MBW’s Stat Of The Week is a series in which we highlight a single data point that deserves the attention of the global music industry. Stat Of the Week is supported by Cinq Music Group, a technology-driven record label, distribution, and rights management company.

Are the world’s biggest music markets headed towards an era where streaming growth plateaus, in the same way it has in the ‘early adopter’ Scandinavian territories?

The latest data, at least on a volume basis, suggests so.

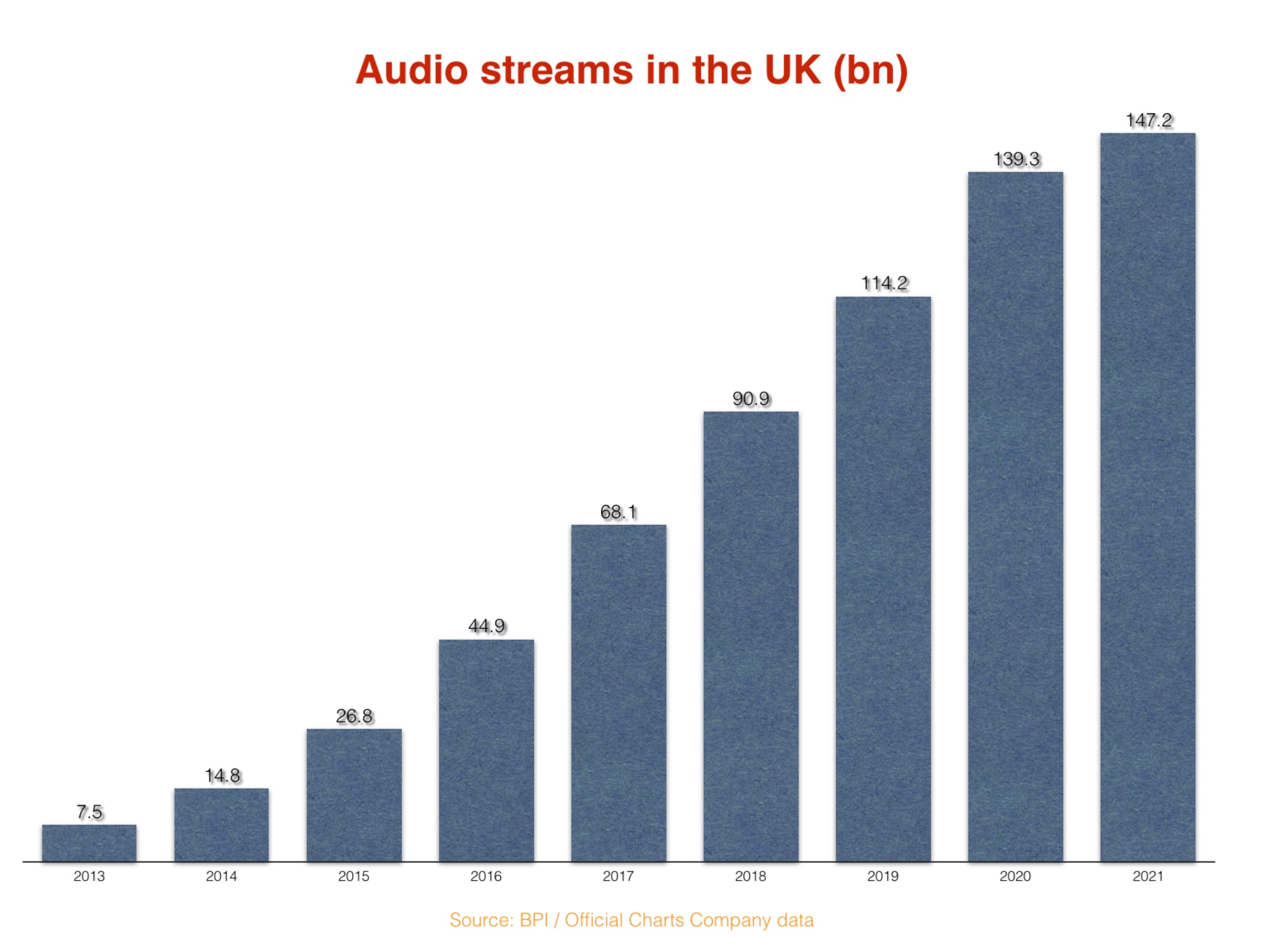

According to new figures confirmed by the UK’s official recorded music trade org, the BPI, the British market saw 147.2 billion total on-demand audio streams in 2021.

That was up by 7.9 billion – or 5.7% – on 2020’s total haul (139.3 billion).

This might sound like a lot… but when you compare it to the trends of previous years, it’s really not.

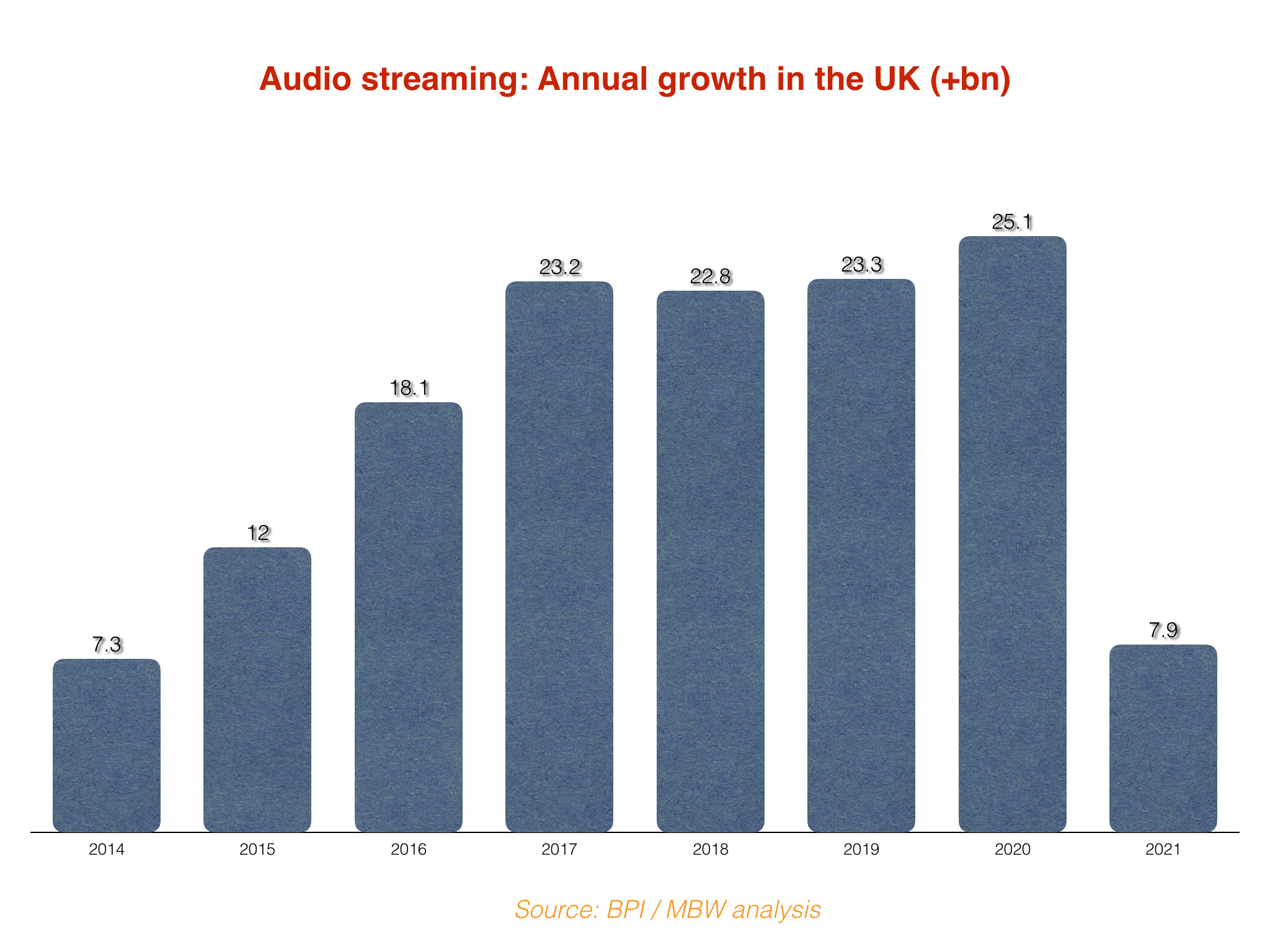

In 2020, for example, total annual audio streams in the UK rose by 25.1 billion vs. the prior year. That was actually the largest YoY increase in yearly streams in the UK’s history.

In 2019, the equivalent annual growth stood at 23.3 billion.

In fact, this audio streaming yearly growth figure was comfortably above 20 billion each year during the rampant market expansion that took place in the UK between 2017 and 2020 (see below).

By contrast, 2021’s annual growth figure (+7.9 billion) is less than a third of the size of the growth (+25.1 billion) that the UK enjoyed in 2020.

There are a few consequential details to bear in mind on these figures.

For starters, these are simply audio streaming volume numbers. The UK’s streaming revenue numbers for 2021 will be released later this week (on a retail basis) by the Entertainment Retailers’ Association (ERA).

Due to a number of factors – not least what percentage of streams come from paid-for accounts vs free accounts – this streaming revenue figure doesn’t always follow the trends of the streaming volume data.

For example: In 2020, annual audio streaming volume in the UK (as previously mentioned) grew by the biggest ever amount (+25.1 billion).

However, audio streaming revenue on a retail basis couldn’t match this growth: UK subscription streaming revenue, according to ERA, grew by a smaller amount in 2020 than it did in each of 2019, 2018, and 2017.

Stat Of The Week: Official market numbers from the BPI show that the UK’s total audio streaming tally in 2021 was up by 7.9 billion year-on-year. That growth figure was less than a third of the size of the equivalent growth number from 2020.

Something else to consider about the latest BPI numbers: Because of the way 2021 was structured, the year had 52 ‘chart weeks’ in it (following the global industry standard, the UK’s charts are announced each Friday).

The BPI uses these ‘chart weeks’ to obtain data (via the Official Charts Company) about the market every seven days, which culminates in its annual numbers.

However, 2020 had 53 of these ‘chart weeks’, meaning the YoY comparison is slightly skewed in that year’s favor.

Or to put it another way: The average amount of audio streams in the UK per chart week in 2020 was 2.63bn, while in 2021 it was 2.83 billion.

As such, with an additional ‘chart week’ added in – i.e had last year been a 53 ‘chart week’ year like 2020 – the UK market would have ended 2021 with around 150 billion annual audio streams.

That would have meant a 9.9 billion annual YoY rise in total audio streams… still way behind the 25.1 billion growth seen in 2020.

What can we glean from all of this?

Well, the UK is a more mature streaming market than the US: The UK, for example, saw Spotify launch on its shores in 2008, while Daniel Ek‘s market-leading platform didn’t land in the States until 2011.

As such, the UK – as the world’s third biggest recorded music market – is a useful bellwether for what may be coming down the road for the world’s No.1 market in the US.

Right now, the evidence suggests that what’s coming down the road is a significant slowdown in streaming volume (and potentially streaming revenue?) in the United States.

All of that being said, remember this: The recorded music divisions of each of the three major music companies – Universal Music, Sony Music and Warner Music – enjoyed double-digit growth throughout 2021, mainly fuelled by streaming revenue increases.

In other words, the brakes might be about to be slammed on YoY streaming increases in the globe’s biggest music markets… but the globe’s biggest music companies are still finding plenty of growth worldwide.

Also, let’s not forget that the United States saw a huge jump (+27%) in YoY growth for its recorded music industry revenue in the first half of 2021, according to the RIAA.

US music streaming-specific revenue, according to RIAA, was up 26% YoY in this H1 2021 period, generating $5.9 billion for the industry. That’s almost $1 billion per month.

With the latest UK figures in mind, it will be interesting to see if the US market can keep up anything like this growth in 2022… and beyond.