BMI will pay songwriters and publishers a smaller portion of its revenues as a for-profit company – while upping its own margin from 10% to 15% of collections. Will its members tolerate this change?

Credit: AlamyPeso Pluma was one of nearly 100,000 new BMI members to join the org in the 12 months to end of June

MBW Explains is a series in which we dig behind the headlines, via data and context, to improve your understanding of key stories. Only MBW+ subscribers have unlimited access to these articles. MBW Explains is supported by Reservoir.

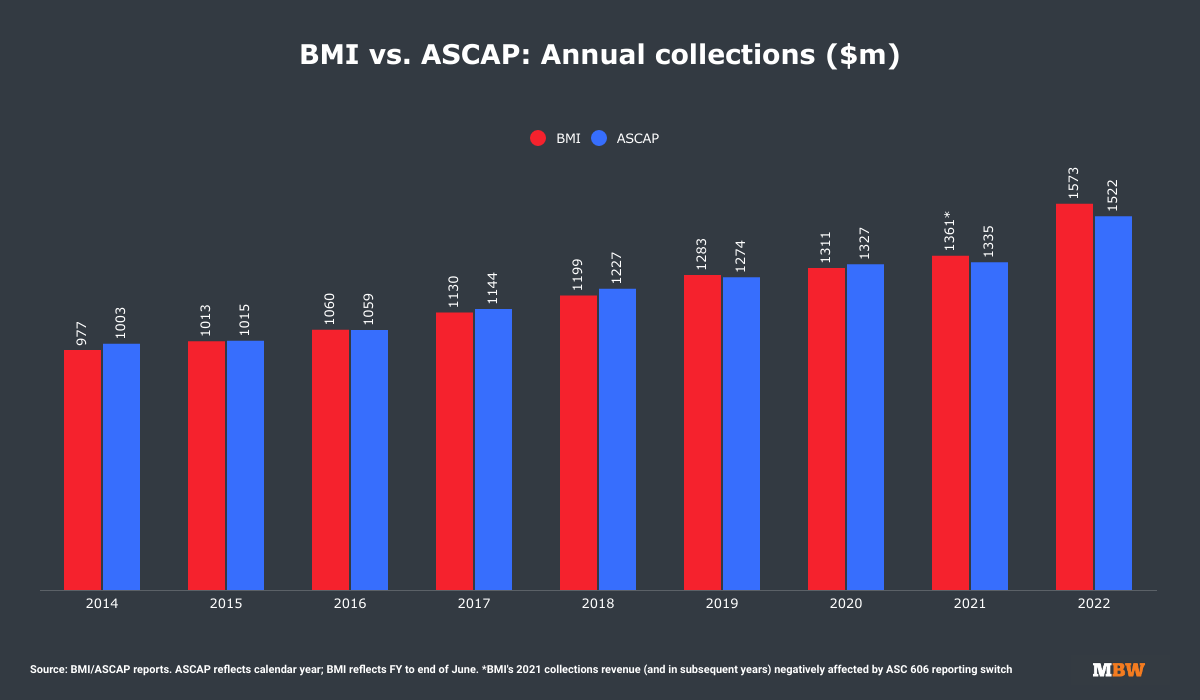

In recent years, at around this juncture in the calendar, Music Business Worldwide has published data charts showing the size of BMI’s yearly revenue collections and distributions; subsequently, we’ve looked at how these figures match up to ASCAP‘s equivalent numbers.

For example: In 2022 (to the end of June last year), BMI’s annual collections hit USD $1.573 billion; ASCAP’s 2022 collections (to the end of December last year) weighed in at around $50m less – $1.522 billion.

Sadly, for 2023, such a comparison has been rendered impossible – because BMI’s 26-page latest annual report doesn’t include any headline revenue data. BMI has chosen to omit these figures following its announcement, a year ago this month, to switch to a for-profit business model.

There are, however, other very important numbers included in BMI’s new annual report – with one in particular bound to get the songwriter and publishing communities talking.

Ever since BMI announced its switch to a for-profit model, questions have been circling amongst its members (‘affiliates’) as to how this will affect their payouts from BMI, the world’s largest PRO in revenue terms.

Now, Michael O’Neill, CEO of BMI, has answered at least some of these questions.

In the new report, O’Neill reveals that BMI is planning to increase the margin of annual collected revenue it retains (i.e. spends on operating costs or banks as profit).

Says O’Neill: “As we look at the next three years of our business, our goal is to distribute 85% of licensing revenue to our songwriters, composers and publishers and retain approximately 15% to cover our expenses/overhead (which have historically run around 10%) and a modest profit margin.”

“As we look at the next three years of our business, our goal is to distribute 85% of licensing revenue to our songwriters, composers and publishers and retain approximately 15% to cover our expenses/overhead (which have historically run around 10%) and a modest profit margin.”

Michael O’Neill, BMI

O’Neill defends the move to increase BMI’s retained margin from 10% to 15% by noting that the latter figure “is well below the margins taken by comparable for-profit businesses in our industry”.

O’Neill also addresses a previously expressed concern of the songwriting community: the idea that BMI could borrow capital and then, in future, ‘pinch’ from BMI revenue that would otherwise be distributed to songwriters in order to pay it down.

That’s not going to happen, says O’Neill.

He clarifies: “[If] BMI decides to seek outside capital or borrow money to invest in new services and opportunities, any repayments will come out of our retained profits and not distributions.”

What’s the context?

Simmering away in the background of O’Neill’s new clarification, of course, is the fact that BMI might (or might not) be acquired by a private equity company any time soon.

In August, MBW broke the news that BMI was in conversations regarding a potential sale to New York-headquartered private equity company, Blue Mountain Capital (BMC).

(Sidenote: BMC is the majority-owner of Citrin Cooperman… who’ve not had the easiest past few days in the music industry).

The price-tag subsequently bandied around that BMC-BMI acquisition deal: USD$1.7 billion.

“Importantly, the strategy outlined [to move to a 15% retained annual margin] will hold true for BMI whether or not we move forward with a sale.”

Michael O’Neill

Michael O’Neill addresses the BMC-BMI rumors directly in his comments in BMI’s latest report, noting: “[W]e are all aware of the conversations taking place about a possible sale ofBMI.

“I can confirm that we are engaging in discussions with a potential new partner, and while our conversations are ongoing and have been very productive, no deal has been signed at this time.”

O’Neill further clarifies that BMI’s plan to retain a 15% margin in future “will hold true for BMI whether or not we move forward with a sale”.

WHAT HAPPENS NOW?

The biggest danger for Michael O’Neill and BMI in switching to a 15% margin is simple: Songwriters and publisher clients notice a negative impact on their earnings from this move – and quit the PRO.

Since announcing its for-profit move a year ago, BMI has sold the idea to its songwriter members as a cause for excitement. O’Neill and his management team argue that retaining more profit in BMI’s business also means having more cash to reinvest into better services and acquisitions… which will ultimately grow songwriter revenues.

An early example of this strategy could be seen in May this year when BMIpartnered with Music Nation, a music rights org based in the United Arab Emirates (UAE), in a bid to extract better data – and bigger royalties – from the region for BMI members.

Can BMI strike more deals like this in future to materially increase annual revenues by such a degree that songwriters and publishers don’t begrudge the org swallowing an extra 5% of margin?

It’s off to a good start.

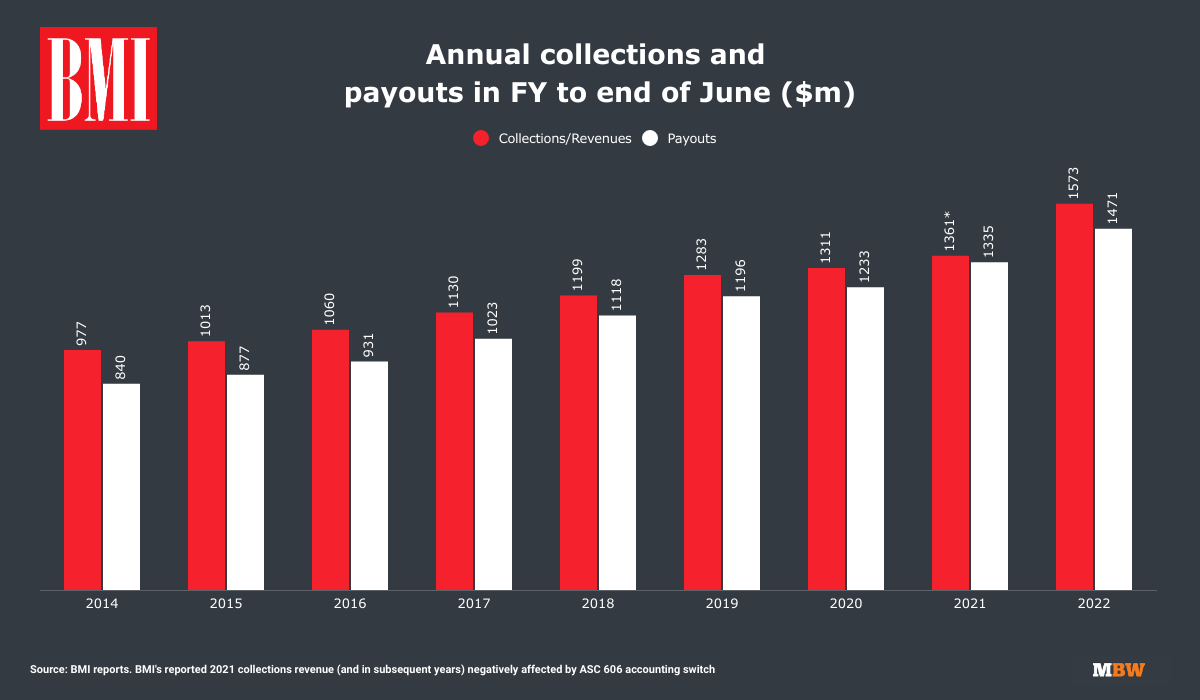

As mentioned, BMI doesn’t give us an exact figure for its annual FY 2023 revenue collections (to end of June this year) in its new report.

However, MichaelO’Neill does give away two related data points in the report that paint a picture of the org’s current size:

O’Neill says that BMI’s payouts to members for the full calendar year of 2023 (under the new for-profit model) are “projected to be up11%” versus the same period a year before. We don’t know exactly what BMI’s payouts (aka ‘distributions’) were in calendar 2022, but we do know that in the 12 months to end of June 2022 (i.e. its FY), this payout figure stood at $1.47 billion. An 11% rise on that would have meant BMI’s annual distributions surpassing $1.63 billion in FY 2023;

In addition, O’Neill notes that BMI’s upcoming quarterly distribution of royalties, in November, is “forecast to be over $400 million” – the first time, he says, that any PRO worldwide has ever surpassed this milestone in a single quarter. Obviously enough, on a run-rate basis, this $400 million quarterly number suggests that a $1.6 billion-plus annual payout to members is on the cards for BMI at some point soon.

There is, though, one other big question sparked by Michael O’Neill’s new announcements: Will BMI stop at a 15% margin? Or will it – especially under the prospective ownership of private equity – look to crank this number further upwards in the years ahead?

It’s worth noting that O’Neill’s new announcement on the switch from a 10% margin to a 15% margin isn’t definitive: He says, if you read his words carefully, that a 15% margin is BMI’s “goal”.

Should the company fall short of revenue/profit targets in years ahead, might the “goalposts” move a little on that number?

“Any incremental growth [BMI’s management] create[s] for the company (for example through better technology, M&A opportunities, new businesses or expanded services), we will look to take a higher margin [than 15%] on any revenue generated, though always with the goal of sharing that new growth with our affiliates.”

Michael O’Neill, BMI

Indeed, O’Neill has also already confirmed that, yes, in specific circumstances, BMI will move the 15% margin figure higher.

In his opening address in the new report, O’Neill qualifies that “any incremental growth [BMI itself] creates for the company (for example through better technology, M&A opportunities, new businesses or expanded services), we will look to take a higher margin [than 15%] on any revenue generated, though always with the goal of sharing that new growth with our affiliates”.

Sounds like that 15% margin covers BMI’s existing services. If and when it expands into new areas of business, it may retain a higher margin of revenue from these additional services.

A final thought…

There are a few intriguing angles to think through on Michael O’Neill’s new comments and BMI’s future more generally.

One of those angles: If, as it says it’s planning to, BMI uses its fatter profit margin to acquire future companies, what kind of businesses will it look to buy?

Could we see BMI following the path set by its for-profit rival SESAC, which has in recent years not only expanded geographically (see: SESAC’s JV with SUISA in Europe, Mint) but also via acquisition into ‘music services’ outside of its core business of performance royalty collection?

Today, SESAC Music Group’s ‘music services’ division includes the recorded music distributor and services provider, Audio Salad (acquired in March 2023), as well as the US mechanical rights licensing house, HFA (acquired in September 2015), plus digital royalty collection platform Audiam (acquired in August 2021).

In addition, SESAC has moved into some degree of music rights ownership: under SESAC Music Group these days sits Audio Network, the UK-headquartered production/audiovisual music rights house which, according to UK Companies House filings, generated GBP £34.6 million in calendar 2022 – with a pre-tax profit of GBP £11.7 million.

Without outside capital, it may prove tough for BMI to keep up with the M&A spending of SESAC, of course… considering that SESAC can call on capital from its parent – Blackstone’sprivate equity business.

Another interesting narrative to watch: In a previous column on BMI, I suggested that, chasing a meatier profit margin, the org might consider limiting the number of songwriters who can join its membership in years ahead – or even jettison a chunk of its existing member base.

The logic behind this? It runs parallel to the recorded music industry: There are 9 million artists today on Spotify, but, according to Spotify itself, 95% of the royalties on its platform are generated by just 200,000 of these acts. i.e. 2.2% of the artists on Spotify generate 95% of the revenue.

These are the economics of streaming, which have been dramatically changed by DIY distribution and an explosion of amateur artists making records at home.

Fact is, for an org like BMI, the vast majority of these amateur artists (who are usually also songwriters) generate negligible streaming and other performance revenue – adding to the risk that their rights may actually cost more to administer than the annual membership fee they pay a given PRO.

Michael O’Neill is adamant, however, in BMI’s latest report that the PRO, as a for-profit entity, will “maintain our open door policyof welcoming all songwriters and composers of all genres of music, as we have done since our founding.”

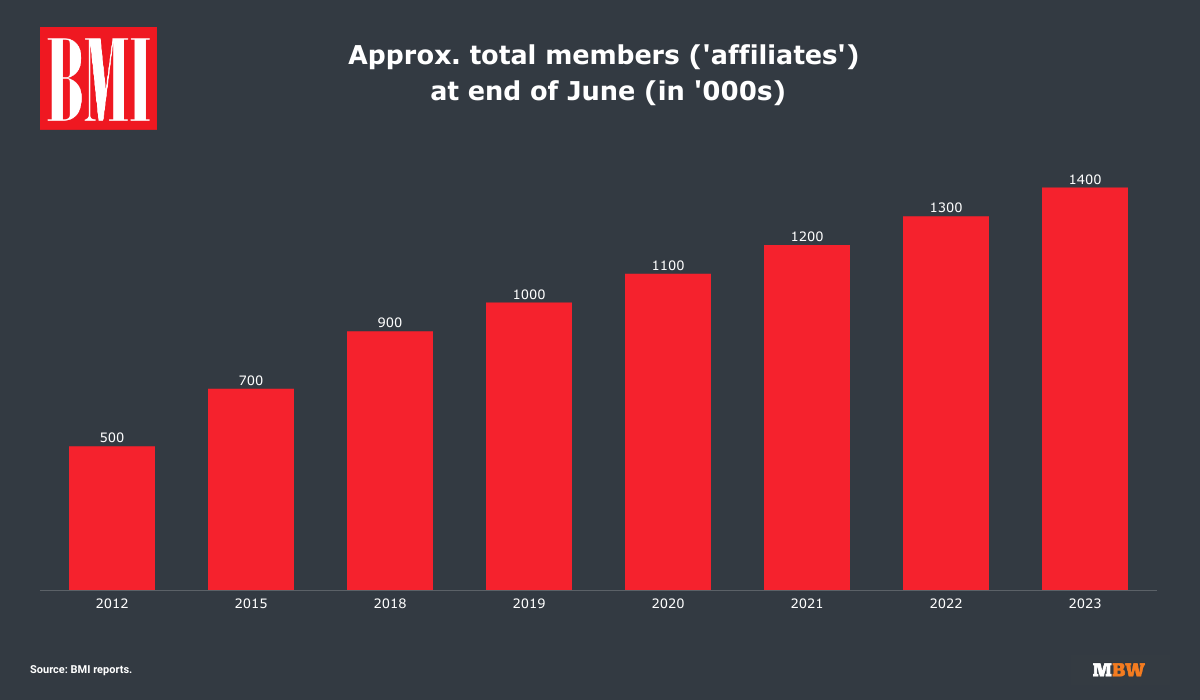

That intention plays out in the numbers: According to BMI’s latest report, it counted 1.4 million ‘affiliates’ at the end of June 2023, up by “nearly 100,000” on the same period of the prior year.

That ~100k+ annual growth in membership has remained remarkably consistent at BMI in recent years, according to the data (see below).

Last thought on all of this (for today): What happens when BMI sells?

Within this new report, Michael O’Neill has answered a few of the key questions from songwriter groups that have been publicly posed to BMI since it announced its for-profit plans.

But what O’Neill hasn’t answered – or even hinted at – are those questions that linger over the post-sale process at the PRO. A colossal example: Where will the mooted $1.7 billion sales price actually go if BMI sells?

As covered in my previous column on this topic, BMI today is owned by US broadcaster networks – predominantly in the world of radio.

How will the songwriter community feel about this sector netting a ten-figure windfall, essentially thanks to the financial growth of the music publishing industry?

Especially when the US radio industry isn’t exactly considered the most generous payer amongst songwriting talent or music publishers – and continues to refuse to pay a performance royalty for recorded music in the US?

To smooth over these potential bumps, might BMI consider paying something – perhaps a set amount, perhaps a proportion of that ~$1.7 billion sale price – to its members? Would its radio industry owners acquiesce to such an outcome?

If so, whatever BMI pays would have to be meaningful. After all, if it went down this route, it would be breaking with recent music industry tradition.

When Universal Music Group and Warner Music Group floated on stock exchanges in 2021, neither their songwriter or artist rosters received a direct monetary windfall (at least, those who weren’t shareholders didn’t).

For songwriters (but not performing artists), it was the same scenario when Sony Music Group and Warner Music Group sold stakes in Spotify in 2018, netting vast proceeds.

Sony Music was rightly applauded by the artistic community for sharing over $250 million of its $768 million in Spotify equity proceeds with performers – and disregarding their unrecouped balances – in 2018. (Warner also shared a portion of its proceeds with artists, but didn’t disregard unrecouped balances.)

However, because these equity stakes were rooted in recorded music licensing agreementsdating back to Spotify’s beginnings, songwriters (as in, songwriters who aren’t also artists) missed out on this cash.

In August, a group of songwriter advocates wrote to Michael O’Neill with a list of questions that included the following pointed queries on the topic of BMI potentially sharing out some or all of the proceeds from its sale:

If BMI sells, will writers or composers receive part of the sale proceeds?

If BMI sells, will the broadcasters on BMI’s Board receive the sale proceeds?

If so, why should broadcasters be the biggest beneficiary from a sale of a company whose only asset is songs that belong to songwriters?

If BMI’s most successful songwriter members are left feeling aggrieved or excluded by the PRO’s sale process – or, indeed, by BMI’s decision to increase its margin of collected revenues from 10% or 15% – the likes of ASCAP, SESAC, and Global Music Rights will be only too pleased to make their acquaintance.

Michael O’Neill’s opening letter from BMI’s latest annual report (FY 2023) in full

October 12, 2023

Dear BMI Affiliates and Industry Partners:

We are pleased to issue our FY ‘23 annual report, which highlights the excellent year for BMI and our affiliates. In addition to the annual report, which I encourage you to review, I would like to address a few other topics.

First, we are all aware of the conversations taking place about a possible sale of BMI. I can confirm that we are engaging in discussions with a potential new partner, and while our conversations are ongoing and have been very productive, no deal has been signed at this time.

There have also been a lot of questions recently about BMI and our business model transition, and I appreciate that our affiliates have a right to understand how they may be impacted by these decisions.

As I have shared, we changed our business model last year to invest in our company and position BMI for continued success in our rapidly evolving industry. Our mission remains the same, to serve our songwriters, composers and publishers and continue to grow our overall distributions as BMI has done each year that I have been CEO. In order to continue this trajectory, we need to think more commercially, explore new sources of revenue and invest in our platforms to improve the quality of service we provide to you. I’m pleased to say that we have already made great progress on delivering these goals.

Understandably, much of the recent discussion has centered around the level of profit that BMI will take under this new model, and I have heard your feedback around the need to clarify this issue. So let me do just that. Importantly, the strategy outlined below will hold true for BMI whether or not we move forward with a sale.

As we look at the next three years of our business, our goal is to distribute 85% of licensing revenue to our songwriters, composers and publishers and retain approximately 15% to cover our expenses/overhead (which have historically run around 10%) and a modest profit margin. For context, this is well below the margins taken by comparable for-profit businesses in our industry. Additionally, for any incremental growth we create for the company (for example through better technology, M&A opportunities, new businesses or expanded services), we will look to take a higher margin on any revenue generated, though always with the goal of sharing that new growth with our affiliates.

In addition, if BMI decides to seek outside capital or borrow money to invest in new services and opportunities, any repayments will come out of our retained profits and not distributions. We will also announce the annual growth rate of our cash distributions.

I am pleased to share that our distributions for the full calendar year of 2023, all under our new model, are projected to be up 11% compared to the corresponding distributions under our old model in calendar year 2022. Not only did each quarter increase year-over-year, but our upcoming November distribution is forecasted to be over $400 million, another record that would make BMI the first PRO to ever distribute this high an amount in a single quarter.

We will also maintain our open door policy of welcoming all songwriters and composers of all genres of music, as we have done since our founding.

We are excited for the future and confident in our ability to accomplish our plans on our own, but we also recognize the opportunity to substantially accelerate our growth by partnering with a like-minded, growth-oriented investor with a successful history of building businesses. Of course, that partner would need to share our vision that driving value for our affiliates goes hand-in-hand with growing our business and building a stronger BMI.

As always, we are there for you, our incomparable creative community. We recognize there is no BMI without our songwriters, composers and publishers and it is in our best interests to ensure that any changes we make work to your advantage, so that you choose to remain part of the BMI family for many years to come. You have my commitment that the updates I’ve shared here, and any decisions we make going forward, will continue to benefit our creative community, so you can keep delivering the world’s best music.

Thank You,

Mike O’Neill

Reservoir (Nasdaq: RSVR) is a publicly traded, global independent music company with operations across music publishing, recorded music, and artist management.Music Business Worldwide