There are financial statistics in the music business that, on the surface of things, don’t tell us too much. They might be big and impressive, but they give little away about trends affecting the wider business.

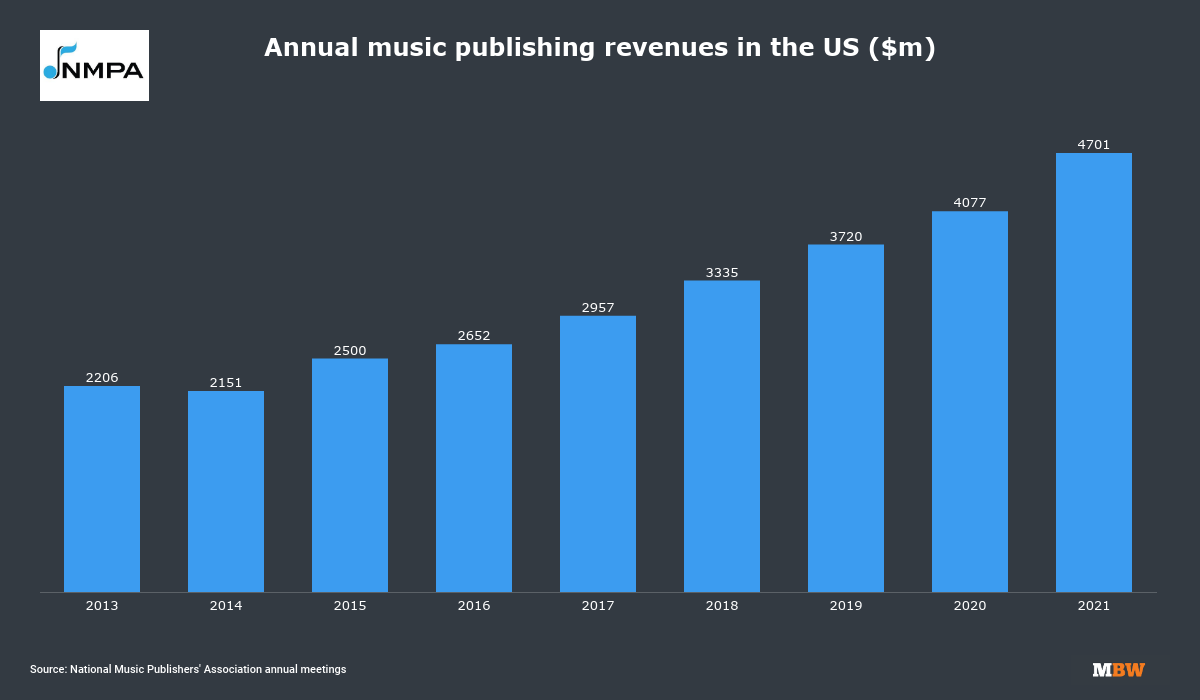

Here is one of those numbers: According to the National Music Publishers’ Association, the US music publishing industry generated USD $4.70 billion in the calendar year of 2021.

That figure, revealed by NMPA boss David Israelite at the trade org’s annual meeting in New York in June, was up by just under $700 million versus the equivalent number from 2020 ($4.08bn).

It was also more than double the size of the annual revenues of music publishers in the States as recently as 2014 ($2.15bn), according to previously announced NMPA data.

Music publishing’s growth in the US in 2021, however, was nothing compared to how the recorded music industry ballooned in the same year.

Where the NMPA figure gets really interesting – especially in the context of ongoing music industry debates – is when you compare it to the equivalent figure from the US record industry.

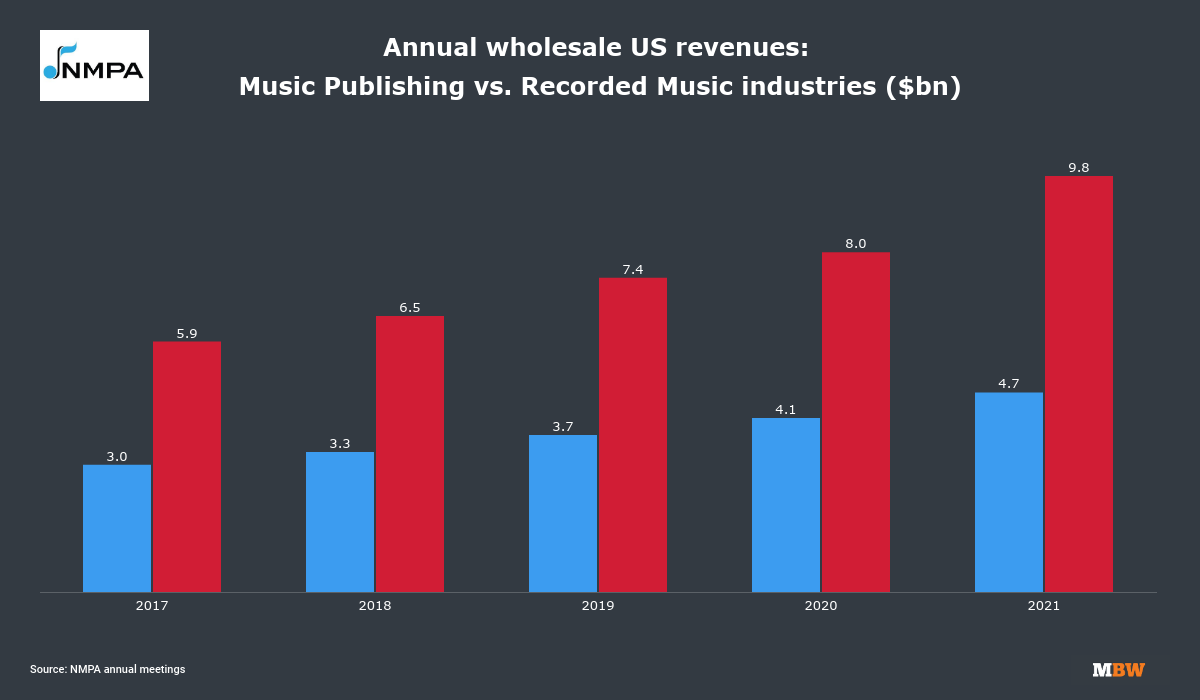

The aforementioned 2021 figure for annual US music publishing revenues ($4.70bn) was estimated using a survey of NMPA members.

As such, it is a reflection of total wholesale revenues received by music publishers in the period.

There is an equivalent wholesale annual number on the recorded music side of the music business in the US, provided by the RIAA (Recording Industry Association of America).

That figure stood at $9.8 billion in 2021, as confirmed by the RIAA back in March.

That $9.8 billion wholesale figure for 2021 was up by $1.8 billion year-on-year, compared to the $8.0 billion revenue received by record labels/distributors in the US in 2020.

To summarize the point: Music publishers saw their wholesale US revenues rise by $700 million in 2021, according to industry (NMPA) data; but record companies (and distributors) saw their wholesale US revenues rise by more than double this figure: $1.8 billion.

Regular MBW readers will know that the difference between these two numbers is sure to fire up certain figures within today’s music biz, who argue the recorded music industry is generating an inequitable amount of money versus the music publishing (and songwriting) space.

One such figure is Hipgnosis founder Merck Mercuriadis, who last year wrote an op/ed for MBW in which he argued: “[2021] will be the most lucrative year ever seen for the recorded music industry by approximately 90% of the people working within it – and the cash is flooding in.

“Yet songwriters, who are ultimately responsible for this success, are not getting their fair and equitable share.”

That being said, there are signs that 2022 could be a uniquely bumper year for the growth of the music publishing (and songwriting) business.

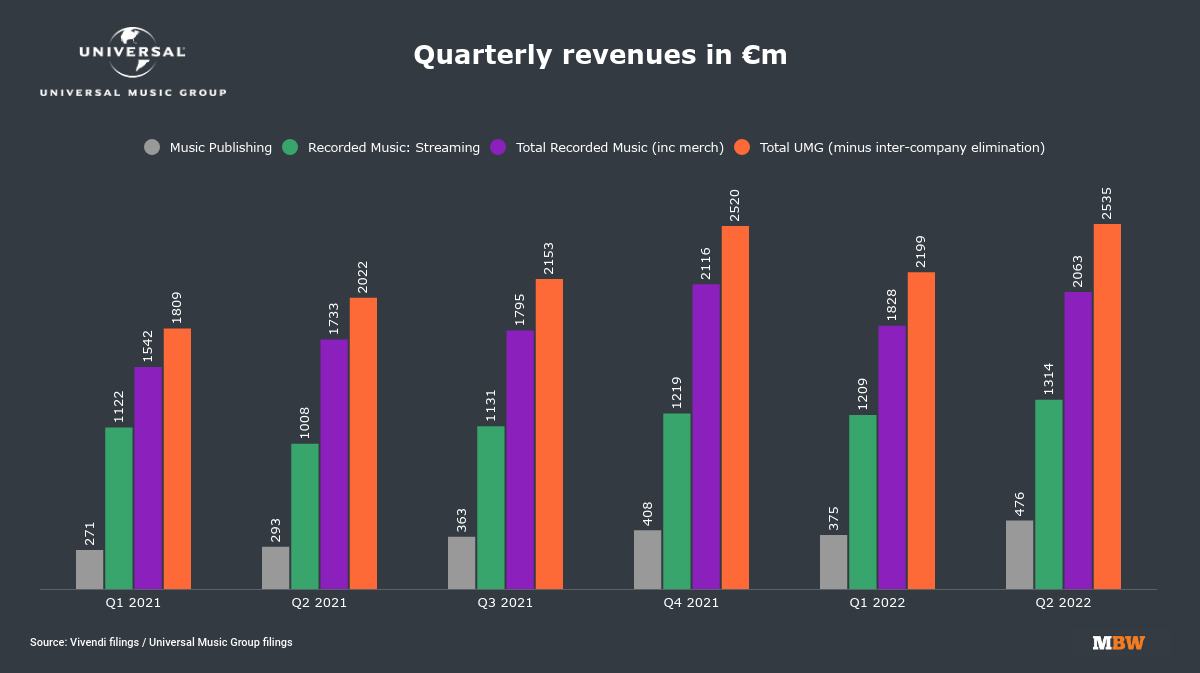

One key indicator behind that suggestion: the impressive global performance of major music publishers in H1 2022.

For example, Sony‘s global music publishing revenues were up by 14.0% YoY in calendar Q1 2022 (at US dollar-based constant currency), and were up by 13.2% YoY in calendar Q2 2022.

Universal Music Group‘s music publishing revenues, meanwhile, were up by a whopping 42.1% YoY at constant currency in the first half of 2022, although this dramatic increase was partly driven by UMG now recognizing collection society revenue differently than it did in 2021.

Another significant contributing factor to music publishers’ growth in 2022: A hard-fought windfall from the likes of Spotify and Amazon Music.

In July, the US Copyright Royalty Board announced a final ruling regarding the legal showdown known as ‘Phonorecords III’.

That ruling centered on an increase in the overall percentage of on-demand music streaming services’ US revenues that legally have to be paid by the likes of Spotify to songwriters.

The CRB ruled that this percentage figure should have moved up from 10.5% to 15.1% across the five years between 2018 and 2022.

As a result, streaming services are now having to fork over retrospectively-owed money to music publishers.

How much money are we talking about?

There was a clue in Warner Music Group‘s latest financial results (for the quarter ending June 2022).

In those results, WMG announced that Warner Chappell Music (WCM) – its own publishing company – had received a one-time $17 million benefit in the quarter “resulting from the July 1 remand ruling by the CRB in the Phonorecords III proceedings”.

Music & Copyright estimates that WCM’s global market share of the music publishing industry was 11.8% in 2021.

WCM’s market share could obviously be higher than that figure if we’re specifically talking about the US alone. But it strongly indicates that WCM’s $17 million bonus from the ‘Phonorecords III’ outcome should be multiplied many times over if we’re looking to estimate how much one-time money the entire US music publishing industry will be receiving from Phonorecords III.

On that topic, the music publishing industry is now gearing up for another major legal fight with the on-demand streaming services in ‘Phonorecords IV’ – the new, yet-to-begin CRB proceedings that will determine what songwriters in the US get paid from streaming services in the years between 2023 and 2027.

Speaking to NMPA members at the org’s annual meeting in June, David Israelite said: “We now know [via NMPA estimates] that [on-demand streaming] services paid record labels $5.7 billion in 2021, 58.6% of the revenue pool – significantly higher than the 52% that is often reported.

“To be clear, songwriters being paid properly does not mean artists and record labels need to be paid less.

“It is unconscionable that digital delivery services take three times the amount they pay the songwriters to make their businesses possible.”Music Business Worldwide