MBW’s Stat Of The Week is a series in which we highlight a data point that deserves the attention of the global music industry. Stat Of the Week is supported by Cinq Music Group, a technology-driven record label, distribution, and rights management company.

2022 was a big year for music publishing companies (plus their songwriters… and their investors) in the United States.

Not only did pubcos benefit from a rise in streaming activity in the US (the world’s largest music market), many of them also welcomed a substantial bump in performance royalty income, thanks to the re-opening of public spaces in multiple international territories following Covid lockdowns.

In addition, of course, there was that other major moment: last summer, the US Copyright Royalty Board (CRB) rejected appeals from platforms such as Spotify against a planned rate rise for publishers from streaming services in the States.

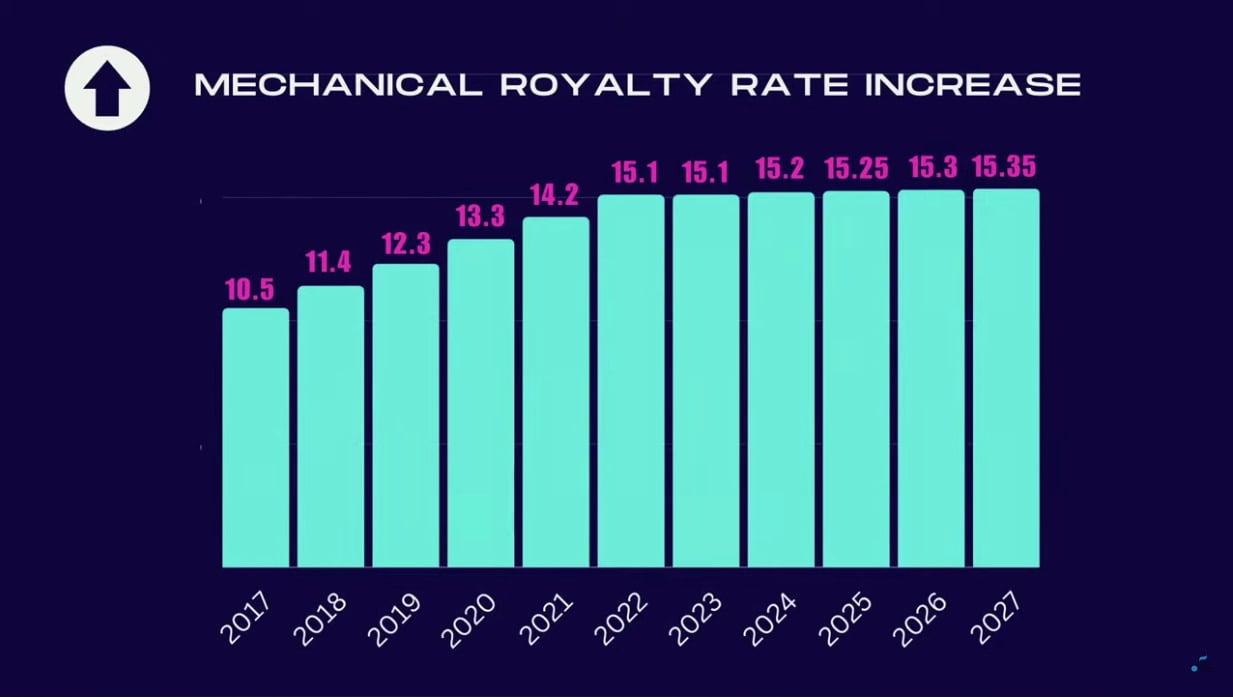

The CRB’s decision (concluding its ‘CRB III’ proceedings) meant that the headline USD mechanical royalty rate paid to publishers by music streaming services during the years 2018-2022 was retroactively increased up to a 15.1% share (see below) of those streaming services’ annual revenues.

To put it in much simpler terms: Digital services were ordered to hand over bagfuls of cash to music publishers for the retrospective use of their music in the five years from 2018-2022.

Then, in August last year, more big news: The National Music Publishers’ Association (NMPA), which fights on behalf of publishers and songwriters in CRB proceedings, announced that it had agreed a deal with DSPs for the next five years (2023-2027), which would see a new headline royalty rate of 15.35% phased in during this period.

Speaking of the NMPA… last Wednesday (June 14), the US trade body, led by President and CEO, David Israelite, held its Annual Meeting for 2023 in New York, where it presented an abundance of interesting information (such as the below slides) to its music publisher members.

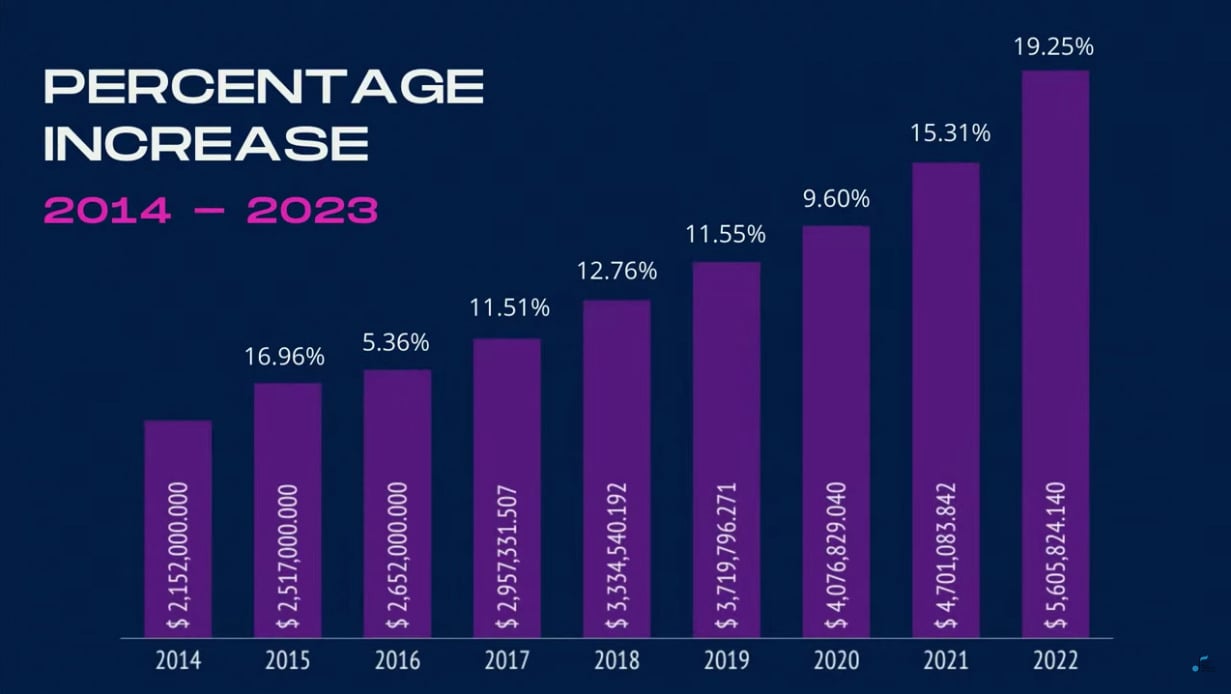

Said information included one huge stat for the music business: The overall trade revenue of US-based music publishers in calendar 2022 stood at USD $5.605 billion, up 19.25% YoY.

To put the recent growth experienced by the music publishing industry in the US into better context: That $5.605 billion figure was more than double the size of the US publishing industry’s annual revenues as recently as 2016 ($2.65bn).

As David Israelite pointed out at the NMPA meet last week, the official USD $5.605 billion revenue number for 2022 may actually get even bigger, as it doesn’t capture the as-yet-unpaid remaining amount of ‘CRB III’ money that music publishers are owed retrospectively (for that 2018-2022 period) by digital services.

Israelite confirmed that the NMPA’s revenue figure for 2022 was based on submissions from NMPA’s own membership, which he said made up 95.7% of all music publishing rightsholders operating in the States, “The highest representation of any industry for any trade association [operating] in Washington DC.”

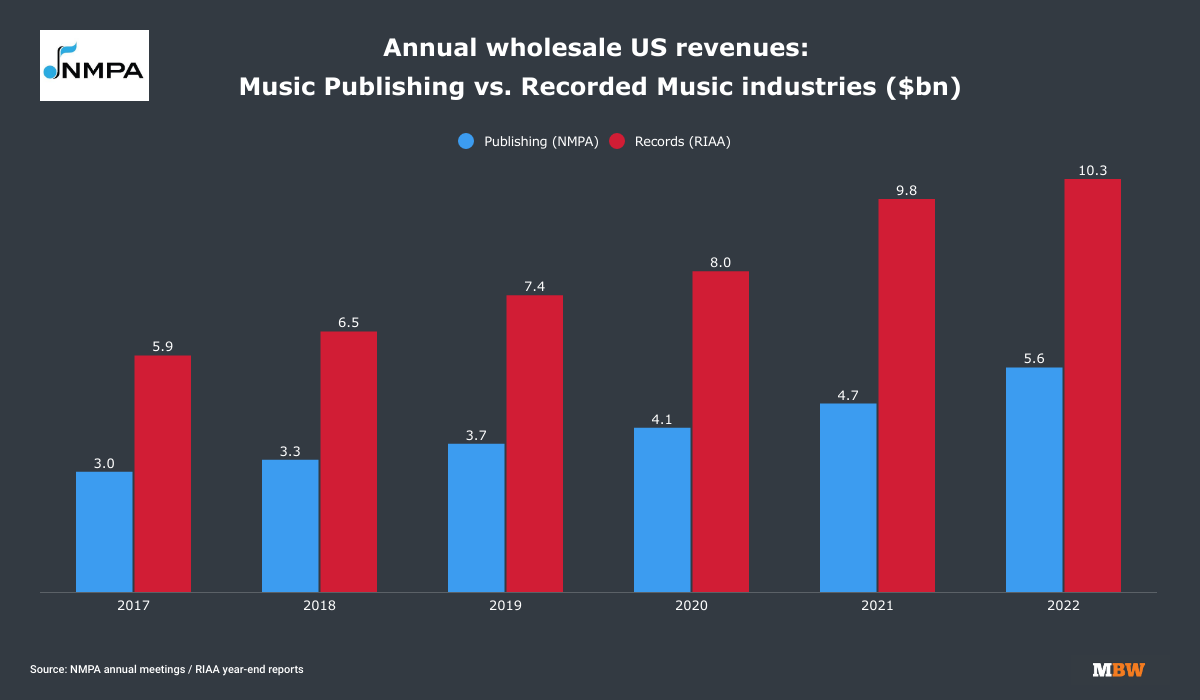

Where that USD $5.605 billion revenue figure becomes extra interesting is when you compare it to what the US record industry turned over in 2022, via data from the NMPA’s equivalent on the recorded music side, the RIAA.

Important: The revenue data reported by the NMPA is wholesale data (i.e. trade revenues reported by its members).

For a like-for-like comparison, then, we have to compare it to the wholesale number provided by the RIAA each year (i.e. the amount of money that ends up in the pockets of distributors, record labels, and artists – as opposed to the RIAA’s ‘retail’ figures, which reflect the money paid by consumers to streaming services, record stores etc.).

Here goes:

As you can see above, the $5.6 billion generated by US music publishers in 2022 was significantly smaller than the $10.3 billion generated by recorded music rightsholders, as reported by the RIAA (to one decimal place).

A particularly interesting angle here: how the NMPA (i.e. publishers’) number works out as a proportion of the record industry (i.e. RIAA’s) figure.

In 2022, the NMPA’s $5.6 billion number was equivalent to 54.4% of the RIAA’s equivalent figure.

That was the first time that the NMPA’s revenue figure stood as more than 50% of the RIAA’s wholesale figure since 2020 ($4.1bn vs. $8.0bn).

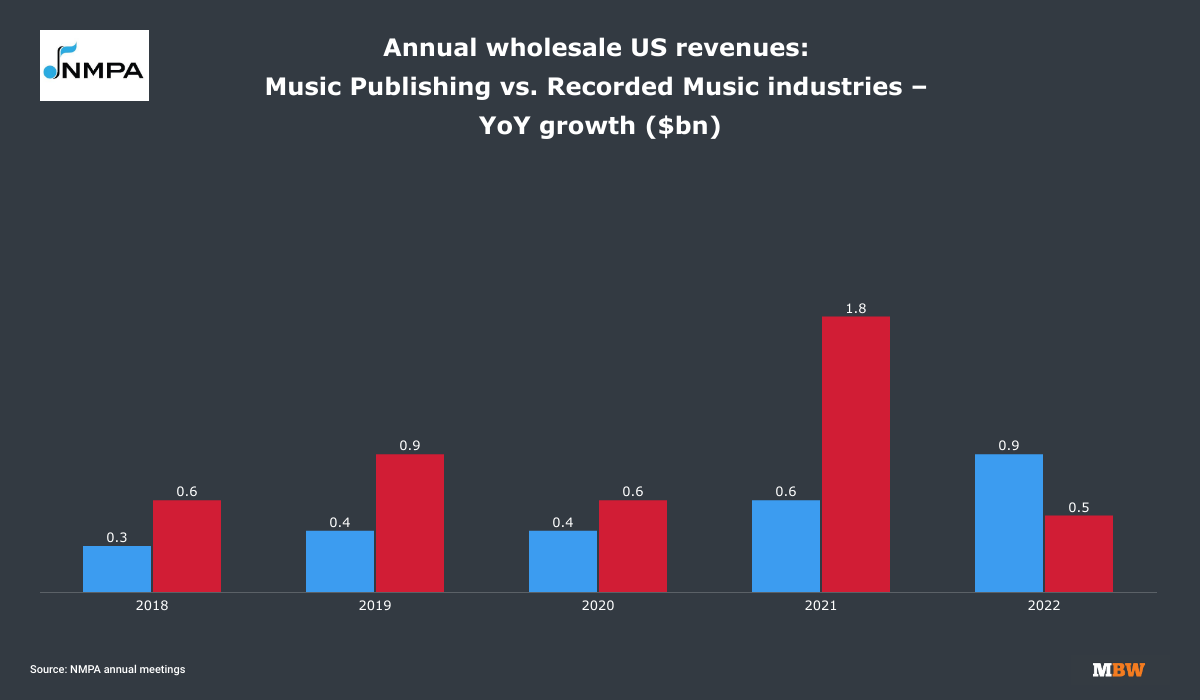

But look what happens when we compare the actual year-on-year monetary growth in annual wholesale revenues of both the US record industry and the US publishing industry in 2022:

This is something of a shock: when you boil it down to wholesale annual revenue growth, the US music publishing industry grew by a significantly larger real amount last year than the US record industry.

In fact, publishing’s growth was nearly double the size of the record industry’s: +$0.9bn ($900m) for publishing vs +$0.5bn ($500m) for records.

(Look for the reversal in the size of the blue and red bars above to see why 2022 was such an unusual year.)

What drove music publishing’s comparatively handsome growth vs. the US record industry in 2022?

There was that CRB III boost, for one thing (bagfuls of cash, remember?). There was also that post-Covid performance royalty boost to take into account.

Indeed, in 2020 and 2021, music publishing’s leading lights would have naturally seen a suppression of potential growth due to Covid lockdowns, and therefore the lack of domestic and international performance income derived from bars, clubs, restaurants, shops etc.

In 2022, in contrast, we saw record years for the likes of ASCAP and BMI – plus, as confirmed David Israelite last week, record years for private/for-profit PROs such as SESAC and Global Music Rights.

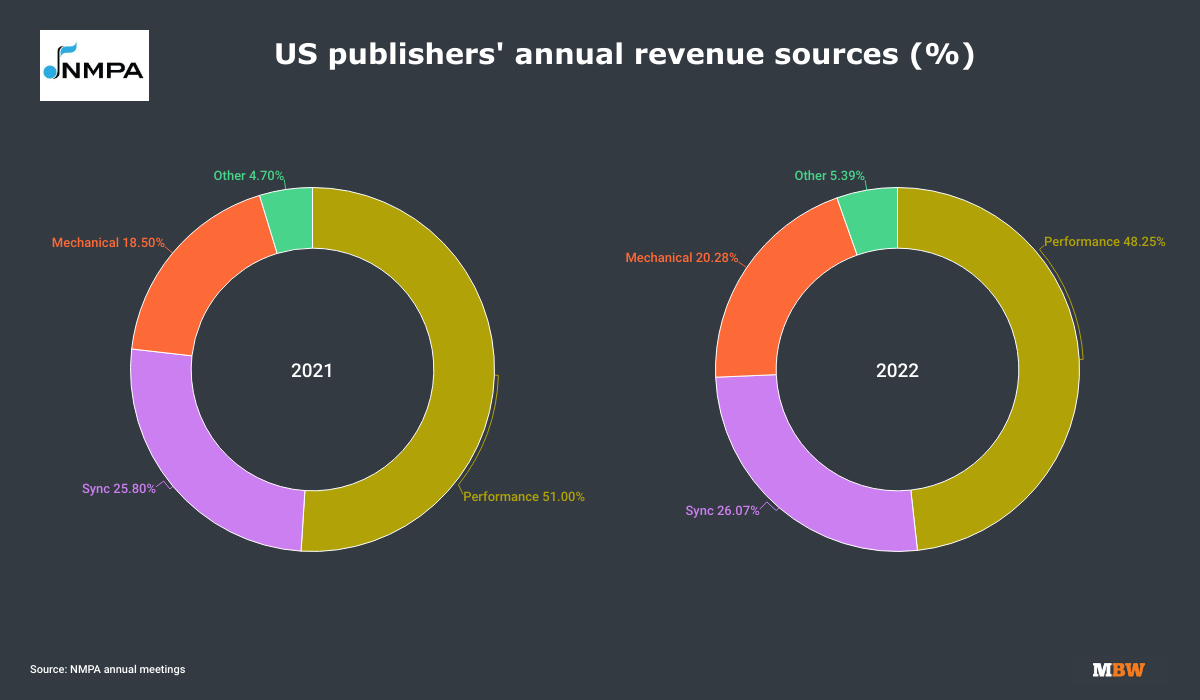

Interestingly, despite that PRO growth, for the first time in history, less than 50% of the NMPA’s annual revenue figure came from performance royalties in 2022; the category contributed 48.25% of that $5.605 billion total revenue (see below).

In addition to a CRB-powered boost in mechanical royalties (20.28%), the 2022 NMPA revenue haul also saw significant year-on-year growth in sync revenue to more than a quarter of wholesale annual music publishing industry turnover (26.07%).

In music publishing / NMPA terms, ‘sync’ revenue covers the use of music in film, advertising, games etc., but it also covers the use of music across multiple non-audio online platforms including YouTube videos and TikTok.

“Much of the work that the NMPA has done,” in legally forcing/encouraging new online platforms to license music publishing catalogs, said David Israelite last week, “has created new revenue streams [in ‘sync’] that we now enjoy today.”Music Business Worldwide