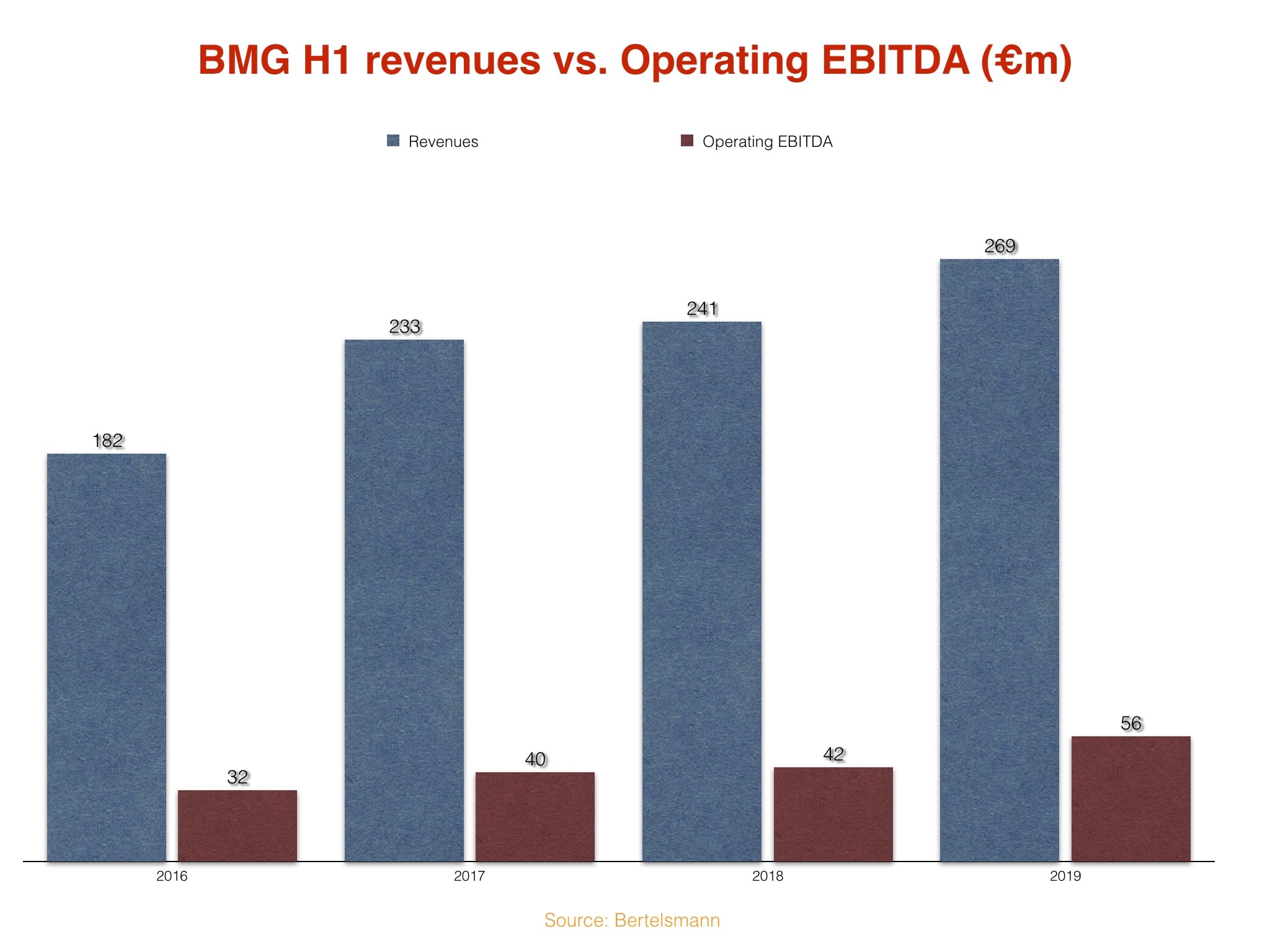

BMG is on course to turn over more than $600m in 2019, after seeing its midyear revenues rise 11.4% in the first six months of this year.

The company’s CEO, Hartwig Masuch, tells MBW that Bertelsmann-owned BMG now expects to generate one billion dollars per year as soon as 2022.

Yet, as the old saying goes, revenue is vanity… but profit is sanity. And, as excited as he would be to see BMG’s annual sales hit ten figures, Masuch is determined to keep his focus on the latter measure.

The Berlin-based exec acknowledges that “a [$1bn turnover] is definitely a target we set ourselves over the next three to five years”, but notes that a number of market factors – including a “big crisis” in industry valuations – could affect BMG’s fiscal journey, whether positively or otherwise. (For example, if industry valuations suddenly sink, BMG might be able to snap up some tasty music rights at attractive prices, accelerating its revenues.)

Importantly, Masuch adds: “We won’t be losing any sleep if, after five years, our revenues aren’t at [$1bn] but our profit [margin] stays where it is today.”

His point: BMG is, increasingly, a more profitable company. Its revenues might have risen 11.4% year-on-year in H1 2019 (to €269m/$305m), but the company’s operating EBITDA margin shot up even faster, by 16.7% (to €49m/$56m) in the same period.

This means that BMG’s operating EBITDA margin now sits at a very healthy rate of 18.2%. Impressively, BMG has secured this level of profitability despite basing its business on giving far more money to artists, as a rule, than traditional major label deals.

Typically, BMG offers a recorded music deal which sees artists receive a 75% share of revenue, with 25% retained by the company. This split buys the artist core services like royalty collection, product management and accounting, while other label services – including marketing spend, PR and physical distribution – are layered on via optional additional costs.

Masuch, who credits BMG’s expanding profit margin to the “scalability” of his company’s publishing and recordings catalog as streaming grows globally, told MBW: “One of the most important achievements in the past 10 years was that we were able to transform the music industry cost structure that is necessary to bring artists global success.

“That’s why you see us growing our EBITDA without [major] acquisitions on a [typical artist deal rate of] 75/25 or 70/30. We’re able to keep a very rational cost base, and still participate in all the glory and fun of the modern music industry.”

If you didn’t pick up on it, Masuch appears to be questioning the cost structure of the major music companies – whose EBITDA margins have, in the past few years, weighed in lower than BMG’s (alongside, it should be noted, far higher annual revenues than the Bertelsmann company’s).

Says Masuch: “The question for the shareholders [of major music companies] is this: ‘Hey, what was the rationale for the in-many-ways irrational cost structure of the music industry [in years gone by]?’ Well, one part of it was that you needed incredibly talented [label] heads to break new artists.

“at the end of the day, there will always be a No.1, whether you pay your executives $5m a year, or whether you pay them $500,000.”

Hartwig Masuch, BMG (pictured)

“But the ratio of that part of the business [ie. the blockbuster global superstar business] is getting smaller as a percentage [of the overall record industry]: and, at the end of the day, there will always be a No.1, whether you all spend $2m [on marketing] and pay your executives $5m a year, or whether you spend less [on marketing] and pay them $500,000.

“The logic of that structure will be increasingly questioned. Because the costs you incur there, ultimately, end up being the costs of artists.”

Masuch believes the fiscal model of music’s biggest companies will increasingly face pressure in the modern industry, as artists are able to demand more lucrative (i.e. BMG-style) splits – and/or, indeed, take back ownership of their rights following copyright reversions.

He admits that, internally, when his frontline recorded music heads look to approve advances for their biggest deals, he applies a simple test of logic: how many streams will it take for BMG to earn its money back?

This idea makes for an interesting thought experiment when you apply it to the salaried leaders of the blockbuster music industry.

For example: let’s take the $5m wage for the hypothetical high-rolling label executive cited by Masuch above. Applying a very broad per-stream Spotify royalty payout rate of $0.004 for recorded music industry rightsholders, it would take 1.25bn streams in order for a record company to generate $5m per year.

(For context: according to Kworb, only six tracks have ever topped 1.25bn plays on Spotify: Ed Sheeran’s Shape Of You; Post Malone’s Rockstar; The Chainsmokers’ Closer; Drake’s One Dance; Drake’s God’s Plan; and Camila Cabello’s Havana. Although these are obviously all single tracks on a single service.)

Now consider the fact that Masuch believes, pretty soon, most record industry artist deals will start to mirror BMG’s 25/75 or 30/70 splits in favor of the acts themselves.

In this case, with a 30% royalty margin, an executive on $5m a year would need to bring in over 4 billion streams just to square off their own annual salary – let alone the advances they pay out over the same 12 months in order to attract artists (whose deals they hope will become profitable).

Masuch has a further point to make here, too.

“In my view, some of the most talked-about companies [in music] haven’t made enough effort to [adjust their business models]. The shit will hit the fan sooner rather than later!”

“The deals for big hits today are much more aggressive [in terms of artist splits] than people think,” he says.

“We all know the cost of that [frontline] part of the business will drastically go up as artists have a higher demand on the share of royalties they get, and you have to translate that into your business model.

“In my view, some of the most talked-about companies [in music] haven’t made enough effort to do this so far. The shit will hit the fan sooner rather than later!”

Specifically, what kind of frontline artists deal structures is Masuch referring to? His answer leads on to his other big concern about the modern music business – the confidence of investment analysts in the bright future for record labels, and the knock-on effect this has on certain huge valuations.

Masuch shares the bullishness of the likes of Enders and even Goldman Sachs on the future of streaming, both in terms of the format’s global reach, and the number of subscribers who might pay for services like Spotify in the decade ahead.

But, he says, he doesn’t believe this volume growth will necessarily translate into the profits of music companies whose current catalog rights are, generally speaking, based on a deal split that sees them retain the vast majority of royalties.

“A lot of rights from big catalog deals will revert to artists; and those deals won’t renew with a headline royalty rate of 25% minus packaging deductions; they will clearly change so [the artist earns] above 50% of digital income.”

“I don’t agree that you can convert topline [streaming] growth forecasts one-to-one with the old metric of [a record company’s current] contribution margin and arrive at their future EBITDA,” says Masuch. “A big part of today’s business is driven by catalog and established recordings. There is a large question mark over when those historical deals terminate or have legal reversions, because when those things happen you’ll see an incredible rise in royalty payments [to artists and away from their labels].

“A lot of rights from big catalog deals will revert to artists; and those deals won’t renew with a headline royalty rate of 25% minus packaging deductions; they will clearly change so [the artist earns] above 50% of digital income. This factor is totally ignored right now in almost every analysis you read, because nobody out there owns as much as they pretend to own.”

As for BMG, it will increasingly become known as a record company itself.

Masuch expects BMG’s recordings business to tip the scales and become a bigger annual earner than its publishing operation across its business “in the next 24 months, at the latest”.

Masuch adds: “It takes some time to introduce a new paradigm into the way you do business like BMG has done – and we are now seeing exponential interest in working with us. I’m surprised about the incoming interest we are [increasingly seeing] from major recording artists.”

According to internal data seen by MBW, the company saw 56% of its revenues in H1 2019 – or $171m – derived from digital formats.

BMG’s big revenue-generating recorded music projects in the first six months of 2019 were, in order: (i) Avril Lavigne’s Head Above Water; (ii) Kontra K’s Sie Wollten Wasser Doch Kriegen Benzin; (iii) Jason Aldean’s Rearview Town; (iv) Dido’s Still On My Mind; and (v) Keith Richards’ Talk Is Cheap (reissue).

The firm’s big publishing successes included breakout British star Lewis Capaldi, in addition to Juice WRLD and Bring Me The Horizon.

In a memo sent to colleagues following the announcement of BMG’s results, obtained by MBW, Masuch noted that the company confidently expects its second half 2019 revenues to outperform its H1 results.

Said Masuch: “Delivering for artists and songwriters is why we are here. That is our brief. Unlike some, we are not here to maximize our share price: we are privately owned; we have no ‘share price’.

“We believe music companies should exist to serve artists and songwriters. The music industry would be a much healthier business if everyone held this view.”

“We are not here to buy songs and recordings and then ‘flip’ them, nor are we trying to create a technology ‘unicorn’. Instead we work with artists and songwriters to optimize their careers and their income.”

He added: “We don’t believe that artists and songwriters exist for the convenience of music companies. We believe music companies should exist to serve artists and songwriters. The music industry would be a much healthier business if everyone held this view. As long as they do not, however, this can only work to our advantage.”

One area BMG isn’t likely to be focusing its attention for the time being is major-league rights acquisitions, focusing instead on organic growth.

In his internal note, Masuch referenced recent venture capital and private equity-driven buyouts across both recorded music and publishing which, in his view, are driving multiples to a level which may end up disappointing certain investors.

“Between 2009 and 2016 when we made 100 significant acquisitions, virtually no one else was buying music assets,” he said. “Now we are in the middle of a feeding frenzy which has pushed prices in some cases beyond all reason, a game BMG is unwilling to play.”Music Business Worldwide