Hipgnosis Songs Fund has today (July 14) published its full-year financial results for the 12 months to end of March.

Before we dig into that, and our headline above, the now-standard bit of housekeeping:

- Hipgnosis Songs Fund (HSF) is the publicly-traded UK fund that IPO’d on the London Stock Exchange in 2018;

- Its investment advisor is Hipgnosis Song Management (HSM), which is run by Merck Mercuriadis and his team;

- Blackstone last year privately invested a billion US dollars in a new Hipgnosis fund, Hipgnosis Songs Capital (HSC), in addition to making an undisclosed investment in Hipgnosis Song Management;

- The latter company (HSM) is not only tasked with finding catalog acquisition opportunities for both HSF and HSC, but also with maximizing returns from their owned catalogs vis sync, marketing, streaming etc.

What was particularly interesting about Hipgnosis Songs Fund (the UK-listed entity) in the second half of its latest fiscal year? It didn’t spend a single penny on catalogs.

Having revolutionized the catalog-acquisition market since 2018 – and been a major catalyst in Wall Street’s understanding of music as an “asset class” – HSF stood still (acquisition-wise) in the six months to end of March 2022.

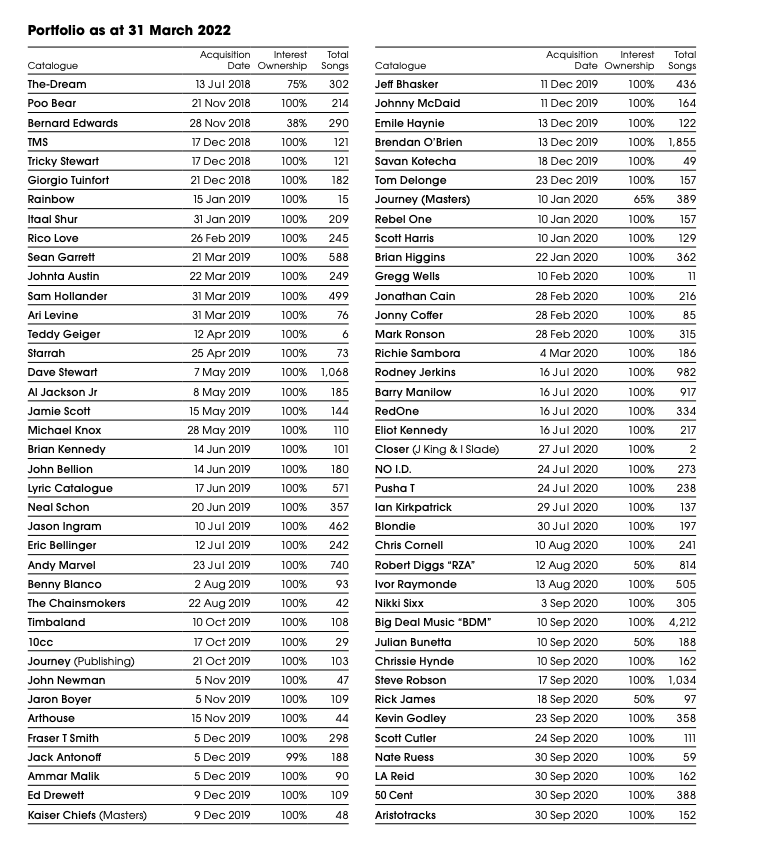

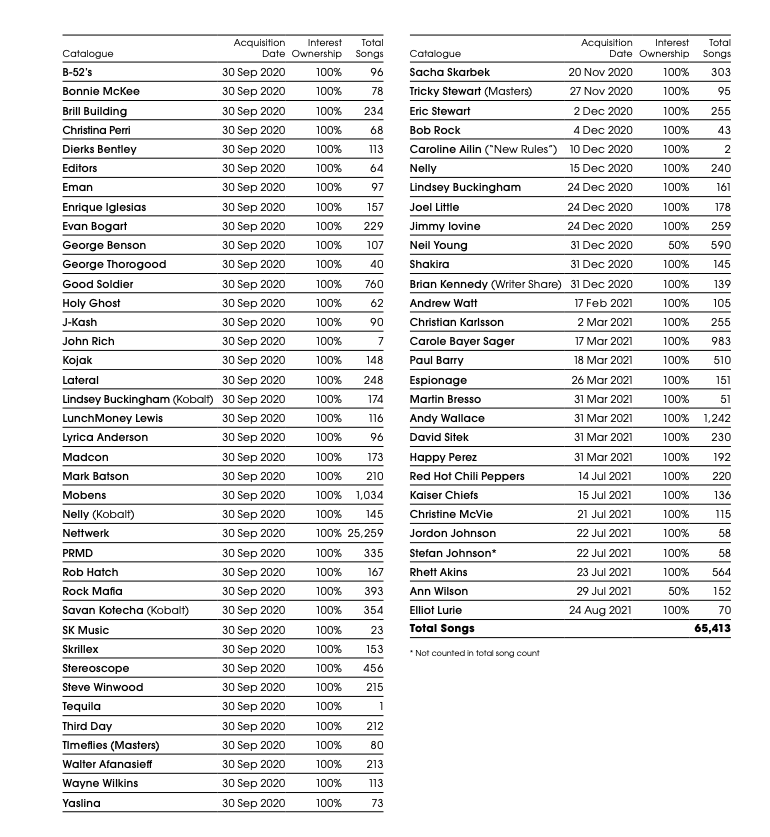

How do we know? Because in its half-year fiscal report (covering the six months to end of September 2021), published last year, Hipgnosis confirmed it owned 146 Catalogues across 65,413 songs.

And today, in its full-year fiscal report (covering the 12 months to end of March 2022), Hipgnosis confirms that it owns… 146 Catalogues across 65,413 songs.

None of this is a surprise: As MBW explained to you last year, Hipgnosis Songs Fund raised $215 million via the public markets in July 2021 (which it then spent on catalogs from artists/writers like the Red Hot Chili Peppers, The Monsters & Strangerz, Christine McVie and more).

After that raise, however, the company pledged it wouldn’t raise any more capital on the public markets until at least Q2 2022 (a period we now find ourselves in).

Meanwhile, debt-wise, HSF appears fully leveraged under the current fiscal rules governing the running of its business.

(By contrast, Hipgnosis Songs Capital, the Blackstone-backed private fund, has been busy buying catalogs by the likes of Leonard Cohen and Justin Timberlake for nine-figure sums in recent months.)

So here’s the thing: For once, for now, the interesting aspect about Hipgnosis Songs Fund (in the six months to end of March) isn’t what it bought; it’s how much it grew in value.

According to an independent valuer quoted in HSF’s financial filings (and as reported by MBW last year), Hipgnosis Songs Fund’s portfolio of copyrights was worth USD $2.55 billion at the end of September 2021.

Six months later (as per HSF’s new annual report) and that same independent valuer now says that – as of end of March 2022 – Hipgnosis Songs Fund’s portfolio was worth $2.69 billion.

In other words, over the course of six months, Hipgnosis bought nothing at all… and still grew in value by $140 million.

Explains Hipgnosis Songs Fund founder, Merck Mercuriadis, in HSF’s new annual report: “In the second half of our fiscal year 2021/2022, as most global restrictions have eased and market growth has returned, we have now also shown that our acquisition strategy and disruptive Song Management approach leaves us well-positioned to outperform.

“Our strategy to acquire only the most successful and culturally important Songs, including 67 of the 271 Songs that have been played over 1 billion times on Spotify, has delivered like-for-like Streaming growth of 19% in the second half of our fiscal year alone.”

“In the second half of our fiscal year 2021/2022, as most global restrictions have eased and market growth has returned, we have now also shown that our acquisition strategy and disruptive Song Management approach leaves us well-positioned to outperform.”

Mercuriadis adds that this streaming growth “outperformed our Independent Valuer’s expectations, and together with the first time recognition of the value of revenue generated from the now established digital lifestyle platforms that have emerged, led to an annual increase in our Operative NAV of 9.9%”.

One key factor in the growth of Hipgnosis Songs Fund’s value: The firm’s annual report says that it saw a “20% increase of formal synch licences approved in the 6 months to [March 31, 2022] versus the first half of the financial year”.

A bunch of other financial information is revealed in Hipgnosis Songs Fund’s new annual report, too.

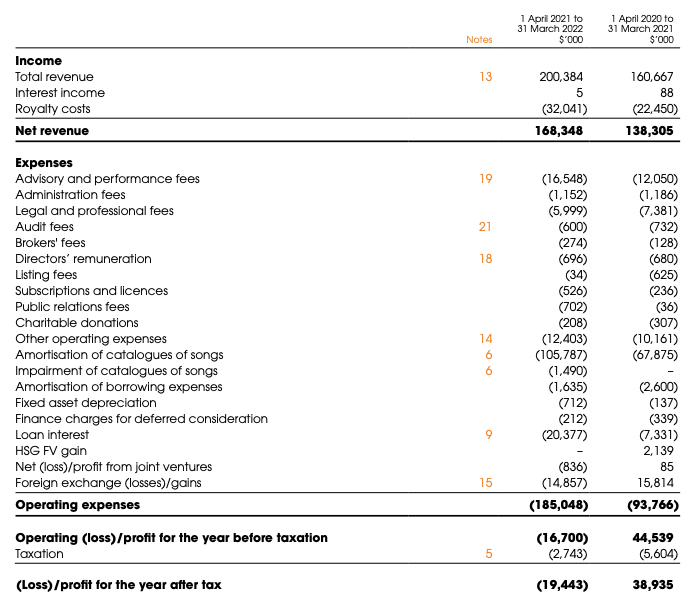

Across the full year (to end of March 2022), HSF’s gross revenue increased by 24.7% to USD $200.4 million (31 March 2021: $160.7 million) partly due to the catalogue acquisitions the firm executed in the first half of its fiscal year.

Net revenue of $168.3 million increased by 21.7% year-on-year (31 March 2021: $138.3 million), following royalty cost deductions of $32.0 million (31 March 2021: $22.5 million).

And EBITDA increased by 21.8% to $129.9 million (31 March 2021: $106.7 million).

HSF posted an operating loss of $16.7m in the year (see below).

Added Mercuriadis: “Over the last four years we have acquired an incomparable portfolio of some of the most successful and culturally important Songs of all time, now valued at $2.7 billion. The unique strength of our Catalogue is demonstrated by the 9.9% increase in the Operative NAV to $1.8491 per share, as reported by our Independent Portfolio Valuer, and a Total NAV Return of 14.2%. This is largely driven by our iconic Songs outstripping the general market growth in Streaming, particularly in the second half of 2021, providing validation for our investment strategy.

“As we look forward, we continue to expect strong global revenue growth driven by the continued adoption of paid-for Streaming. Despite the macro-economic environment, the attractiveness of the music Streaming proposition continues to grow.

“It is the lowest-cost entertainment subscription service and, with its offering of a near complete repertoire of global music, provides the most comprehensive offering of the on-demand, entertainment subscription services.

“This view is shared by the leading voices in the sector, including Goldman Sachs, who recently upgraded their double-digit annual growth forecast through to 2030 in their gold standard Music In The Air: Music still sounds good in a macro downturn; raising global industry forecasts report.”

Continued Mercuriadis: “With clear evidence of a strong recovery in global Performance income, the recent CRB III determination to increase Streaming royalty rates for songwriters, and potential for further improvements in the upcoming CRB IV determination, all in addition to the extremely strong growth in Streaming, I believe we are looking forward to very attractive market conditions.

“Given our incomparable collection of iconic Songs, I believe Hipgnosis is perfectly placed and will continue to deliver excellent returns for our Shareholders.

“Thank you to our Shareholders for your incredible support, our Board, brokers and the incredible songwriters who have entrusted us with their incomparable Songs.”

Below, taken from the Hipgnosis Songs Funds annual report – which you read in full here – you can see the entirety of catalog acquired by the company to date.