Hipgnosis Songs Fund (HSF), the UK-listed entity founded by Merck Mercuriadis, now owns a music rights catalog worth over USD $2.5 billion.

That’s according to an independent valuation revealed within Hipgnosis’ new interim financial report, covering the six months to end of September 2021.

The report reveals: “As at 30 September 2021, [our] Portfolio comprises of 146 Catalogues, 65,413 songs, with an aggregate fair value of $2.55 billion (as determined by the Independent Portfolio Valuer).”

The valuation of that catalog keeps on going up and up, just as multiples paid across the music industry for rights continue to increase.

According to HSF’s report, its latest independent valuation placed an aggregate multiple of 19.03-times historical annual net publisher share income on the company’s rights portfolio. (i.e. The valuer believes that the current M&A music market would pay a 19-times multiple for HSF’s rights should they hypothetically be up for sale.)

That 19.03-times multiple, says the interim report, is significantly higher than the blended acquisition multiple of 15.93-times net revenue that HSF has paid, on average, for the rights it owns today.

Indeed, at the end of March 2021, Hipgnosis Songs Funds’s catalog – then of 64,555 songs – was valued at $2.2 billion.

That $2.2 billion figure was based on a 17.96x multiple of historical annual net publisher share income.

Since that point (i.e. in the six months from end of March to end of September 2021) HSF has acquired rights to 858 songs.

It’s done so via eight separate acquisitions, costing a total consideration of USD $260 million.

The firm has used that money to snap up rights to songs by the Red Hot Chili Peppers, Christine McVie of Fleetwood Mac, Rhett Akins, The Monsters & Strangerz (Stefan and Jordan Johnson), Elliot Lurie, Ann Wilson and Kaiser Chiefs.

Hipgnosis says that the value of HSF’s catalog rose 3% on a like-for-like basis in the six-month period to end of September 2021, which it said was due to: “An increase in expected performance income in 2023 as [our] Independent Portfolio Valuer is now forecasting a stronger bounce back from COVID-19 to pre-pandemic levels,” as well as, “An increase in streaming growth rates to reflect the continued growth in paid subscribers in excess of expectations.”

Hipgnosis Songs Fund has also revealed some key revenue data in its new interim report.

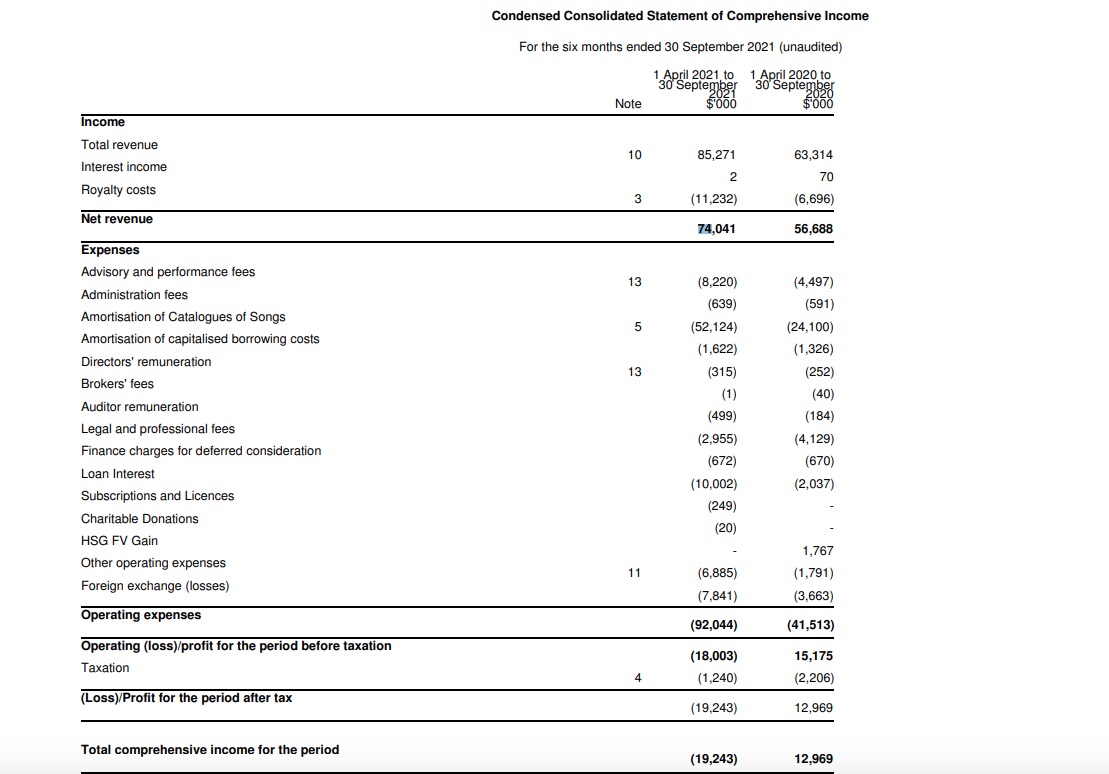

In the six months ending September 2021, the company generated net revenue of $74.1m, up 31% year-on-year.

HSF primarily pinned that revenue growth on the catalog acquisitions it made over the prior 12 months.

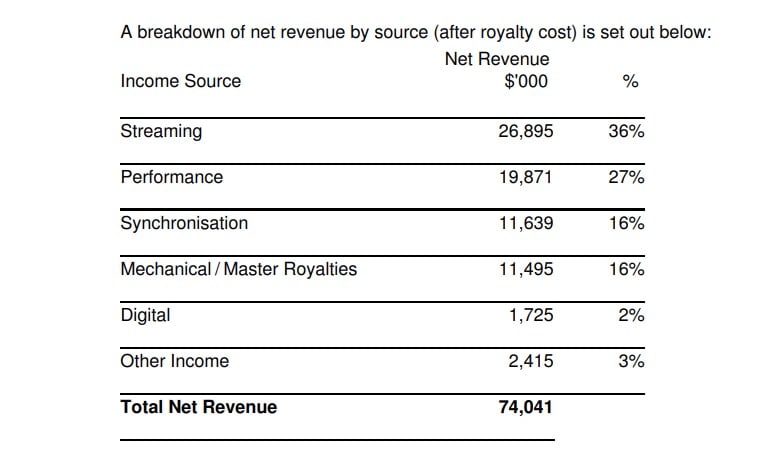

Of that $74.1 million, some $26.9 million (36%) came from streaming platforms, while $19.8 million (27%) came from performance royalties, and $11.6 million (16%) came from synch licensing. (See below for a full breakdown.)

As a result, HSF’s current rights portfolio now looks firmly on course to post around $150 million annually.

Other headline numbers for Hipgnosis Songs Fund in the half-year period (to end of September 2021) include:

- EBITDA for the six months ended 30 September 2021 increasing by 16.2% to $54.6 million (six months ended 30 September 2020: $47.0 million);

- Operative NAV (net asset valuation) increasing by 2.5% to $1.7242 per share over the six month period (31 March 2021: $1.6829);

- An operating loss of $18.0 million, largely due to expenses related to the Amortisation of Catalogues (-$52.1m) and related to loan interest repayments ($-10.0m)

Merck Mercuriadis, Founder of Hipgnosis Songs Fund Limited and Hipgnosis Song Management Limited said: “It’s incredible to believe we are half way through our fourth year! The last nine months, including this Interim reporting period from 1 April to 30 September 2021, have been a very important and exciting time in our maturation.

“I am delighted to report year-on-year net revenue growth of 31%, EBITDA growth of 16% and most importantly NAV growth of 2.5% over the past six months driven by an increase in the fair value of our Catalogues. This takes our Total NAV Return delivered since IPO less than 4 years ago to an incredible 46.7%.”

Added Mercuriadis: “Whilst we are in an incredibly strong position with our Catalogue of iconic songs, this period has been challenging. As we have previously stated, the time lag between the consumption of songs and the royalty statements being processed, which is the point at which we recognise revenues, means that the impact of COVID-19 is now being fully felt within these results. In particular, and along with the wider music industry, the closure of live music venues, pubs, bars and restaurants during various lockdowns has impacted the like-for-like performance earnings of our Catalogues during this period.

“As we look forward, despite the emergence of the Omicron variant of COVID-19, we continue to see a promising outlook for the music industry and our Catalogues.”

Merck Mercuriadis

“Our vintage Catalogues have made up for a fall in their performance earnings with outstanding streaming performance earnings as consumers turned to classics during lockdown. Despite being in one of the most challenging economic and operationally difficult times of our lives we are delighted that we were still able to deliver a fully covered dividend – a validation of the reliability of songs as an asset class. As we look forward, despite the emergence of the Omicron variant of COVID-19, we continue to see a promising outlook for the music industry and our Catalogues.

“Over the last 6 months we have seen live venues are fully booked until 2023, pubs, bars and restaurants are full and streaming growth continues to exceed expectations. This optimism in growth is shared by our independent valuer who has increased the future earnings trajectory for our Catalogues in their valuation models resulting in 3% growth in the fair value of our Catalogues. However, we must be proactive and not take this recovery for granted, something highlighted by the continued uncertainty caused by the Omicron variant of COVID-19.

“Therefore, in order to ensure our Catalogues outperform, no matter the wider market conditions, we continue to increase our Song Management efforts. We have hired experts in all parts of Song Management as we explore every opportunity to innovate and maximise earnings from our songs. Our focused and conscientious model provides the bandwidth to be able to manage great songs responsibly, as we maximise their revenues while enhancing their long-term legacies.”

After raising a $215 million sum in June/July this year via a share placing, Hipgnosis Songs Fund pledged to its investors that it wouldn’t be raising any more capital on the public markets until at least Q2 2022.

Since that point, Merck Mercuriadis has announced a new private $1 billion fundraise from Blackstone.

That money will be fuelling a new Hipgnosis-affiliated fund – Hipgnosis Songs Capital – run separate to Hipgnosis Songs Fund.

In addition, Blackstone has made an investment into Mercuriadis’ investment management firm, Hipgnosis Song Management.

When Hipgnosis Songs Fund is able to raise more funds next year, says Mercuriadis, it will – so long as it has the requisite money – be able to obtain a 20% stake in any rights acquired by Hipgnosis Songs Capital.Music Business Worldwide