The following MBW op/ed comes from Kim Bayley (pictured), CEO of the UK’s Entertainment Retailers Association, whose members include the likes of Amazon, Deezer, HMV, SoundCloud, Spotify, and YouTube. ERA recently released its 2021 Yearbook, packed with data about the UK entertainment market.

Like most things in life, timing really is everything. Just contrast the experience of someone who started their career in music in 2013 compared with their predecessors who started in 2001.

The 2013 cohort have so far enjoyed seven straight years of growth while their unfortunate 2001 counterparts suffered the opposite for 12 years, a dozen years of store closures, redundancies and the constant fear that it might be them next.

The lucky new starters of 2013 are enjoying buoyant times, music is the darling of investors and they could be forgiven for feeling things have never been better.

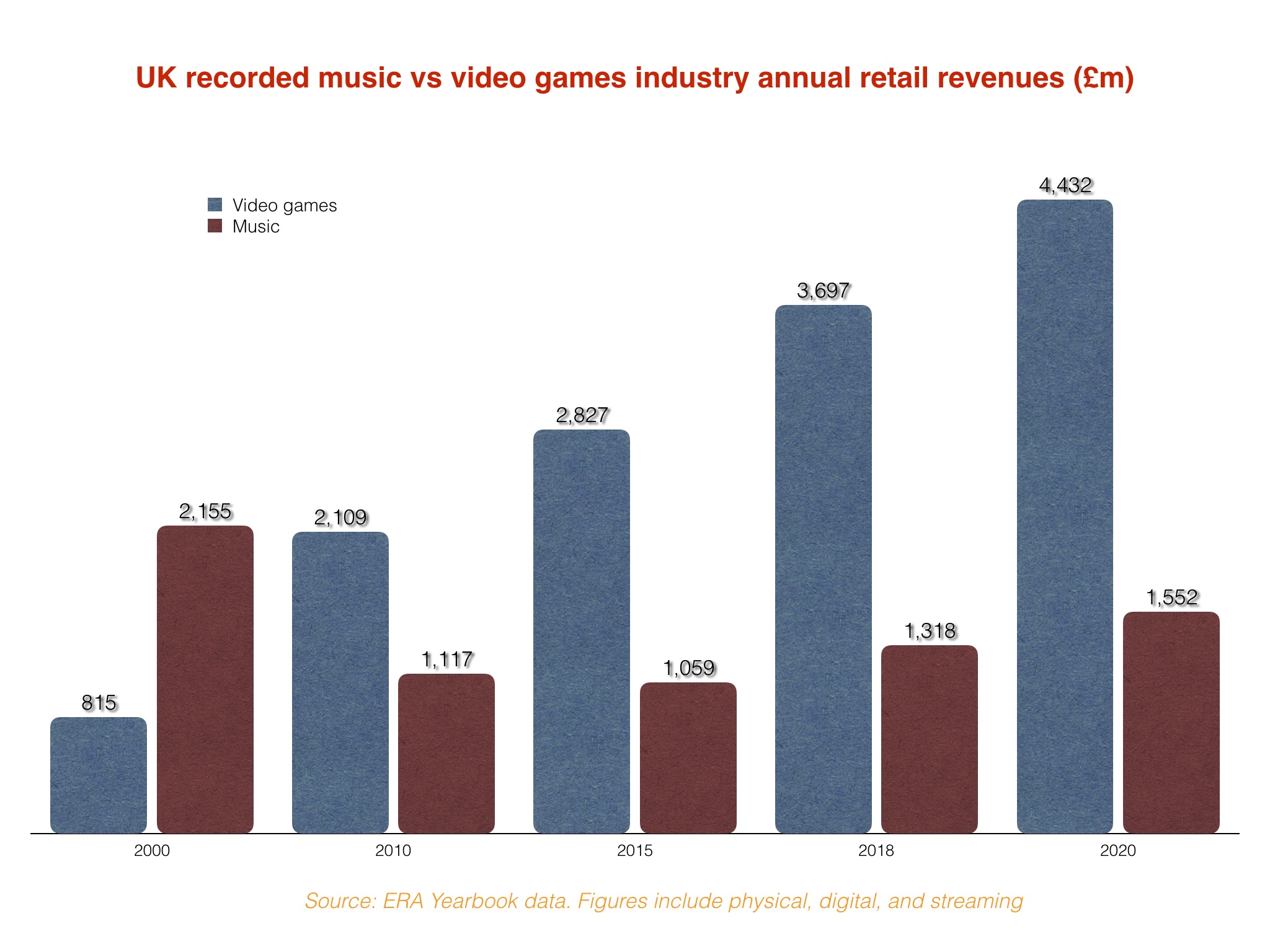

Of course, as their elders could tell them, they would be wrong. Despite the last seven years of growth during which UK recorded music revenues [on a retail basis] have grown by 50%, music is still way off its 2001 peak of £2.2bn. Adjusted for inflation, it would have to be at £3.7bn to equal its record high.

Such comparisons might be uncomfortable amid the celebration of streaming services’ undoubted achievement in driving music sales. It is tempting to dismiss them as unrealistic given the scale of the disruption to traditional music sales wrought by the internet.

But there is a real world comparison we can make as to how to deal with technological change really successfully, and how new formats can be additive rather than substitutional. And luckily we don’t have to look far – it’s a sector which targets fundamentally the same market, and has done so outrageously well over the past two decades: video games.

The UK games market in 2020 was worth £4.4bn, nearly three times as much as music. What’s all the more remarkable is that in 2000, it was worth just £815m, less than half the value of music at the time.

To put it in context, if the UK recorded music industry had grown at the same rate as games over the past two decades, it would now be worth not £1.5bn, but £11.7bn!

So what lessons can we learn from that rise and rise of games? How can we make music as successful as the games market?

Here’s just five potential areas to explore. The following points make no claim to be exhaustive, but cover some of the most glaring contrasts…

1) Embracing technology

The evidence of history is that every great new technology ultimately expands the market for entertainment. It is also full of examples of established players seeking to thwart the rise of new means of consuming content.

While music lost vital years fighting the internet, the games business ruthlessly embraced it, devising new formats of gaming to embrace its possibilities.

2) Diversity of channels

Back in the Nineties, there was a determined effort in the music business to create a new format to sit alongside the compact disc with PolyGram – the then-biggest UK music company – supporting DCC, the Digital Compact Cassette, and Sony backing the Minidisc.

The rationale was explicit – “We have to avoid becoming a single format market at all costs”: they realised that competition between formats creates growth. The increasingly overwhelming dominance of premium streaming means music is well on its way to being effectively a single format business again.

Contrast that with gaming where console games sales are growing again alongside a bewildering number of channels and platforms from direct to console downloads to Roblox to mobile apps, to Twitch each with their own hits.

3) Proactive marketing to all demographics

From its origins as a pursuit to be enjoyed only by the obsessive – usually male – gamer nerd to be reached through gamer media, the gaming industry has embraced marketing channels which reach all demographics.

Mums in grocers see gaming towers front of store, pensioners play Candy Crush and endless variants of sudoku and Scrabble, pre-teens embrace Nintendo Switch, while 15-25s play the field on their phones.

Music may be universal but only a minority have an active commercial relationship with it, gaming has perfected the art of turning almost everyone into a paying gamer.

3) Deal with the limitations of exclusive rights

Copyright may be the key enabler of the music business, but the ability of any one of literally hundreds of rights owners to veto a new idea means for many entrepreneurs, music’s exclusive rights can be a dis-abler.

The need for universal buy-in means too often services report difficulties in licensing new services or even features.

Put yourself in the shoes of an entrepreneur who has the choice of creating a game where he needs no one’s permission to launch, versus music where the negotiation can be truly Kafka-esque and it’s pretty clear which is the better bet.

That’s not an argument against copyright. It’s an argument for using it to facilitate new ideas, rather than to block them.

4) View the consumer as an equal

Gaming is inherently interactive, involving the consumer in co-created experiences. Recorded music is by definition a fixed linear performance, but that still leaves scope to better enhance the interactivity of the listener experience, what’s known as gamification.

It is no surprise that the huge growth we’ve seen in digital gaming in particular over the past years has coincided with the huge growth in social media. More than ever popular culture is about the fan as much as it is about the art itself.

There are doubtless multiple other factors, but the point most of all is to kickstart a more fundamental conversation about what the music market could be.

Too often music feels weighted down with its history whether it be remuneration models dating back to the days of the phonograph, wasteful duplication among collection societies or cavalier approaches to data more suited to the days of paper ledgers rather than the age of cloud computing.

5) Music needs to embrace its future.

True, there some positive signs with a growing number of entrepreneurs exploring options beyond the £9.99 all-you-can-eat default, services like kids audio platform Yoto or genre specialist Jazzed. And there’s VR, live streaming and podcasts too.

Music needs all of them and more. The example of the games business shows the benefits of developing a portfolio of channels to market.

If music can crack that, the potential could be greater than any of us can even imagine.Music Business Worldwide