Credit: PressHipgnosis Songs Fund will be very unlikely to sell its stake in Mariah Carey's huge streaming hit, All I Want For Christmas Is You. But might it divest some of of the other copyrights it acquired from Kobalt in 2020?

MBW Explains is a series of analytical features in which we explore the context behind major music industry talking points – and suggest what might happen next. MBW Explains is supported by JKBX, a technology platform that offers consumers access to music royalties as an asset class.

What’s happened?

Revenue isn’t a problem for Hipgnosis Songs Fund (HSF). As MBW reported this morning (July 13), underlying net revenue at the UK-listed catalog company jumped by a healthy 10.9% YoY in the 12 months to end of March 2023.

HSF does, however, have a valuation problem.

On the London Stock Exchange, as this piece is published, shares in Hipgnosis Songs Fund are trading at GBP £0.738 each.

That’s around half the size of the per-share ‘operative net asset value (NAV)’ – USD $1.915 – that the company announced in its latest FY report.

Merck Mercuriadis, founder and CEO of Hipgnosis Songs Fund, is not hiding his irritation over what he sees as an artificial delta in his company’s current worth on the public markets vs. its true value.

“The current share price does not reflect the success of our investment strategy and I know all [HSF] shareholders share my frustration and disappointment that this is the case,” says Mercuriadis in his company’s FY 2023 report today.

Pointing at the potential reasons for HSF’s disappointing current share price, Mercuriadis notes: “When we launched the company, we created a new asset class with songs.

“It is therefore perhaps not a surprise, that in a world of incredible turmoil following a global pandemic, the largest war in Europe in nearly 80 years and increasing inflation and interest rates, that some investors have turned to ‘risk-free’ safe havens overexposure to new asset classes.”

The hope for HSF’s management and shareholders in recent months was that the continued strong growth in music’s paid streaming revenues would combine with a downward trend in interest rates to boost HSF’s share price.

That – particularly the interest rate part of it – hasn’t happened.

“It is perhaps not a surprise that in a world of incredible turmoil following a global pandemic, the largest war in Europe in nearly 80 years and increasing inflation and interest rates, that some investors have turned to ‘risk free’ safe havens over exposure to new asset classes.”

Merck Mercuriadis, Hipgnosis, on the factors behind HSF’s current depressed share price

Now, some of HSF’s biggest shareholders are hatching a plan to pump up the company’s public valuation via tactical methods, including a potential corporate share buyback and – most notably – through the disposal of some assets in the marketplace.

If HSF can sell a sliver of its assets at a price that reflects their true value, goes the logic, that in turn will be an indicator that the current public value of the firm’s entire portfolio is being unfairly suppressed. HSF’s share price may then enjoy a natural bounce as a result.

Solomon Nevins from CCLA, which owns 4.9% of Hipgnosis Songs Fund, told the Financial Times this week: “The big thing to get the share price moving would be to dispose of less attractive catalogs in the portfolio and give a meaningful return to shareholders.”

He added: “Where the shares are trading today, there must be something in the portfolio that makes sense selling, to buy shares back.”

Caspar Rock, Chief Investment Office at Cazenove Capital, which owns 6.2% of HSF, told the FT that, on balance, an asset sale to boost the share price would not be his preferred strategy.

However, he admits: “For some investors, validation of the valuation through a transaction . . . would release equity and reduce gearing.”

So if Hipgnosis Songs Fund does go down the route of selling some copyrights, which songs might it be willing to part with? And who will it sell them to?

What’s the context?

At this stage, we need to do something we nearly always end up doing in reports about Hipgnosis (!) and reiterate the structure of its three-headed ‘family’:

As mentioned, Hipgnosis Songs Fund is a UK-listed public fund that owns shares in over 65,000 songs;

Elsewhere, there’s Hipgnosis Songs Capital, a private fund with over a billion dollars of Blackstone’s money at its disposal, which launched in late 2021. So far, it’s spent over $700 million on catalogs – including, in the past 18 months, portfolios created by the likes of Justin Bieber, Tobias Jesso Jr., Leonard Cohen, Justin Timberlake, and Nile Rodgers;

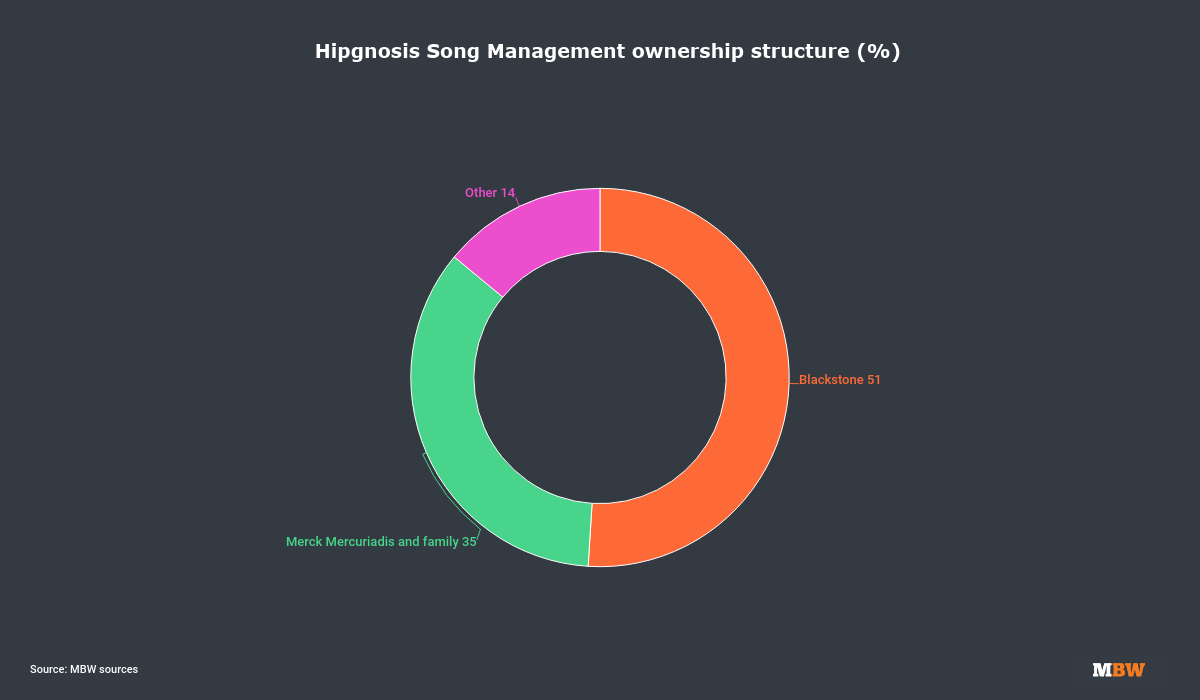

Finally, there’s Hipgnosis Song Management – the investment advisor to the two Hipgnosis funds (the public and private ones), which also markets and promotes catalogs owned by the Hipgnosis companies.

Hipgnosis Song Management is run and co-owned by Merck Mercuriadis, and majority-owned by Blackstone (which is understood to own a ~51% stake in HSM).

One very important factor here that doesn’t get much airtime: MBW understands that Hipgnosis Song Management – the investment advisory firm – has a ‘first refusal’ agreement with Hipgnosis Songs Fund should the latter company seek to sell any of its assets.

What this means in practicality: The ‘left hand’ (Blackstone-bankrolled Hipgnosis Songs Capital) would have first refusal to buy any prospectively-disposed-of copyrights from the ‘right hand’ (Hipgnosis Songs Fund) via their mutual middleman (Hipgnosis Song Management).

This obviously complicates the idea of HSF offloading a few copyrights in music’s M&A ‘marketplace’ in months to come if Blackstone/Merck Mercuriadis want to keep said copyrights ‘in the family’.

Would selling one asset from the ‘right hand’ to the ‘left hand’ satisfy the goal of proving the value of the HSF portfolio in the private market? Maybe.

But there’s another possibility, too: Hipgnosis Song Management (and Blackstone) might agree to pass up their ‘first refusal’ on certain assets and allow them to be sold outside the Hipgnosis ‘family’.

If we had to guess which asset might get sold? Here’s an idea.

In November 2020, Hipgnosis Songs Fund announced that it had acquired over 33,000 songs/portions of songs from Kobalt Capital for a total price of $323 million.

These songs included massive global hits made famous by the likes of Mariah Carey (All I Want For Christmas Is You), as well as Lindsey Buckingham and Steve Winwood.

“The big thing to get the [HSF] share price moving would be to dispose of less attractive catalogs in the portfolio and give a meaningful return to shareholders.”

Solomon Nevins, CCLA, speaking to the FT

However, the 33,000 songs in the Kobalt deal included a large tranche of 18,000 songs from the Nettwerk music publishing catalog, which Kobalt Capital itself acquired in 2016.

That Nettwerk catalog includes many critically acclaimed songs – by artists such as 10,000 Maniacs and Tasmin Archer – that arguably don’t fit with Hipgnosis Songs Fund’s central thesis.

That thesis, to quote Mercuriadis in HSF’s latest report, is laser-focused on “a portfolio of songs that is unrivaled for its extraordinary success and cultural importance”.

The Kobalt transaction was also unique in Hipgnosis history: It appears to be the only time that Mercuriardis (via a Hipgnosis company) has not directly acquired rights from an artist or songwriter – meaning his company arguably has a lesser connection to the talent behind the Nettwerk portfolio that with (to name just a few artist/writers who’ve sold assets to Hipgnosis companies in the past five years) Justin Timberlake, The-Dream, Lindsey Buckingham, or Neil Young.

Could Hipgnosis be willing to sell off some or all of this Nettwerk catalog into the marketplace?

If so, could the eventual buyer end up being a major music company, or a private equity-backed rival?

Another possibility: Hipgnosis might, for neatness, be attracted to selling the Nettwerk catalog back to Kobalt Music Group, which continues to administer it today, and is now an active music copyright buyer via cash on its own balance sheet.

What happens now?

Which copyrights will Hipgnosis decide to sell – if it decides to sell?

If you’re looking for potential criteria for Mercuriadis and his shareholders to follow, you probably won’t get a sharper one than that offered by Solomon Nevins from CCLA in the FT.

Nevins suggests that Hipgnosis should look to sell some “less attractive catalogs in [its] portfolio” without “selling the family silver to buy shares”.

One potential obstacle hanging over all of this: It will ultimately be up to the Hipgnosis Songs Fund shareholders to decide whether it disposes of some assets (whether they’re “less attractive” or “more attractive”!). They will have the final vote on the matter.

Mercuriadis nodded to this fact in Hipgnosis Songs Funds’ FY2023 report today (July 13), writing: “[We] have been working with the Board, following consultation with many of our largest shareholders, on a number of options to enhance shareholder value. We look forward to updating the market prior to the AGM [Annual General Meeting] and the Continuation Vote.”

HSF’s AGM this year will arrive in September, so we can expect an update on any asset sale strategy/process within the next two months.

A final thought…

You might have noticed Merck Mercuriadis also mentioned a “Continuation Vote” in his quote above. It’s very relevant.

In September, at that AGM, HSF’s shareholders will vote on whether they believe the company should continue to operate as a publicly-listed entity on the London Stock Exchange.

This ‘Continuation Vote’ takes place every five years at HSF (we’ve just past five years since HSF IPO’d on the LSE in summer 2018).

There are shareholders who already look odds-on to vote ‘yes, let’s keep this going’ at the AGM.

“We don’t think the current share price is a true representation of the value of the company.”

Paul Flood, Newton Investment Management, speaking to the FT

Such shareholders (plus analysts like JP Morgan) believe in the long-term value of HSF, and that its share price will naturally recover over time – meaning its public valuation closes the gap on its private valuation.

Take, for example, Caspar Rock of Cazenove Capital, who told the FTthis week that, rather than sell off assets in a short-term bid to boost HSF’s share price, he would “prefer them to carry on and let revenues grow and eventually the valuation should reflect the performance of the portfolio”.

Paul Flood, Head of Mixed Assets at Newton Investment Management (owner of nearly 10% of HSF) offered similar levels of confidence in HSF when talking to the FT, saying: “We don’t think the current share price is a true representation of the value of the company.

“We continue to see a recovery in performance revenues, as consumers return to concerts and the tailwinds benefiting the music industry from music streaming.”

Other shareholders, however, may be feeling less bullish, more impatient, and concerned over the gulf between HSF’s private and public valuation.

Mercuriadis and his team may be hoping that an asset sale in the months ahead – and a consequential boost to HSF’s share price – will stave off any doubts over the company’s long-term value potential… and encourage investors to choose ‘yes, let’s keep this going’ at that all-important Continuation Vote.

Reservoir (Nasdaq: RSVR) is a publicly traded, global independent music company with operations across music publishing, recorded music, and artist management.Music Business Worldwide