You might remember that Universal Music Group‘s Q2 results didn’t exactly attract a sunny response from Wall Street analysts.

Despite overall revenues being up close to 10% YoY, UMG’s subscription streaming revenues in the quarter were up by a moderate 6.9% YoY – lower than many analysts forecast.

Those results set into motion a wave of what Wall Street calls a ‘correction’ — aka multiple analysts downgrading their price targets for UMG’s stock.

Later today (September 17), Universal Music Group is hosting a Capital Markets Day (CMD) event in London that the company doubtless hopes will renew optimism about its future valuations.

MBW will obviously report all the juicy details from this CMD. But with around three hours still to go before the event kicks off, UMG has already come out of the gate today with some big news.

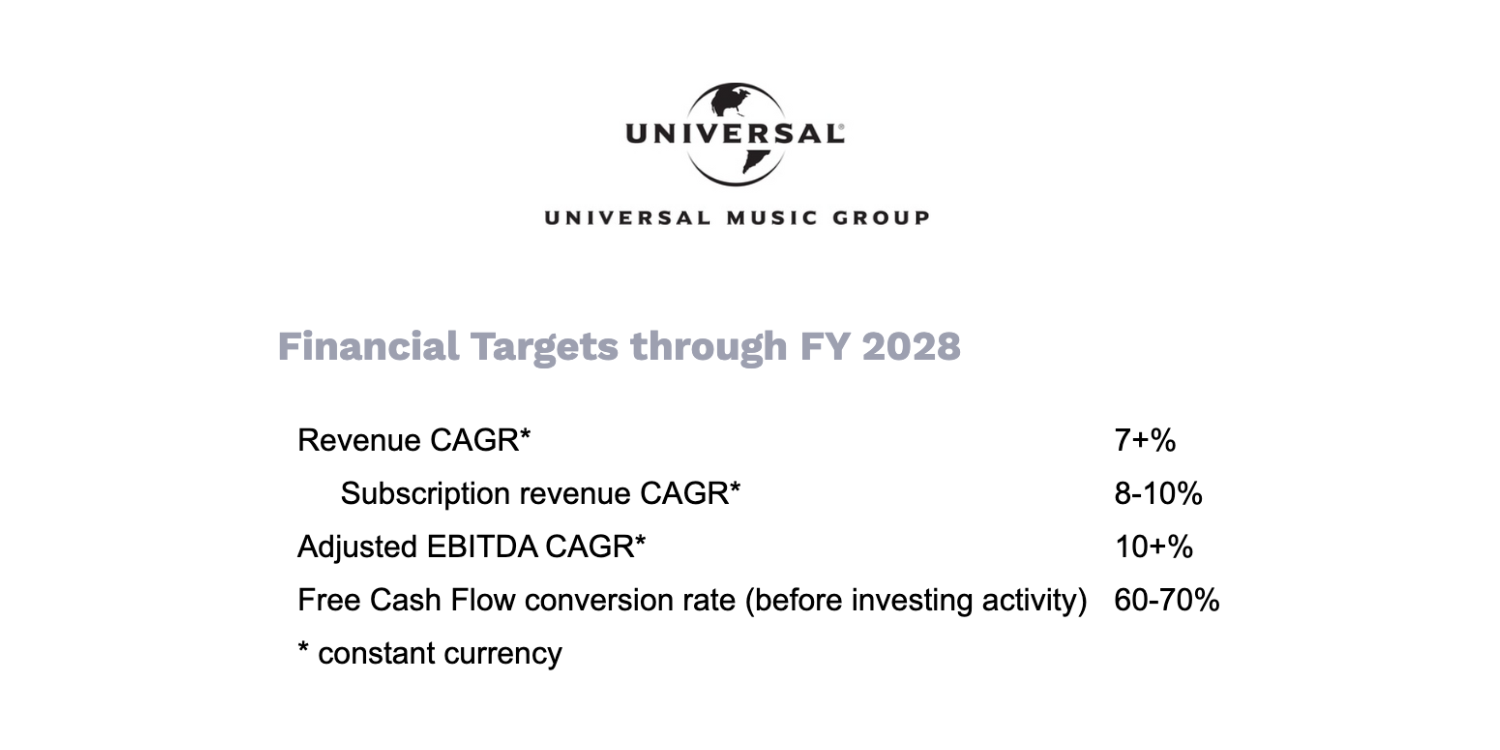

The company has this morning issued new financial targets for its next five fiscal years (including the current one), taking us through to the end of FY 2028. (UMG’s FY runs the same as each calendar year.)

Although UMG hasn’t published specific annual revenue projections for each of these years, it has given us ‘CAGR’ expectations.

That’s Compound Annual Growth Rate or, to the layman, the average percentage figure by which its numbers will increase annually across the half-decade period.

UMG’s new CAGR forecasts are reasonably buoyant, with Universal citing optimism over “the continued growth in subscription revenue, accelerating superfan monetization, and an expanding partner ecosystem that [we] expect will translate into meaningful Free Cash Flow generation.”

Here are the three headlines from UMG’s new targets:

- UMG expects its overall revenues to grow at a CAGR of 7%-plus (at constant currency) between FY2023 and FY2028;

- UMG expects its subscription streaming revenue to grow at a CAGR of somewhere between 8% to 10% (at constant currency) in the same period;

- UMG expects its adjusted EBITDA to grow by 10%-plus (at constant currency) during the same period.

The firm also expects its Free Cash Flow (FCF) conversion rate (before investment activity) to reach 60%-70%.

Now let’s understand what all that means in real terms.

MBW has modeled out how, if they come true, UMG’s target CAGR numbers will affect its financial performance in the years ahead.

Below, you can see what these forecasts will mean for UMG’s future financial health: first, in terms of its overall revenues and profitability, and second, specifically, in terms of its streaming subscription growth.

UMG’s new forecast: Overall revenues and profitability

To fully grasp the importance of UMG’s new numbers, it helps to know two things:

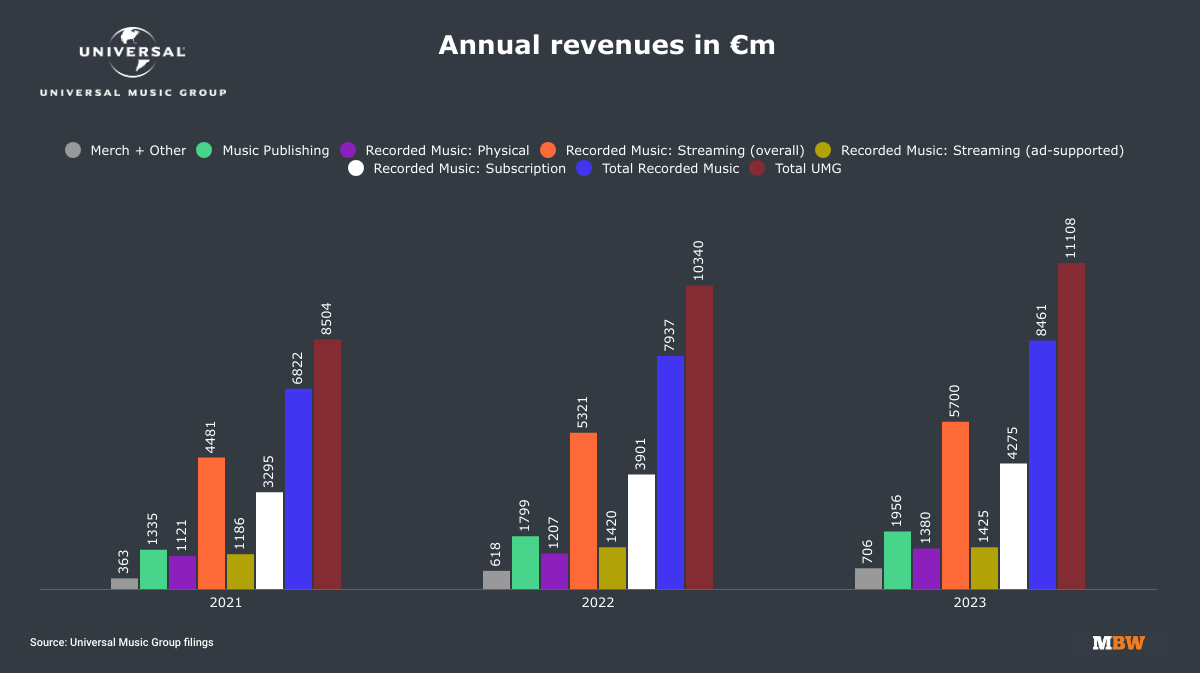

- The company’s overall revenues jumped to EUR €11.108 billion in FY 2023, up 11.1% YoY at constant currency;

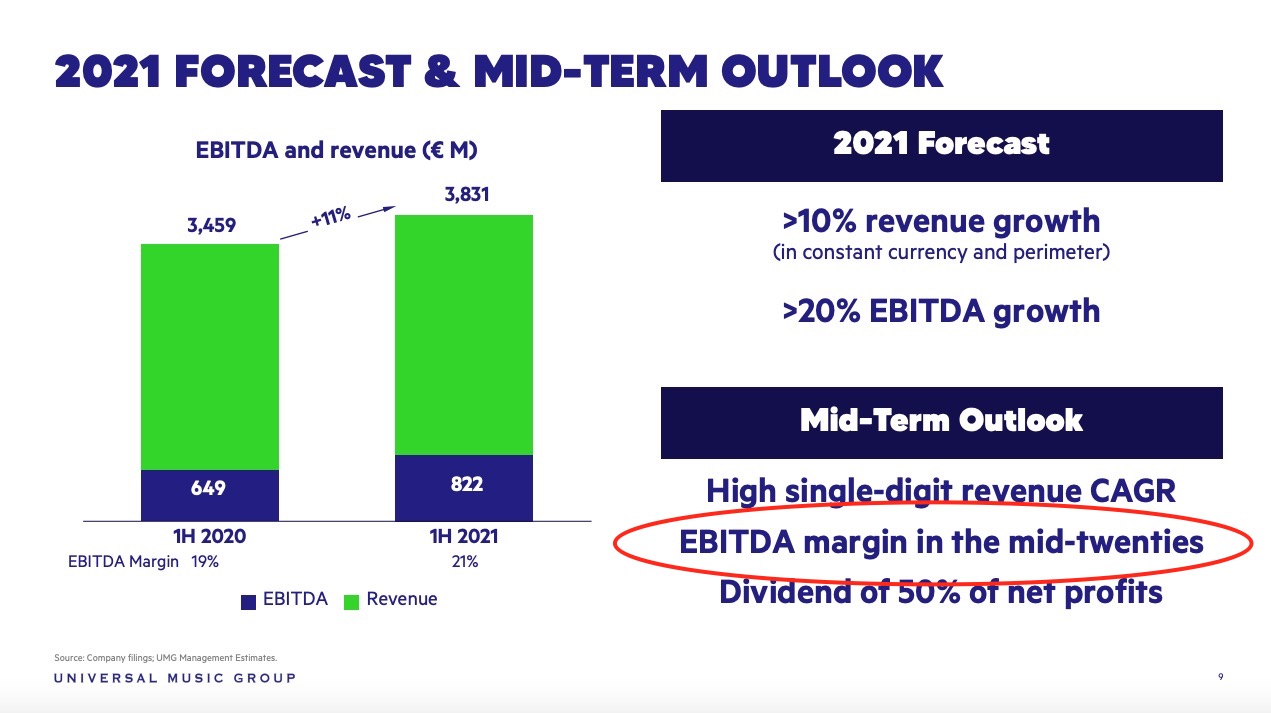

- At UMG’s last Capital Markets day in 2021, the firm pledged to hit a “mid-twenties” EBITDA margin (i.e. around 25%) in the “mid-term.” Earlier this year, UMG announced a global cost-cutting program, which it said was required to reach this EBITDA target.

So. Remember that UMG now says it expects its total revenue CAGR to hit 7%-plus (to be extra-clear: that’s at least 7%), and its adjusted EBITDA to hit 10%-plus?

You don’t have to be a math genius to realize that, if adjusted EBITDA is growing faster than revenues, then so too will UMG’s adjusted EBITDA margin be growing year-on-year.

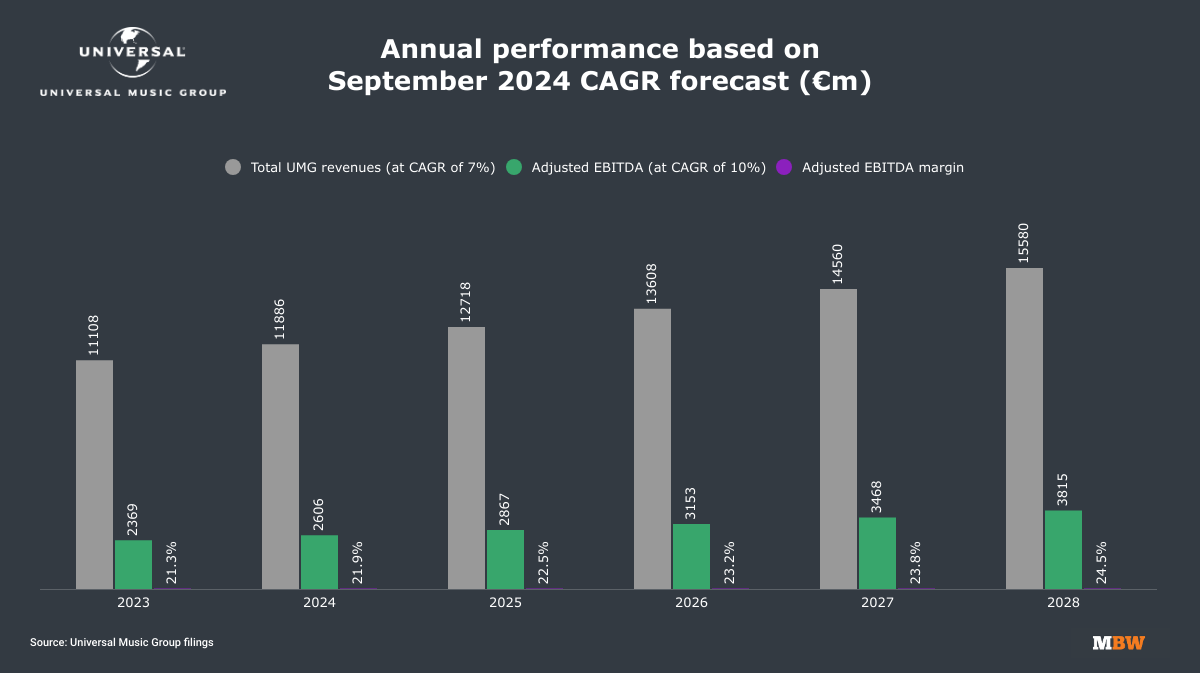

Below, you can see what would happen if UMG’s FY revenues (in EUR) grew at 7% annually between FY2023 and FY2028 and its adjusted EBITDA concurrently grew at a 10% CAGR.

As you’ll see: at these growth rates, UMG would add around EUR €4.47 billion (USD $5bn) to its annual topline revenues over the period, while adding EUR €1.45 billion (USD $1.6bn) to its annual adjusted EBITDA.

(Disclaimer: these numbers all discount future currency fluctuations. They’re what UMG’s performance would look like based on today’s CAGR numbers at constant currency. The EUR-USD conversions are illustrative and have been made at current rates.)

Perhaps more importantly to UMG investors who remember that 2021 Capital Markets Day, this scenario would see UMG land in and around that “mid-twenties” adjusted EBITDA margin target by FY2028, at 24.5%.

And remember, these projections are the low end of UMG’s new financial targets: the ‘plus’ in its 7%-plus CAGR target for revenues and 10%-plus CAGR target for adjusted EBITDA is important!

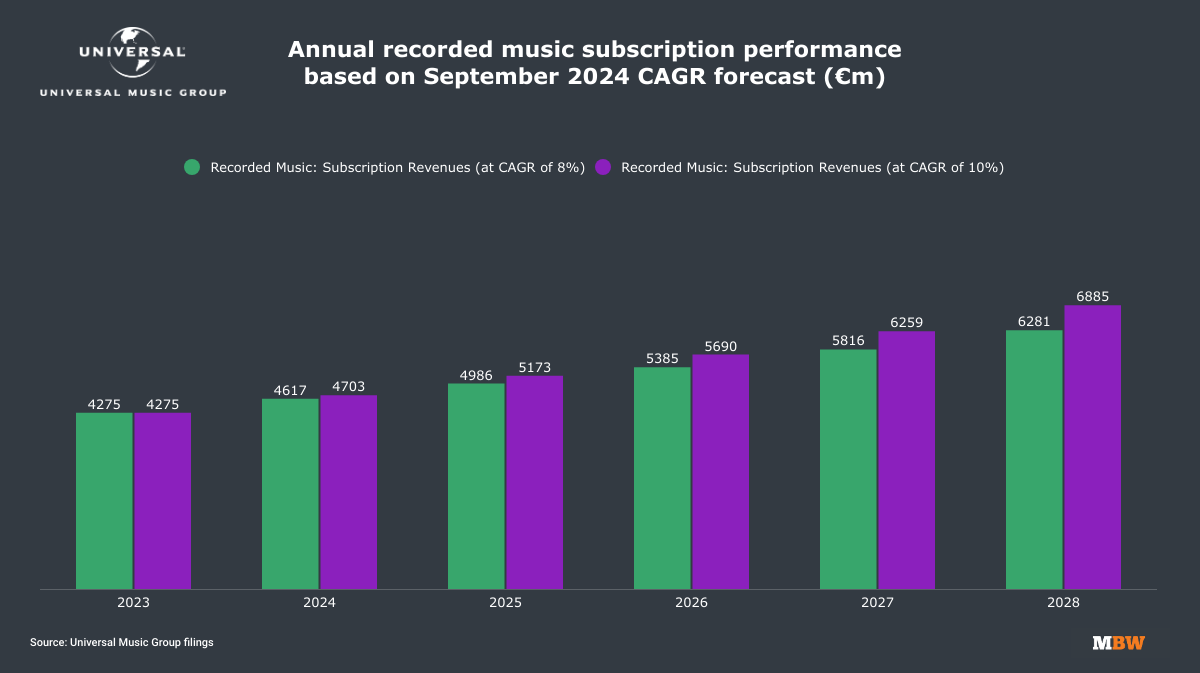

UMG’s new forecast: Annual subscription revenues

Remember: UMG now says it’s expecting subscription revenue to grow at a CAGR of between 8% and 10% over the five-year period in question.

This gives us a specific forecast to model out – a top end (10%) and a low end (8%).

At the top end (10% CAGR), UMG’s annual recorded music subscription revenues in FY 2028 would be EUR €2.61 billion (USD $2.9bn) bigger than they were in FY 2023.

At the low end (8% CAGR), UMG’s annual recorded music subscription revenues in FY 2028 would be EUR €2.01 billion (USD $2.2bn) bigger than they were in FY 2023.

If we look for a rough midpoint, therefore, it’s fair to say that UMG is projecting that its annual recorded music could grow by approximately USD $2.5 billion in FY 2028 vs. FY 2023.

(Again, the disclaimer: these numbers all discount future currency fluctuations. They’re what UMG’s performance would look like based on today’s CAGR numbers at constant currency. The EUR-USD conversions in this article are illustrative and have been made at current rates.)

We expect more detail/color on these numbers from Universal Music Group later today at the CMD.

The company says the event will include “presentations and a Q&A session with senior management”.Music Business Worldwide