniel Ek and his board as they strive to float Spotify in the coming months – particularly as they fly in the face of the evergreen mantra that Spotify will eventually become a profitable entity “at scale”.

This catchy maxim once again reared its head in Spotify’s annual fiscal filing.

‘We believe our model supports profitability at scale,’ said a note to investors, adding: ‘We believe we will generate substantial revenues as our reach expands and that, at scale, our margins will improve.’

The question is… what is ‘scale’, exactly?

Because Spotify’s subscriber base (50m+) is already close to three times the size it was two years ago – and five times the size it was three years ago.

As such, the company looks in serious danger of being ‘loved to death’ unless significant changes are made to its operation.

The good news: theoretically speaking, there are a number of ways Spotify could pull its numbers back from the brink over the next few years – either by saving money in areas of over-expenditure, or simply by generating more cash.

Here are a few of them…

1) Watch the pennies

An interesting fact: Spotify committed €418m ($463m) to sales and marketing around the world last year – a larger sum than that representing its total annual operating loss (€349m – $387m).

Obviously, the idea that Spotify should arrest its promotional activity in order to force its finances back into the black is a bit silly.

But this data does at least add credence to the idea that, once Spotify reaches that magic level of ‘scale’ – ie. annuity income from a critical mass of repeat subscribers – it can slow down on marketing spend and draw back a meaningful chunk of its annual losses.

Between 2014 and 2016, Spotify’s annual marketing spend increased by a whopping €234m ($259m) – more than doubling over the course of just two years.

Compare that to other key outgoings, such as product development, which grew by a milder 81% in the same time period, and it suggests that a pruning of Spotify’s marketing expenditure growth could be on the cards in the coming years – a move which have a significant impact on its bottom line.

The fact that Spotify is still arriving in major global territories (such as Japan, where it launched in September last year) is no doubt having a big effect on its need for it to heavily market to new audiences.

Another significant – and growing – cost at Spotify which may need to come under the microscope is its wage bill.

Spotify’s salary expenditure reached €231m ($256m) in 2016, up 41% on the €163m ($181m) it committed in 2015.

Over the past two years, the average annual wage of a Spotify employee has grown 27% – up from €84,446 in 2014 to €106,841 in 2016.

In the same time period, its global headcount has jumped 59% from 1,364 to 2,162.

To put Spotify’s fast-expanding size into perspective: Warner Music Group, across publishing and records, employed approximately 4,445 people worldwide as of the end of September last year.

Talking of majors… Spotify is believed to have asked the recorded music companies of Universal and others to accept a smaller revenue share each year, down from 55% to around 52%.

If Spotify had kept this extra 3% of its pre-tax revenue last year, it would have saved around €88m ($97m) – a useful bump, but by no means a magic bullet to reverse its operating losses.

2) Increase worldwide sales… especially outside of the USA

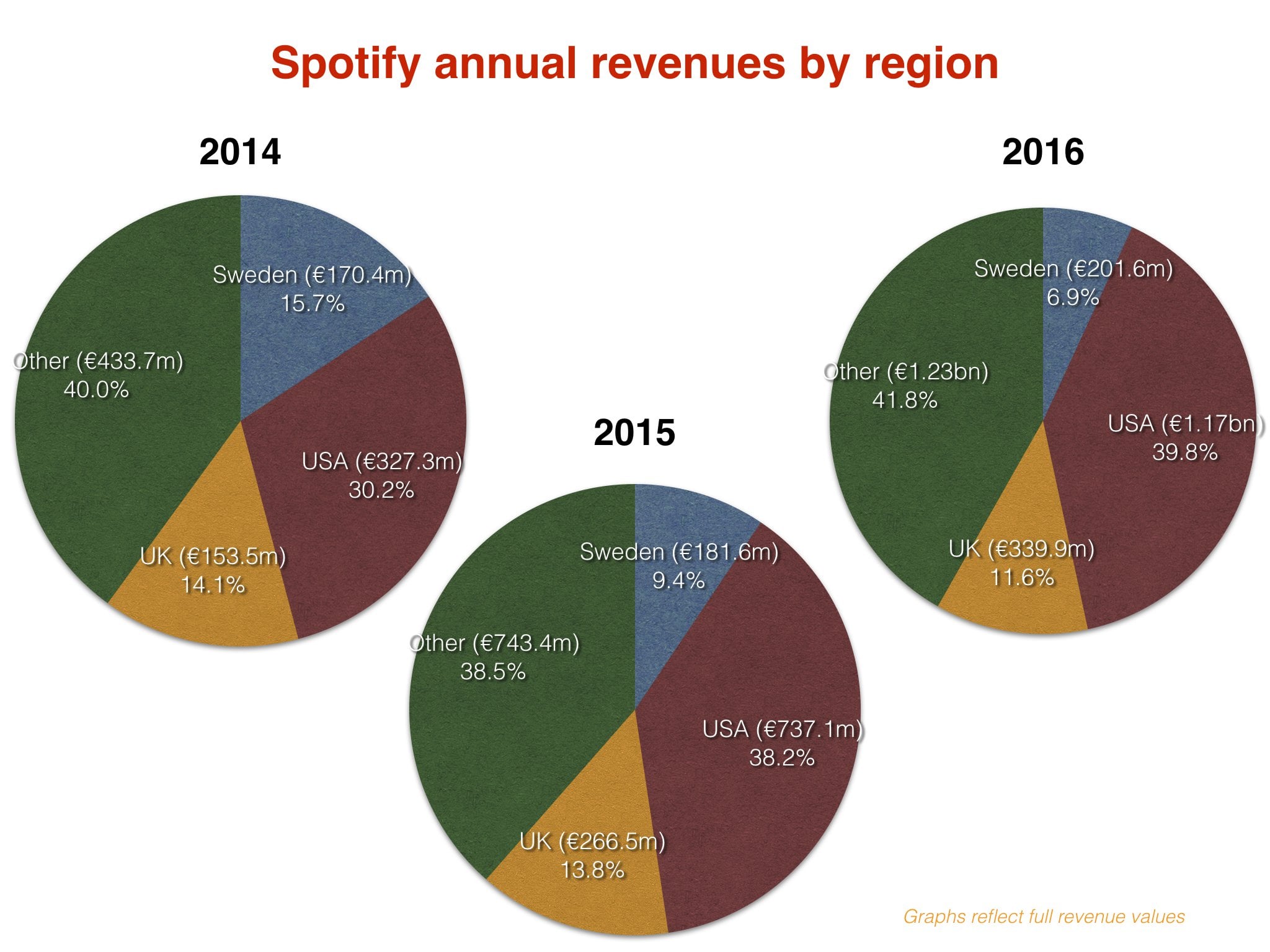

Bucking the trend of most global entertainment businesses today, Spotify is becoming increasingly American.

In 2016, just shy of 40% of its total revenues were generated in the US, up from the 38% share the States took in 2015 – and the 30% portion it claimed in 2014.

On the one hand, this is testament to an impressive performance from Spotify in the world’s biggest recorded music territory, where it has refused to cede ground as market leader since Apple Music‘s arrival in 2015.

On the other hand, it perhaps speaks of the unfulfilled opportunity for Spotify in markets outside of North America.

Between 2014 and 2016, for example, Spotify’s revenues in the US region more than trebled. Last year alone, its US revenues grew by 58%, or €429m ($475m), to top $1bn for the first time.

Perhaps inevitably, Spotify’s revenue growth in more mature streaming markets has slowed. Sales in its home territory of Sweden, for example, grew just 11% last year.

Meanwhile, its revenue increase in all territories outside the US, Sweden and UK last year was €481.6m ($533m) – slightly larger than its US-based increase… but not by a lot.

As markets still dominated by physical formats – notably Germany and Japan – become more streaming-friendly, and as developing nations establish solid, legitimate recorded music businesses, Spotify’s ability to become less reliant on its Stateside performance will become increasingly crucial to its fiscal health.

3) Fixing its advertising business – and arresting the decline of its average subscriber spend

Spotify’s advertising business performs a hugely important function as an entry point for consumers who are then upsold to the paid-for Premium service.

Considering Spotify’s conversion rate between these two tiers has never been higher (currently at around 38%), it’s obviously working.

However, in terms of a standalone revenue generator, the company’s ad-funded tier remains a serious disappointment – and a weak counter-balance to its company-wide expenditure.

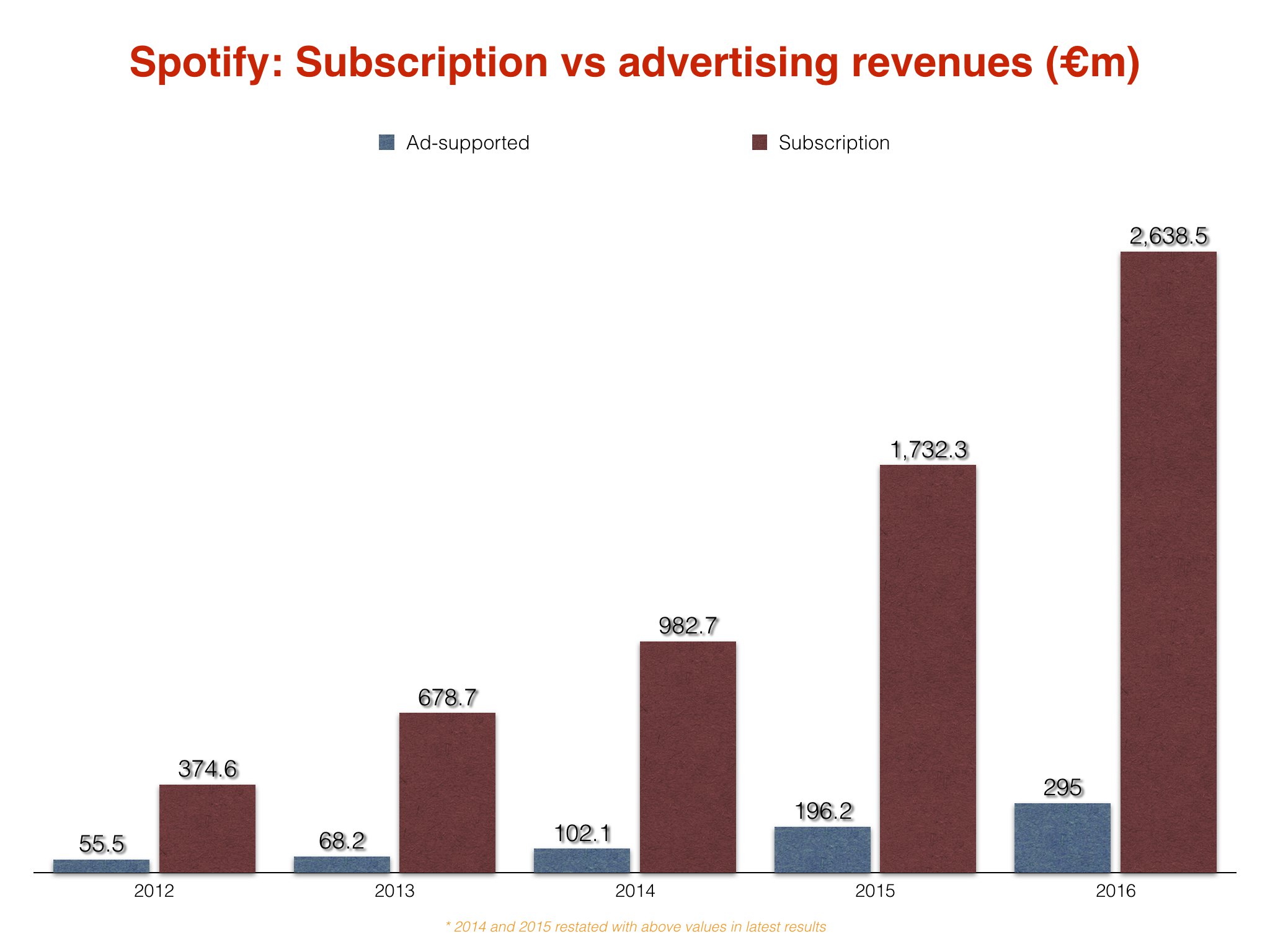

Last year, Spotify made just €295m ($326m) from advertising, up 50% on the €196.2m ($217m) generated in 2015.

Compare that to Pandora, which finished 2016 with $1.1bn in revenues from audio ads – around three times bigger than Spotify – and you can see the potential.

Now… compare it to the traditional US radio industry, which generated an estimated $14bn in over-the-air ads last year, and that potential only gets more exciting.

Going off Spotify’s confirmed 2016 year-end user stats (which will naturally result in a slightly conservative approximation), its 78m ‘free’ users generated an average of €3.78 ($4.18) each last year.

If the firm could have raised this per-head figure by just €2.25 ($2.50), it would have wiped away half of its yearly operating loss.

Spotify can’t be accused of not seeking new advertising opportunities: the company was recently caught testing a ‘Sponsored Songs’ ad-slot within key playlists, presumably as a means to claw back some revenue from record labels in the future. Yet more innovative ideas will be needed to lure radio’s dollars to its service.

As for Spotify’s subscription revenues, well, we’ve already covered that in depth through here.

In a nutshell: thanks to aggressive price promotions, mobile bundles and global expansion, the average global Spotify subscription price has fallen by 35% since 2013, and now stands below €5 per month.

Spotify must stop this price erosion if subscriptions are going to become its golden ticket back to profitability.

It will certainly help when subscribers currently enjoying price promotions tick over to paying full whack. But it’s going to take more than that for a true transformation in ARPU – perhaps involving the launch of some kind of ‘super-fan’ or HQ audio-based higher-price tier.

The kicker: if the 48m people subscribing to Spotify at the end of 2016 would have just spent an extra €7.27 ($8) over the course of last year – or €0.61 ($0.68) per month – Daniel Ek’s business would have posted an operating profit in 2016.

(All US $ figures above translated at 2016 yearly average exchange rates for consistency in comparison.)

Music Business Worldwide