Another day, another chapter in the Hipgnosis Songs Fund (HSF) drama.

This morning (January 23), the UK-listed company’s board – led by Chairman, Rob Naylor – issued a new note to investors that, once again, appeared to express frustration with HSF’s investment adviser – aka Hipgnosis Song Management (HSM), led by Merck Mercuriadis.

I’ll get to that shortly. First, some necessary nuggets of context:

- As explained by MBW here, the Hipgnosis Songs Fund board last week announced a proposal for shareholders whereby any prospective bidder for HSF’s portfolio offering “recommendable terms” would be paid a one-off bung of up to GBP £20 million;

- The purpose of that proposed bung: To entice would-be bidders to make acquisition offers despite the ongoing presence of a ‘call option’ held by HSM;

- This ‘call option’ decrees that, should HSM ever be fired as HSF’s investment adviser, a clause would be triggered that enables HSM to acquire HSF for a pre-set sum;

- That pre-set sum – and the importance of mentioning this will become clear shortly – would be the higher of: (i) Hipgnosis Songs Fund’s currently-in-the-quagmire public market capitalization; (ii) Hipgnosis Songs Fund’s ‘fair value’ as adjudicated by an independent valuer; or (iii) The price that a separate and credible third-party is willing to pay to acquire HSF (i.e. a matching right).

What happened today?

So. Following Rob Naylor and co’s £20 million ‘bung’ announcement last week, it transpired that Merck Mercuriadis and co. had – two days before that ‘bung’ announcement – actually made an offer to the HSF board that few of us thought would ever transpire.

HSM and Mercuriadis were now willing to extinguish their ‘call option’, in exchange for a multi-year guarantee that HSM would continue as HSF’s investment adviser.

Today, Naylor and his board at HSF have essentially publicly dismissed this offer. Look out for the all-important word – “unconditionally” – in their statement here:

“The Newly Constituted Board has requested for the Investment Adviser, Hipgnosis Songs Management, which is majority owned by funds managed and/or advised by Blackstone, to unconditionally remove the Call Option from its Investment Advisory Agreement with immediate effect to act in the best interests of shareholders as a whole. This request has been refused.”

We now appear to be back at a circular impasse:

- The HSF board wants Mercuriadis to torch his ‘call option’ without conditions;

- Mercuriadis – understandably, if you put yourself in his shoes – isn’t exactly thrilled about deleting a clause that was very deliberately inserted into the HSF prospectus in 2018 to protect his connection to these copyrights;

- Instead, seemingly to keep the peace (and to avoid further agitation of HSF shareholders), Mercuriadis now says he is willing to rip up the ‘call option’ – so long as he gets the protection of a few years of continued work as HSF’s investment adviser;

- The HSF board says no to that trade… and wants him to torch his ‘call option’ without conditions.

Rob Naylor and Round Hill

Ultimately, here’s the reason the HSF board despises Mercuriadis’ ‘call option’ so much: they claim it will damage the potential price that the HSF portfolio could fetch on the fair market – i.e. the amount of money that would be paid through to HSF’s public shareholders when they sell.

This is borne out not only in the £20 million ‘bung’ plan, but also by Rob Naylor’s own comments last week.

HSM/Mercuriadis’ call option, Naylor said in a note to shareholders “not only acts as a structural conflict between the interests of our shareholders and the Investment Adviser” but also “creates a significant deterrent to potential bidders for [HSF’s] assets thereby depressing the value of the Company”.

Yet, digging deeper into the documentation, there’s something a bit strange about this.

Again, I’ll get to why shortly, but first… some more necessary nuggets of context:

- Rob Naylor was previously Chairman of Round Hill Music Royalty Fund Ltd (RHMRF). That fund, like HSF, was listed on the London Stock Exchange. And, like HSF, its public valuation was over the past year dragging below the ‘fair value’ that was placed on the company by its independent valuer;

- Then, in September 2023, Naylor and his board at RHMRF delivered good news to their shareholders: Alchemy Copyrights, LLC – trading as Concord – had made an offer to acquire RHMRF’s portfolio for USD $468.8 million;

- That offer, it was said at the time, represented an 11.5% discount on the economic NAV of RHMRF (i.e. the valuation of RHMRF according to its independent valuation);

- Shareholders approved the deal, it went through in November.

Rob Naylor’s view on Concord’s offer was unequivocally positive.

In September, he told RHMRF’s shareholders that it represented “excellent value for shareholders”.

In addition, he noted that the offer brought with it an “opportunity for liquidity at a premium to both the share price and the IPO price, as well as at a narrow discount to economic net asset value per share”.

And once the shareholders approved the Concord acquisition, in November, Naylor further crowed about a “resounding endorsement of the value that [the RHMRF board] have been able to deliver on [shareholders’] behalf”.

Can you see why HSF shareholders were so keen to appoint Naylor as their Chairman now?

Naylor has a proven track record of ‘working’ the private market to get the best possible acquisition price for a public music fund that is trading at a discount vs. its ‘fair value’.

The obvious conclusion: HSF shareholders now want him to perform the same trick twice.

And he probably could, of course, if it weren’t for that blasted ‘call option’! Which… what were Naylor’s words again? Oh yes: “Creates a significant deterrent to potential bidders for [HSF’s] assets thereby depressing the value of the Company.”

Only one issue there. RHMRF’s investment manager – Round Hill Music LP, run by music entrepreneur Josh Gruss – also had a ‘call option’.

And it was startlingly similar to HSM/Merck Mercuriadis’ ‘call option’ at Hipgnosis Songs Fund.

A tale of two call options…

Following all the backbiting at HSF last week, MBW decided to dig back through Round Hill Music Royalty Fund Ltd’s prospectus, published in 2020.

The aim: to see if there was anything comparable to the HSM/Mercuriadis ‘call option’ (the one now causing all the mischief and mayhem) located in Hipgnosis Songs Fund’s 2018 prospectus.

Well… “comparable” doesn’t quite do what we found justice.

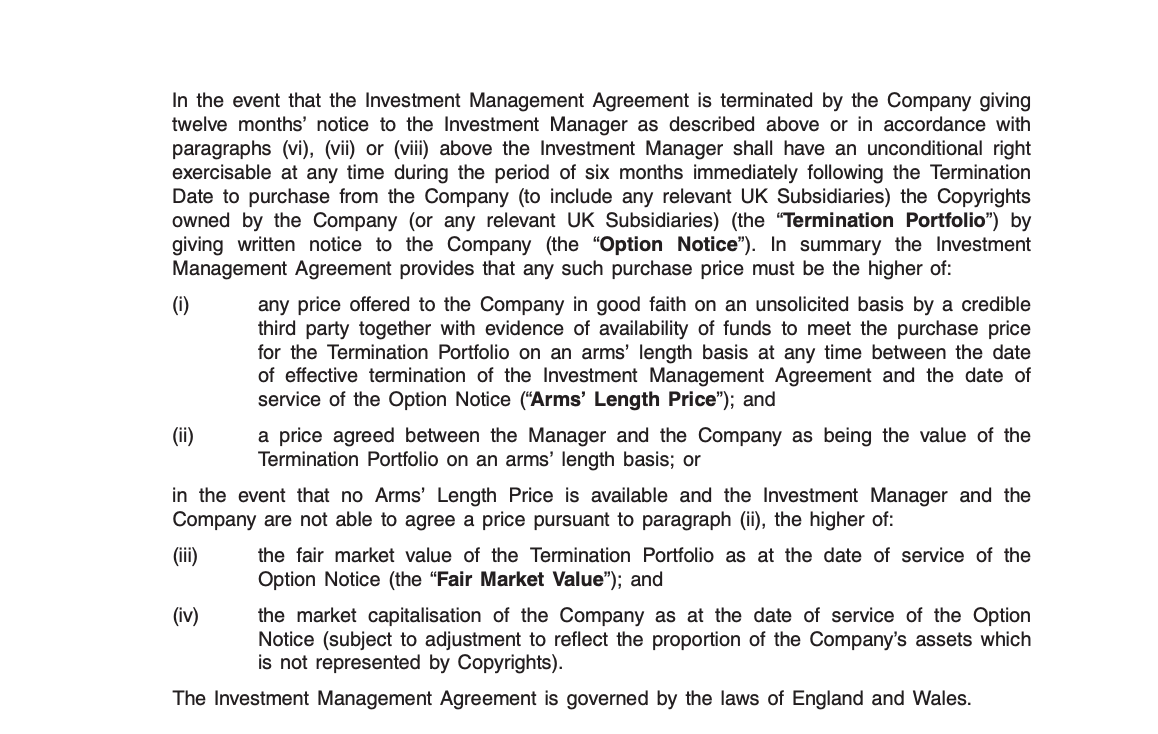

Below, you can read Round Hill’s ‘call option’ clause, on page 107 of its UK-listing prospectus from four years ago.

This ‘call option’ applied throughout the publicly-traded life of Round Hill Music Royalty Fund Ltd.

As you can see, this ‘call option’ very clearly gave Round Hill Music LP an “unconditional right” to acquire RHMRF for a six-month period should the RHMRF board ever terminate Round Hill Music LP as RHMRF’s investment manager.

To exercise that ‘call option’ and acquire these rights, Round Hill Music LP (i.e. Josh Gruss) would have had to pay the higher of:

- (i) RHMRF’s public market capitalization;

- (ii) RHMRF’s ‘fair value’ as adjudicated by an independent value;

- (iii) The price that a separate and credible third-party was willing to pay to acquire RHMRF (i.e. a matching right); or

- (iv) A price privately agreed between Round Hill Music LP and the RHMRF board.

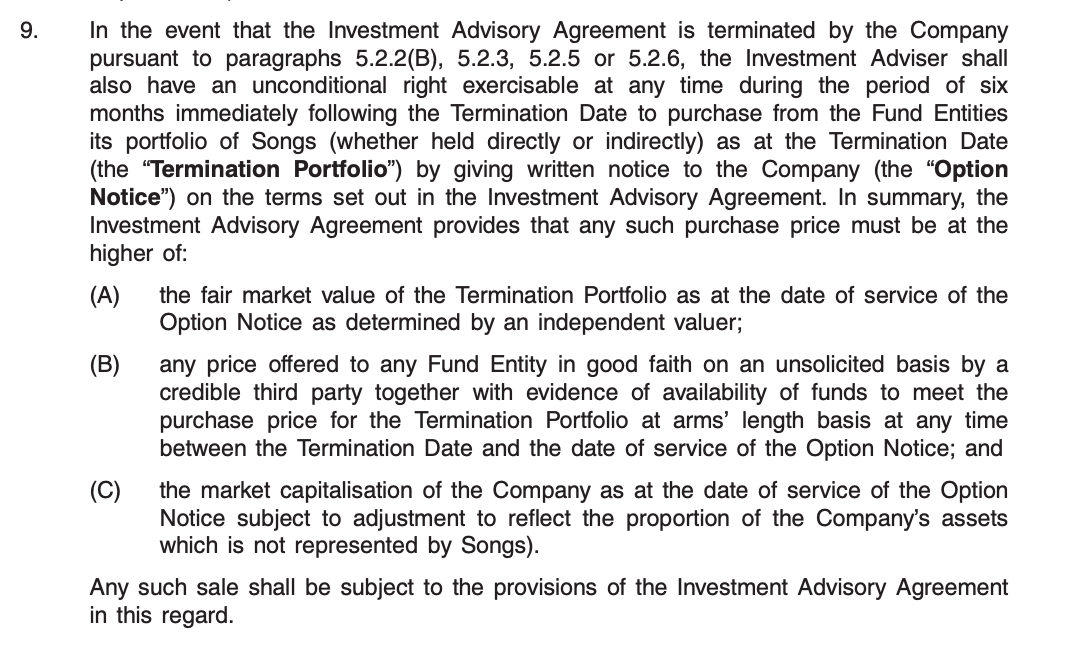

Now let’s take a look at Merck Mercuriadis’ ‘call option’ at Hipgnosis Songs Fund, from that company’s 2018 prospectus:

I mean.

It’s pretty uncanny, right?

The head-scratcher

So riddle me this.

How can it be that Round Hill’s investment manager had in place a near-identikit ‘call option’ at RHMRF to the one Merck Mercuriadis had/has at HSF. Yet, at RHMRF, it was no barrier to shareholders getting a blinding deal… but at HSF, it is?

Just to remind you, in the words of Rob Naylor:

- HSM/Merck Mercuriadis ‘call option’? That “creates a significant deterrent to potential bidders for the… assets thereby depressing the value of the Company”

- But Round Hill/Josh Gruss’ ‘call option’? That was no obstacle to a third-party acquisition offer that represented “excellent value for shareholders”.

Puzzling.

Hipgnosis Songs Fund shareholders may soon get an opportunity to quiz Rob Naylor and his board about this: An Extraordinary General Meeting (EGM) of HSF shareholders – ostensibly for HSF investors to vote on the £20 million ‘bung’ idea – is now set for February 7.

Meanwhile, a ‘strategic review’ of HSF continues to rumble on in the background, conducted by Shot Tower Capital.

Stay tuned.Music Business Worldwide