Last Wednesday (April 5), the wind changed.

William Packer, an influential media and tech analyst for BNP Paribas Exane, issued a research note with a surprising conclusion: Packer had decided to double-downgrade Universal Music Group‘s stock, from outperform to underperform.

This in itself was unusual: According to TipRanks, of the 15 Wall Street analysts who’ve given views on the value of UMG’s stock in the past year, just two are outright negative: Packer, and Joseph Thomas at HSBC.

All but one of the rest – a ‘Hold’ rating from CitiGroup – continue to rate UMG’s stock as a ‘Buy’, albeit with different levels of optimism.

The ranks of this ‘Buy’ group include the likes of Andrew Uerkwitz (Jefferies), Daniel Kerven (JP Morgan), Julien Roch (Barclays), Lisa Yang (Goldman Sachs), Matthew Walker (Credit Suisse), Michael Morris (Guggenheim), Omar Sheikh (Morgan Stanley), and Richard Eary (UBS).

Packer’s downgrade was extra surprising for the fact that, over the past few years, he’s been an unwavering champion of the potential of UMG’s stock value.

So what was it that spooked Packer into demoting his view of Universal’s commercial future?

A few things contributed to his decision, including doubts over the size of TikTok’s payments to the music business, and his assumption that the most meaningful revenue boost to UMG from streaming price rises may already be behind it.

There was, though, one factor that stood out above any other in Packer’s analysis: The potential impact of artificial intelligence (AI) on the music industry in the years ahead. And, in particular, on the major record companies.

Packer wrote that “AI is a new disruptive threat” where “a glass half full industry narrative is holding… for now”.

He added: “While UMG is likely to remain a long-term winner from digital[z]ation, we think AI music is to emerge as a challenging thematic and drag on elevated multiples.”

Packer specifically argued that vast volumes of AI-created music could “accelerate [market] share loss” for UMG and the other major record companies.

As such, he touched on a recurrent conversational theme in today’s business: What happens to major record company streaming market share when the dam breaks, and we start to see millions of songs, all made by AI, distributed to Spotify et al each day?

Millions of tracks, but is anyone listening?

Masses of AI-created, or at least AI-assisted, music is already washing up on the shores of today’s digital music platforms.

One AI-powered music-making startup, Boomy, says its users have created over 12 million songs since it launched in 2019.

The crucial question, though, especially when contemplating AI’s potential erosion of major record company market share, is how many people are actually listening.

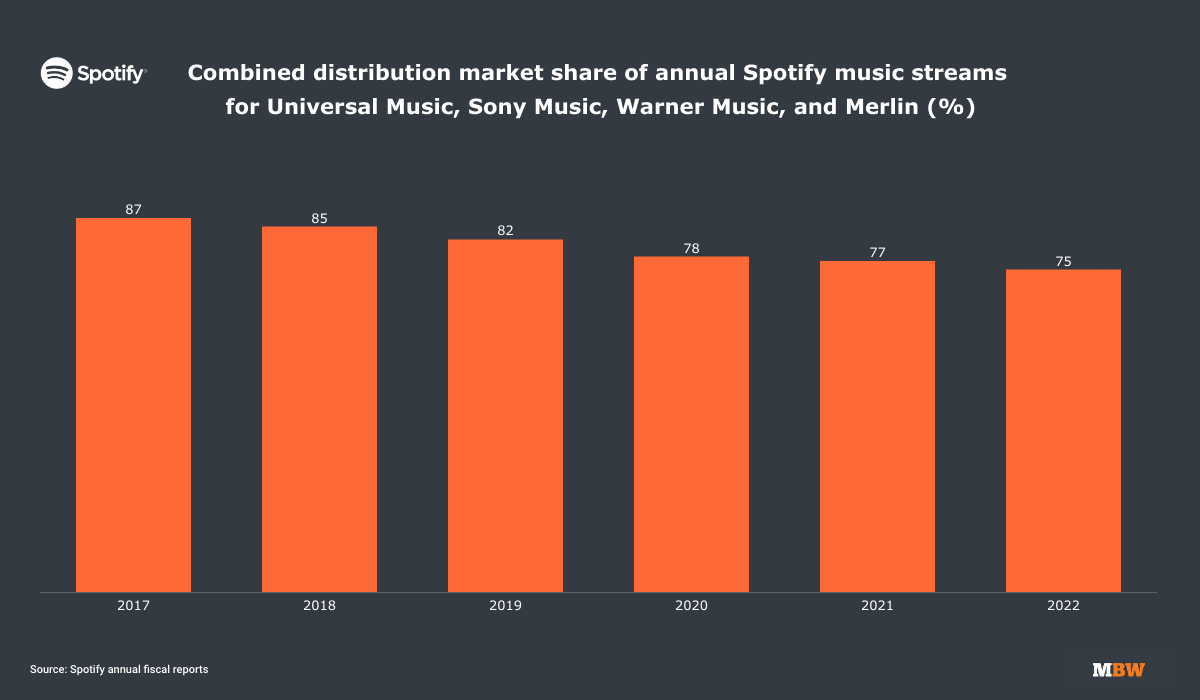

The stat that is often bandied around at this point – and I shall do the same – is that which shows streaming volume market share decline for the major record companies (as well as Merlin members, aka most large independent labels) on Spotify over the past five years.

In 2022, according to Spotify’s annual report, music distributed by the major record companies and their subsidiaries, plus Merlin members and their subsidiaries, lost 2% annual market share of total volume of music plays on Spotify (see below).

And across the five years from 2017-2022, these entities lost a total of 12% market share on the service, down from 87% to 75%.

Yet here’s something that’s rarely remarked upon: The above represents astonishingly strong market share maintenance from the majors (and Merlin) in the face of an overwhelming glut of music being released.

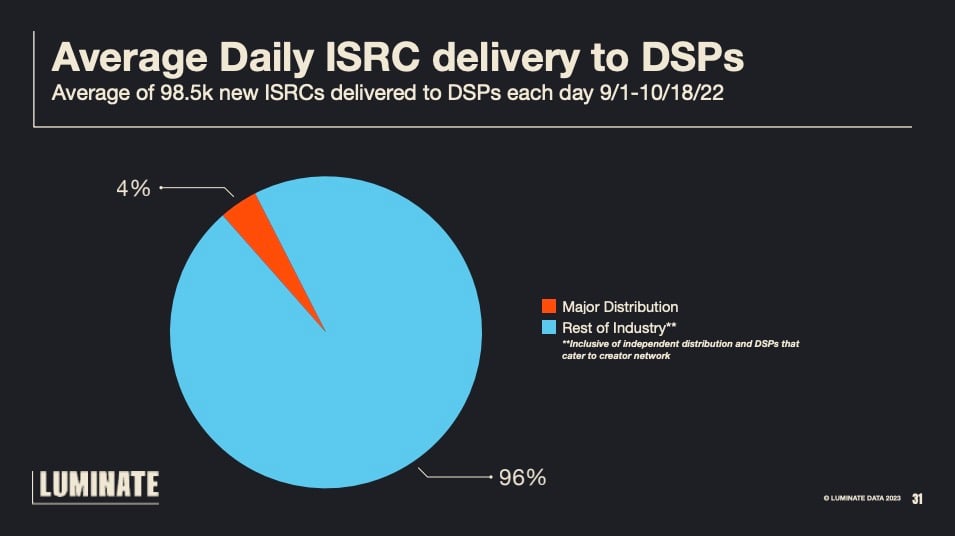

As MBW reported last month, there are – according to market monitor Luminate – around 98,500 separate ISRCs (aka separate tracks or videos) released to music streaming services daily today, a mix, no doubt, of human-created and AI-created music.

The volume of music created in the past few years is unfathomably large: nearly 50% (!!!) of the ≈100 million tracks available on Spotify et al today were created and uploaded in the past three years alone.

Conclusion: The major record companies (and their ‘indie’ distribution subsidiaries) are releasing a weeny fraction of the ≈35 million new tracks/videos now hitting music streaming services every 12 months.

How is it, then, that those major record companies (along with Merlin-affiliated indies) only lost 2% of overall volume market share on Spotify in 2022?

In a word, curation.

Why the major record companies may be well-positioned for the coming AI onslaught

The statistics prove that the vast majority of music being released today – whether by robots or humans – isn’t only barely being listened to; in a lot of cases, it’s not being listened to at all.

MBW pointed to this fact last month, when we cited Luminate data showing that some 38 million tracks on music streaming services didn’t attract a single play in the whole of 2022.

This story is even better illustrated by Spotify’s Loud & Clear, the data site published by Daniel Ek‘s company annually.

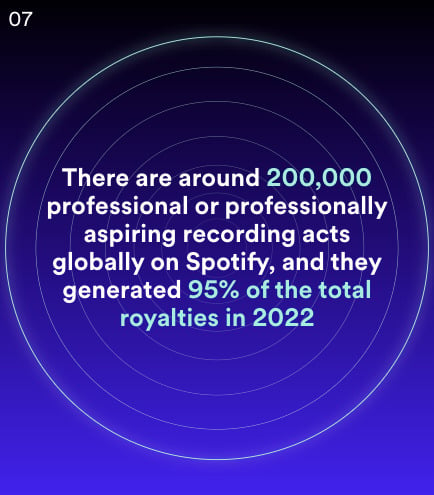

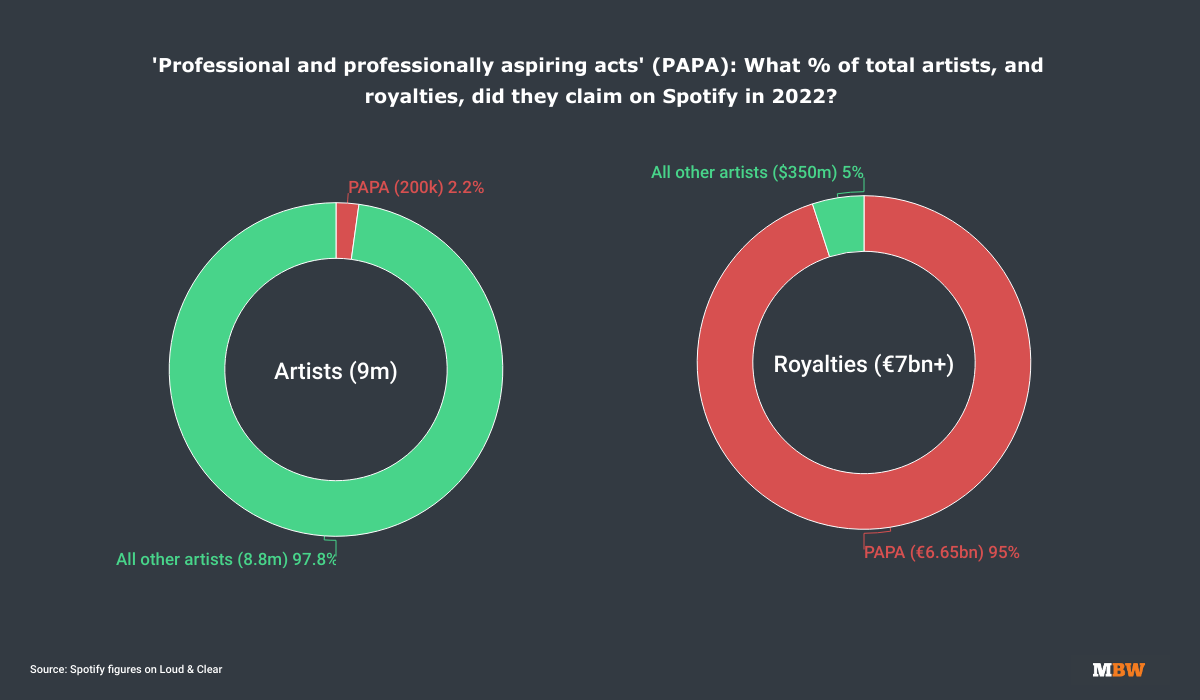

According to the latest update of Loud & Clear, Spotify estimates that there are around 200,000 “professional or professionally aspiring artists” operating on its service today.

Spotify characterizes a “professional or professionally aspiring artist” as someone who has (a) released more than 10 tracks on its platform to date (5.6 million artists have not, says Spotify), and (b) who averages more than 10,000 monthly listeners.

Those two qualifiers combined, says Spotify, apply to just 213,000 artists in total.

Spotify brings down that 213,000 figure in its “professional or professionally aspiring” calculation to 200,000 by mixing in data regarding the number of artists who hosted a gig or virtual live event in 2022, a figure it says shakes out at 189,000.

These are the exact kind of artists, of course, that major (and indie) record companies are interested in signing/investing in – something we’ll come back to.

Anyway, the important bit: The 200,000 “professional or professionally aspiring artists” on Spotify today represent just 2.2% of the 9 million music artists whose music the firm says it hosts on its platform.

And yet, according to Spotify, the same 200,000 “professional or professionally aspiring artists”, in 2022, generated a whopping 95% of all royalties on the service.

It’s a stunning stat, but also one that speaks to one of the flaws of over-analyzing the Spotify market share chart at the top of this story.

That chart, remember, is for total plays on Spotify; it doesn’t differentiate between the high-royalty plays taking place on Premium Spotify accounts, and the low-royalty plays taking place on ‘free’ Spotify accounts.

The fact that 95% of all royalties on Spotify are being generated by just 200,000 “professional or professionally aspiring artists” proffers an important fact: ‘Professional’ artists, with proper fanbases, are being listened to by more valuable (i.e. paying) listeners on streaming services.

As such, the major record companies will be far more concerned about maintaining market share amongst these 200,000 acts (and others who’ll join their league in years to come), than they will the other 8.8 million artists / ‘artists’ on Spotify today who, I remind you, only generate 5% of all royalties.

(As exemplified in the chart above, the last official annual royalty payout figure we have from Spotify, across records and publishing, is for 2021, when the service distributed ‘over EUR €7 billion’ to music rightsholders. Rounded down, those 200,000 ‘professional or professionally aspiring’ artists would have generated €6.65 billion of a €7 billion royalty payout in 2022.)

What does all that have to do with AI?

These stats suggest that the real threat to major record companies from AI music isn’t, as is often proposed, one of sheer volume.

The modern music industry, as evidenced by the above, already has a gigantic imbalance between supply and demand. An explosion in AI music would certainly super-size the supply. But in music listening, as was ever the case, it’s the demand that really matters.

That’s not to say AI-created music can’t or won’t have a serious commercial impact on the music business in the next couple of years. But its biggest influence, especially market share-wise, will probably be felt where there is a natural listener demand for it – and, in my view, that’s not in pop music. It’s in music for application (or as Sir Lucian Grainge would have it, “functional” music.)

One only need look to Berlin-headquartered Endel for evidence. The company, with backing from the likes of Amazon Alexa and Avex Group, positions itself as a “sound wellness company”, whose proprietary AI “create[s] personalized, functional soundscapes to help people focus, relax, and sleep”.

Outside of Endel’s clever tech (with soundscapes that change based on a user’s movement, heart rate, location and other factors), Endel’s doing something else unusual for an AI music startup: It’s actually measuring its success on the number of listeners it’s reaching.

Endel says its “ecosystem” of soundscapes already has over a million monthly users, who listen, cumulatively, to a million and a half hours a month of Endel’s sounds.

Stats like this are not, to my mind, an endemic threat to Universal Music Group, whose strategic bedrock continues to be music made by artists with identities that have meaningful real-world recognition. (Aka: Stars.)

I’d be far more concerned by Endel, and indeed the power of AI-generated “music for X” / “functional music” soundscapes, if I was, for example, Epidemic Sound – the $1.4 billion-valued Swedish company that’s amassed a very lucrative industry position by creating instrumental music for YouTubers and podcasts, and also by creating instrumental music that’s stuffed Spotify’s first-party ‘music for relaxation’ playlists.

(Sidenote: There will be some irony should music created by “fake artists” – to echo MBW’s now-infamous turn of phrase – ultimately be superseded on said Spotify playlists by full-blown robots.)

The real threat?

So, in conclusion, the major record companies are likely doing better in terms of Spotify value market share – rather than Spotify volume market share – than most typically understand.

This is happening because the majors (and their strongest indie peers) are continuing to focus on a couple of hundred thousand “professional or professionally aspiring” artists. These artists, unlike robots, (i) build fanbases by playing live, and (ii) are ultimately keen to be recognized and appreciated over and above the music they upload to faceless streaming services.

(A great analogy I heard the other week: Record companies strive to sign artists who pass the ‘pencil and paper’ test, i.e. if I gave you a pencil and paper, could you draw a decent approximation of the artist simply from your mind’s eye?)

The vast bulk of demand – monetized demand, at least – in the world of music listening continues to reside with these “professional or professionally aspiring” artists.

So the idea that a deluge of AI-generated songs (unless said songs are performed by “professional” artists!) will inevitably wash away major record company market power on streaming sounds to me a little hyperbolic.

“Lucy is [our] first super-realistic virtual idol.”

Tencent Music, speaking in December 2022

The bigger existential challenge for the majors from AI music isn’t one of impersonal volume; in my view, it’s one of human empathy.

We’re already seeing attempts from large tech companies, and indeed music companies, to market AI-created characters that resonate, emotionally, with human patrons. Avatars with enough mythology, enough Homo Sapien-esque traits – or a believable facsimile of them – to elicit true fandom from a large-scale audience.

I’m talking “professional or professionally aspiring” artists… who never perspire a single bead of sweat.

This is where things could eventually, theoretically get scary for the majors.

Witness ‘Lucy’, a priority project for China’a Tencent Music Entertainment (TME), which/who was first premiered in December.

TME’s AI capabilities in music are already under no doubt: The company boasted last year that it had fashioned 1,000 tracks with computer-made vocals that replicated human voices, including the voices of dead Chinese superstars. One of these tracks had drawn over 100 million plays, said TME.

Now, with Lucy, the firm has put an AI-generated face on this kind of machine-generated product – an avatar that it calls “[our] first super-realistic virtual idol”, built by TME’s in-house Lyra Lab’s LyraSinger Engine.

On an earnings call in March, TME Executive Chairman, Cussion Pang, said that Lucy’s team had already “created three chart-dominating original songs across different styles within just one month of [her] debut” and enticed commercial partnership interest from “a broad array of global brands” including Coca-Cola, and KFC.

We’ve seen this kind of thing before, of course.

In 2021 – complete with an MBW headline presaging the coming AI revolution in music – Warner Music China unveiled its own first-ever “virtual idol”, Ha Jiang.

Said WMG’s now-co-President of Asia, Jon Serbin, at the time: “‘Virtual idols’ are already a huge phenomenon in China, as well as other parts of Asia.

“They’re attracting big following on social media, particularly Gen-Z fans. People become really engaged with the idols’ daily lives, much like they are with real film stars or models.”

“I mean, sure, there’ll be a robot popstar at some point. Of course there will – everything that can happen will happen. But that’s not going to be the way the [majority of the] industry goes. It’ll be a one-off.”

Ed Newton-Rex, creator, Jukedeck

Could these “virtual idols”, replete with AI-composed music and human-mimicking vocals, really one day challenge the specialty of the major record companies: Globally marketed, human superstars with millions of ticket-and-merch-buying fans worldwide?

It’s here I turn to the words of a man in a better place than me to answer this question: Ed Newton-Rex, the creator of one of the first AI music-making platforms, Jukedeck, which he sold to Tiktok/ByteDance in 2019.

Newton-Rex recently told me on an MBW podcast: “What people really care about is a connection to the artist.

“I mean, sure, there’ll be a robot popstar at some point. Of course there will – everything that can happen will happen. But that’s not going to be the way the [majority of the] industry goes. It’ll be a one-off.

“That connection with human artists has got to be at least half of the reason that we love music. It’s not just about what we hear.”

That, in itself, will no doubt be music to the ears of Sir Lucian Grainge – fresh from his signing of a new 5-year deal to steer Universal through what may become the most disruptive technological period in major record company history.

Grainge clearly isn’t taking the threat from AI-powered ‘functional’ music lightly: At least a portion of his call for new “artist-centric” royalty models at music streaming services seems like agitating for an industry bulwark against the prospect of millions of high-quality instrumentals being spat out by machines at a rate of knots.

If so, Grainge is not alone in pondering how to trammel unhealthy elements of the advancement of AI in entertainment: Witness the growth of the AI-skeptical public policy body, the Human Artistry Campaign (HAC), whose members span music, sports, film, journalism and other disciplines of IP, and which just increased its membership base by 50%.

(Interestingly, Universal Music Group is a major impetus behind HAC; the US trademark for the org was filed by UMG itself.)

Ultimately, though, as set out in this article – and in the face of doom-laden narratives around AI’s impact on music’s biggest companies – there does seem to be a few solid reasons for that “glass half full industry narrative” to hold a little longer, at least.Music Business Worldwide