July 2023 marked the first time in its 15-year history that Spotify increased its flagship subscription price point in the UK (and many other territories).

Since that point, an individual monthly Premium subscription to Spotify in the UK has cost GBP £10.99, as opposed to its previous price of £9.99; the platform’s Family Plan tariff has moved from £16.99 per month to £17.99 per month.

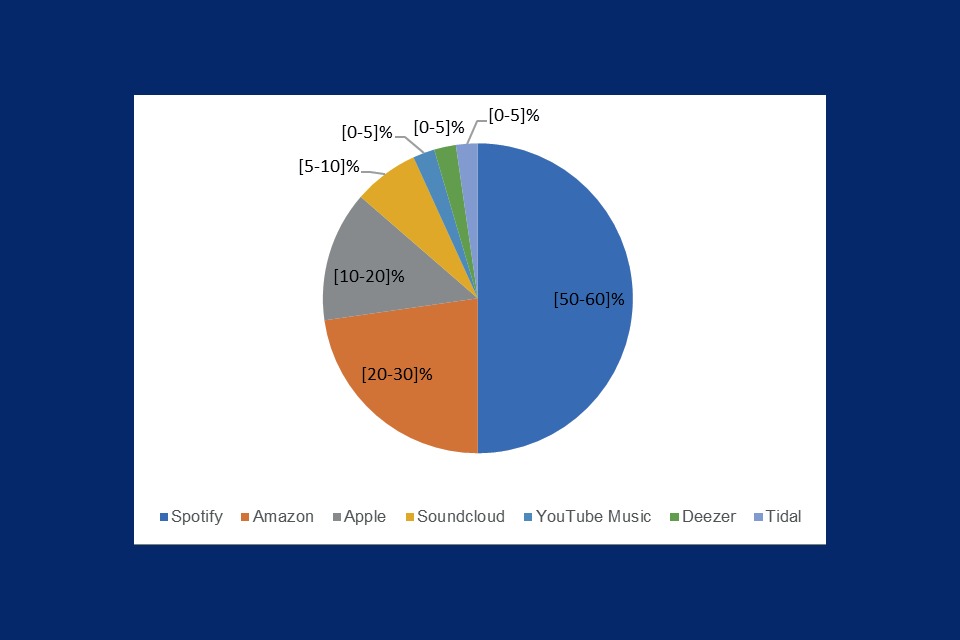

This tweak in Spotify’s pricing was bound to have a significant effect on the UK market’s value: Data captured by the Competitions and Markets Authority (CMA) shows that in December 2021, Spotify’s market share of all music streaming’s monthly active users (‘free’ plus ‘premium’) in the UK stood at over 50% (see below).

Now, for the first time, we can see the impact of Spotify’s 2023 price rise within official industry numbers for the UK (the world’s third-largest recorded music market, according to IFPI).

The UK’s Entertainment Retailers’ Association (ERA) is a trade org whose members include the likes of Spotify, Amazon, YouTube, and SoundCloud.

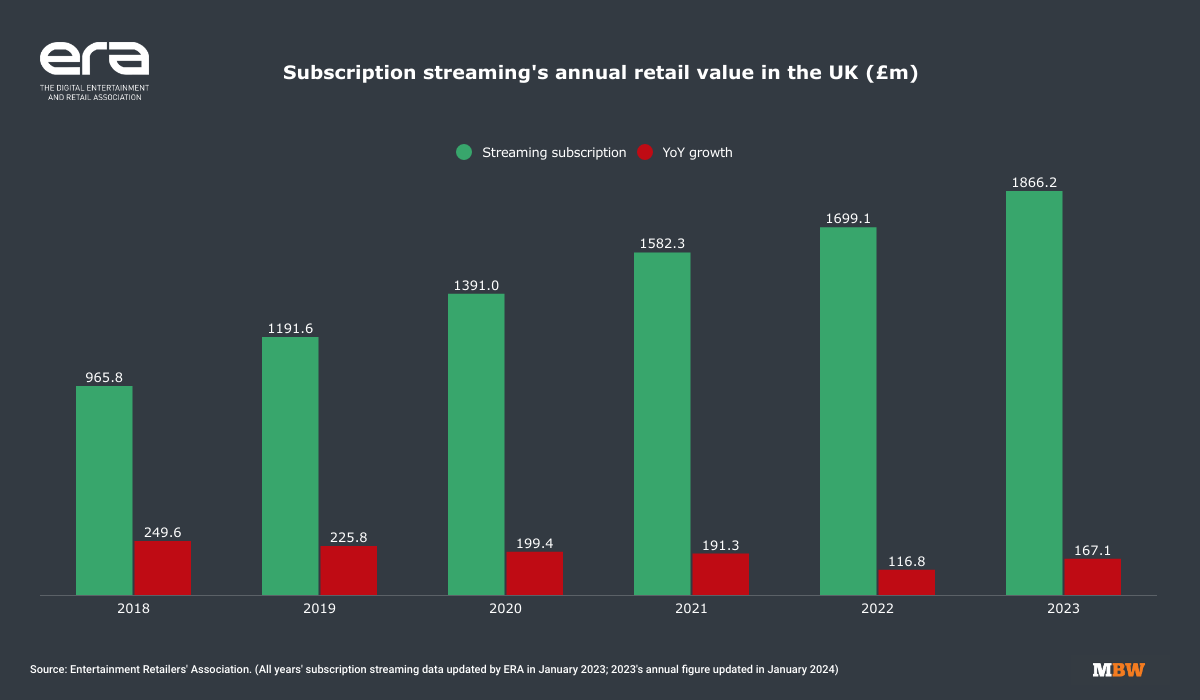

Today (January 9), ERA has published fresh data showing that annual consumer spending on music streaming subscriptions in 2023 rose 9.8% YoY to GBP £1.866 billion (USD $2.32bn).

In monetary terms, that represented a YoY increase of GBP £167.1 million (USD $208m), up from the GBP £1.699 billion generated in the UK in 2022.

(To reiterate: ERA’s data reflects the amount of money spent by UK consumers on music streaming subscriptions – not the wholesale figure being paid through to music rightsholders. It does not include advertising revenues generated on digital services.)

In addition to Spotify, the above numbers will also have been affected by similar UK price rises by other streaming services such as Apple Music (October 2022), Amazon Music (January 2023), and YouTube Music/Premium (August 2023).

The success of these price rises – as clearly manifested in the near-10% YoY industry revenue rise – will no doubt stimulate conversations around the global business as to when we might see the next Spotify/Apple Music/YouTube Music/Amazon Music price hike.

Something else that may stimulate these conversations?

How the 2023 growth of the UK recorded music industry would have looked without said price rises, which in their most basic form – i.e. monthly individual subs rising from £9.99 to £10.99 – represented a 10% increase in monthly payments from continuing subscribers.

In a memo to staff yesterday (January 8), obtained by MBW, Warner Music Group boss, Robert Kyncl, made a strong nod towards the subject of further streaming price rises.

Kyncl noted that “increase[ing] the value of music” was one of WMG’s top priorities for 2024 – a mission that, he said, included a “need to align our DSP relationships so that we… maximize [the] price opportunity for our music“.

Kyncl’s comments came four months after one of Spotify’s rivals, Deezer, announced that it was raising its prices in multiple territories for the second time in 12 months.

Deezer’s flagship individual premium price in the UK stands at GBP £11.99 per month, a pound more expensive than Spotify, YouTube Music, Apple Music, and Amazon Music’s equivalent prices (£10.99). Deezer’s Family Plan in the UK costs £19.99 per month vs. £17.99 for Spotify’s equivalent.

Adding to the chorus of calls for further price rises in music streaming: Bill Ackman, the founder of Pershing Square Holdings, which leads a group of investors who own 10% of Universal Music Group.

In March 2023, Ackman celebrated recent price rises at Apple Music and Amazon Music by noting in a Pershing Square investor update: “We believe that breaking the $10 [monthly price] barrier is a watershed moment, as other platforms will likely follow suit, and regular price increases will become the norm in the audio streaming industry as they are in the video streaming industry.”

Meanwhile, Goldman Sachs predicted last summer that average streaming subscription prices in developed markets like the US and the UK would grow, on average, by 3% per year in the medium-term future.

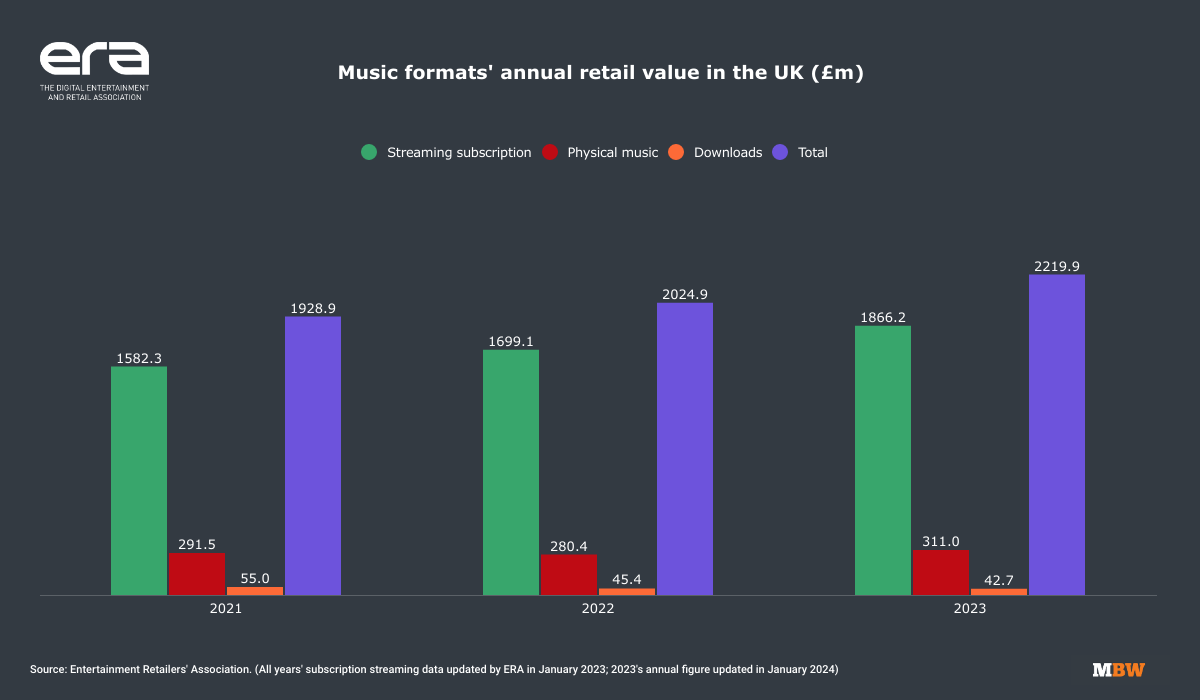

In addition to streaming revenues, ERA’s latest numbers also cover physical music sales and downloads. (ERA’s members include UK physical music retailers such as HMV and ASDA, plus a network of independent retailers).

Annual UK physical music revenues (across CD and vinyl sales) were up 10.9% YoY in 2023 – totaling GBP £311.0 million (USD $387m).

Download sales were down 5.9% YoY, to GBP £42.7 million (USD $53m).

Total UK 2023 recorded music sales – including subscription streaming, physical music, and downloads – stood at GBP £2.2199 billion (USD $2.76bn), up 9.6% YoY.

That GBP £2.2199 billion figure, said ERA, was the UK recorded music industry’s highest annual revenue tally since 2022, and just 0.08% below music’s all-time annual high of 2001. (These comparisons don’t take into account inflation from 2001 to now.)

ERA CEO Kim Bayley said, “With revenues just a fraction away from music’s all-time-high, this is a red letter day for the music industry and is a testament not just to the creativity of artists, but to the entrepreneurial drive of digital services and retailers.

“A world without streaming now seems unthinkable. Meanwhile the tenacity of physical retailers has driven not just the vinyl revival, but a surprise increase in the value of CD sales. Given all we’ve been through, it really doesn’t get much better than this.”

All GBP-USD conversions made at average 2023 annual exchange rate as per IRS data.Music Business Worldwide