Selling future royalties via NFTs can generate meaningful revenue today. But buyers–and the artists selling them–should beware of risks. The following analysis comes from Bill Werde (pictured inset), Director of the Bandier music business program at Syracuse University and a former Editorial Director of Billboard. An earlier version of this essay originally appeared in Full Rate No Cap, his free, weekly email of music industry analysis.

Fans may have been excited when Rihanna opened the Super Bowl halftime show with her 2015 hit Bitch Better Have My Money. But perhaps no one was more ecstatic than the Swedish executives behind anotherblock, an NFT platform that sells stakes in future royalties of specific songs.

They had just days earlier completed the sale of tiny percentages of future royalties of that exact Rihanna blockbuster to investors.

Those same executives, and the producer whose master royalties they sold, were and are now watching —and profiting from — resales of the same. With the sale, anotherblock became the latest company to showcase both the opportunities and the huge questions and concerns that surround these sorts of royalty-based NFT securities.

For starters, and as best I can tell, the sale had nothing to do with Rihanna herself.

I managed to contact at least one member of her management team, in Arizona for the big show, and understandably not focused on this issue. But they were unaware of the anotherblock sale, and Rihanna has no posts on her Instagram or Twitter that share the sale. What anotherblock actually did was partner with Deputy, a credited producer and writer on Bitch Better Have My Money.

Anotherblock says they sold stakes in the master, so we will assume that Deputy has a possibly-generous 3% stake in the master (typically a star producer will get 4-6%, though it may be lower, particularly when there are multiple producers on a song; BBHMM credits at least four producers).

Anotherblock facilitated 300 sales of a .0033% stake of Deputy’s stake for $210 per purchase. So if my math is anywhere close to correct, what investors got for $210 was actually .0099% of the master rights of Rihanna‘s old hit.

UPDATE: The company behind the BBHMM NFT, anotherblock, has responded to this column and its estimates below. A company spokesperson notes that “Deputy [sold] 1% of the future streaming master royalties of the full track, not 1% of his share” in the NFT drop, and clarifies that no third party (manager, lawyer etc) will receive a cut of the “[NFT] buyer’s royalty share”. Furthermore, anotherblock clarifies that it does not make any money via a cut of the buyer’s future royalty earnings, but instead via a cut of the seller’s (Deputy’s) transaction receipts. The company adds: “Our website clearly states that this drop is brought to you by Deputy – in the headline, not the small print.”

So let’s start with the good: if you do the math, Deputy wound up auctioning off 1% of his stake and raised $63,000 with the first round of sales.

I note “the first round” because when you dig into the contract, you see that Deputy and anotherblock will take 5% of resale in perpetuity. Those same NFTs that sold for $210 are now generally reselling for $1200 to $1800, so anotherblock and Deputy are splitting $60 to $90 every time a BBHMM stake is resold. You can see how this sale showcases the artist empowerment aspects of Blockchain that have been much written about (some would say overhyped). It is unclear what cut of this money anotherblock takes.

Some aspects of the sale are less rosy, however.

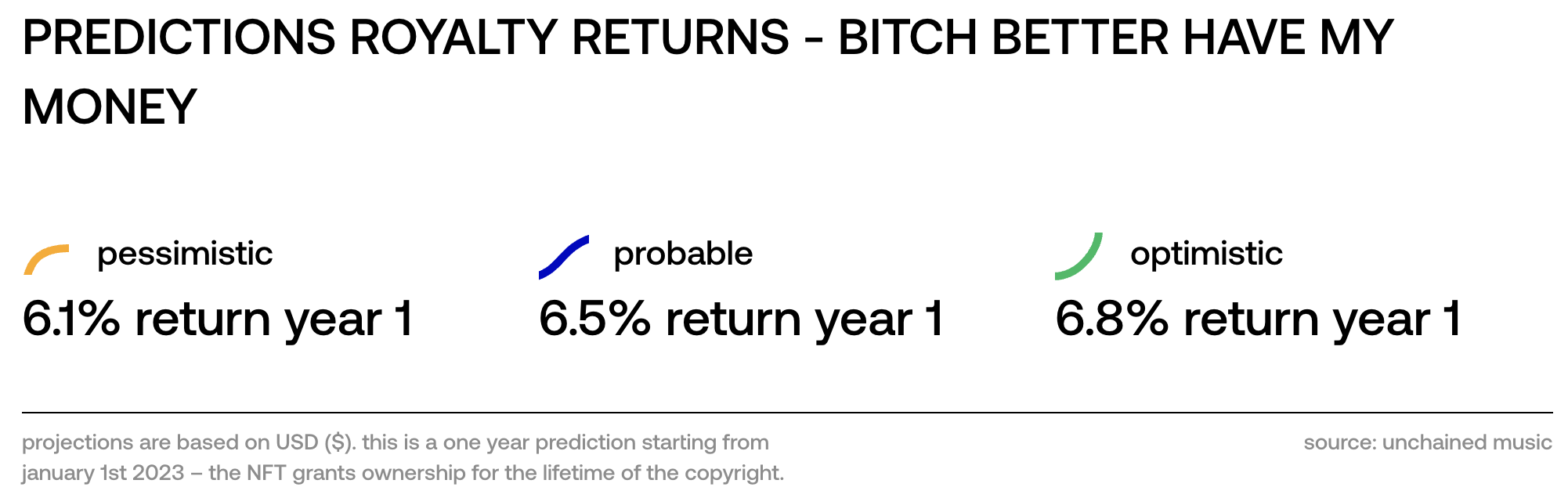

For starters, the site advertises “probable“ return on investment of 6.5% in year one but no amount of back-of-envelope math can get me anywhere close to the ballpark of that return for an investor who paid $210 for .0099% of the master right on this one Rihanna song.

Forget the ballpark—I’m not sure I can even get into the right state or country.

Let’s take out our pencils.

The song is currently averaging 886,000 streams per week for the past five weeks, according to Luminate. If we use a fairly standard estimate of $4,000 to the rights holder for every million streams, that nets out to be about $3,500 per week. From this amount, the master side is taking about 80%, or $2,800. If Deputy gets 3% of that, it takes us to $84. And the .0033% stake of Deputy’s stake? Just under 28 cents per week.

There’s obviously a ton of assumptions and rounding errors in this math, and many things that we don’t know. Does Deputy have a manager? If so, take 5 to 15% off of earnings. An attorney? A business manager? If so, keep trimming. Are we talking about global revenue, and not just US? If so, that 28 cents weekly probably becomes approximately 39 cents, using the roughly 60/40, US/rest-of-world revenue picture for the last full year of data we have from 2021.

Where and how does anotherblock take a cut? I couldn’t find that on their site. Does this .0033% stake include all revenue, including sync licenses?

The answers to all of these questions could shift earnings up or down. But if we use that 39 cent weekly figure, that gets you to about $20 annually. After taxes you’re probably taking home around $14 – $15 a year. At that rate, it would take approximately 14 or 15 years to recoup your initial $210 investment. So either I’m fundamentally misunderstanding a key part of this math, or anotherblock defines a 6.5% rate of return very differently than I do.

We could explore some other issues, such as whether or not the advertising and social media postings to market this sale, which included an image of Rihanna, violate her rights of publicity.

While the site is clear in the smaller print that what is being sold is a share of the producer’s royalties, it’s still Rihanna’s name at the top of the anotherblock site and “Rihanna” in all of the headlines about this, which has clearly created some market confusion.

But more than anything, I think this BBHMM sale probably illustrates why the SEC needs to provide more guidance about, and be more involved in these sorts of Blockchain-based sales against future artist royalties.

So far, the SEC has generally ignored these sorts of sales, but most experts I have spoken with tell me there are conversations happening behind the scenes, and an expectation that clarity will come. Certainly, the SEC has claimed jurisdiction over foreign-based companies selling securities to US investors in the past.

There has been a lot of discussion in legal and financial circles about whether or not these sorts of sales pass the Howey test—a list of questions used to determine if a transaction is considered a security, and should therefore be regulated.

I’m no expert on that question, but having had several conversations with people who are, it’s hard for me to see how sales like this aren’t a security. Artists and producers selling future royalties in this way, and of course, the platforms that are supporting them, should be aware that the SEC doesn’t play once it decides to crack down. Your personal liability may be at stake. If you’re considering a sale like this, a conversation with an attorney would be advised.

It’s worth noting here that non-Blockchain sales of future royalties exist, and are SEC-regulated. SongVes

In the music business as in the world, I try to discourage binary thinking. Most everything that’s interesting and worthwhile involves a spectrum and not a toggle, so please, don’t consider this essay a condemnation of legitimate artists and/or their reps selling NFTs, and perhaps not even NFTs that offer a stake in future royalties, if the math is transparent and the pricing is sensible. There’s a lot of potential for artists to do well for themselves while experiencing more control in the realm of blockchain-enabled business models.

But these are still early days. Without regulation, the risk of fans being exploited – lured by the (sometimes false) promise of ownership stakes in their idols – is very, very high. Not to mention the more pedestrian reality that anotherblock is advertising returns that seem unlikely, given what we know (while absolutely acknowledging all that we don’t).

Perhaps anotherblock and all of the other blockchain-based royalty sellers will share some more transparent math and their feelings about SEC regulation in the near future.

Until then? Buyer beware. The “Bitch” may turn out to be you not having your money after all.Music Business Worldwide