The MBW Review is where we aim our microscope towards some of the music biz’s biggest recent goings-on. This time, we look into the UK competition watchdog’s investigation into Sony‘s acquisition of AWAL from Kobalt. The MBW Review is supported by Instrumental.

Sony Music having to dispose of AWAL due to a UK competition watchdog’s clampdown: it’s not a prospect many in the music industry would relish.

Even Sony’s fiercest rivals – Universal and Warner – would surely have grave concerns about the “chilling effect” such an outcome might have on the market.

Then there’s the uncertainty for AWAL itself, not to mention its artists, which include the likes of Girl In Red, Finneas, and Little Simz.

Yet it’s an outcome that took a further step towards becoming a reality today (September 16), with the UK’s Competition and Markets Authority announcing that it is moving its inquiry into Sony’s acquisition of AWAL to ‘Phase Two’.

As a result, an independent UK panel will be called upon to look further into the CMA’s concerns over the buyout, which saw Sony Music buy AWAL’s global business (alongside Kobalt Neighbouring Rights) for $430 million in May.

The CMA’s initial ‘Phase One’ announcement about its concerns portrayed a body with a surprisingly nuanced level of knowledge about the modern music business.

For one thing, it’s clearly done its research into the difference between a record label and an artist services company, and how artist deal terms typically differ between these two types of industry player.

The CMA is also spot on when it suggests that AWAL helped pile pressure on the major record companies (and their own label/artist services businesses) to offer artists bigger advances and better royalty terms.

As Kobalt founder and Chairman Willard Ahdritz declared in 2018, while announcing Kobalt’s $150 million investment into AWAL: “We are fundamentally changing the cost structure of the recorded music business.”

Yet the CMA’s central thesis – that, had Sony Music not bought it, AWAL would have gone on to be a strong independent company under Kobalt’s ownership – warrants real scrutiny.

First things first, here’s what the CMA has actually said about Sony Music’s AWAL buyout (which has not triggered similar competition concerns in Europe or in the US).

A press release issued by the CMA on September 7 read: “The CMA found evidence that – if the deal had not gone ahead – Sony and AWAL could have competed more strongly with each other in future,” adding that: “AWAL was well-placed to grow its business even further in the coming years.”

It’s here we need to begin chewing over the finer details of Kobalt’s own business.

In the past, to accelerate the growth of its various music divisions – including AWAL, plus Kobalt Music Publishing, Kobalt Neighbouring Rights, AMRA and more – Kobalt Music Group took out a loan that amounted to $185 million.

This loan, plus interest, was due for repayment in 2023.

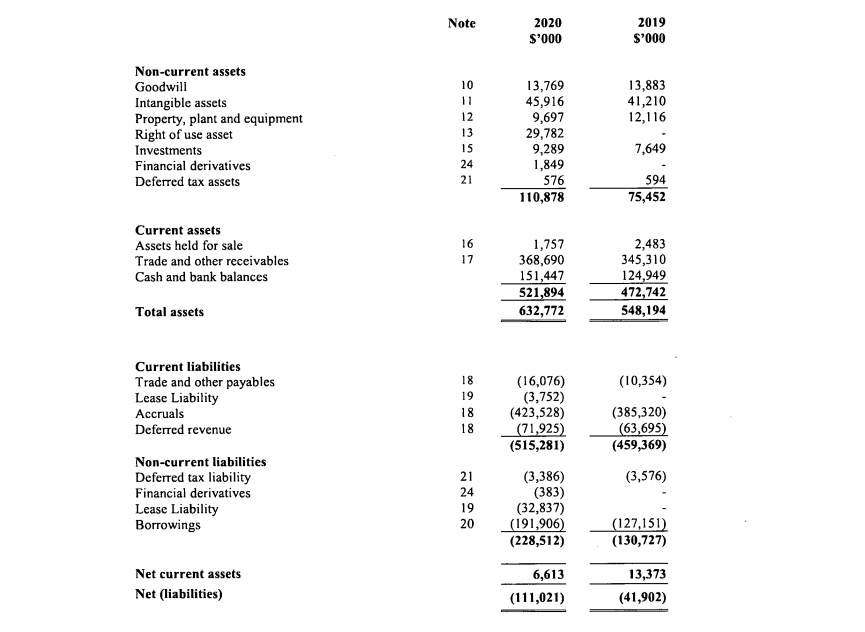

Partly because of this loan, Kobalt closed the financial year ending June 2020 with $111 million in net liabilities – the difference between the assets it owned (including cash) and the liabilities it owed.

It didn’t have enough in cash at this stage ($151.5m) to cover the loan payback.

Some claim that having net liabilities on a balance sheet amounts to “accounting insolvency”.

But in truth, especially for a company prioritizing growth over profits, it’s no disaster… so long as the firm in question has a plan to claw their way back from those net liabilities.

And to do that – other than slashing its expenses – a business like Kobalt has three obvious remedies to turn to:

- (i) Take on more investment to increase your cash pile so you can pay off your liabilities in the short-term;

- (ii) Most importantly, start posting profits – as you can then ‘chip away’ at your liabilities as the years go by; or

- (iii) Sell off a juicy asset for as much money as you can get.

In the end, having found a willing buyer in Sony Music, Kobalt chose option (iii).

Today, thanks to the AWAL deal, Kobalt is a transformed company.

For starters, it’s debt free: Kobalt has confirmed to MBW that it’s used the proceeds from the AWAL deal to pay off its $185 million loan (and a bunch of interest).

In addition, Kobalt has spent $89 million in additional cash (post-AWAL deal) on paying shareholders some of that sweet AWAL dollar, via multiple equity buybacks.

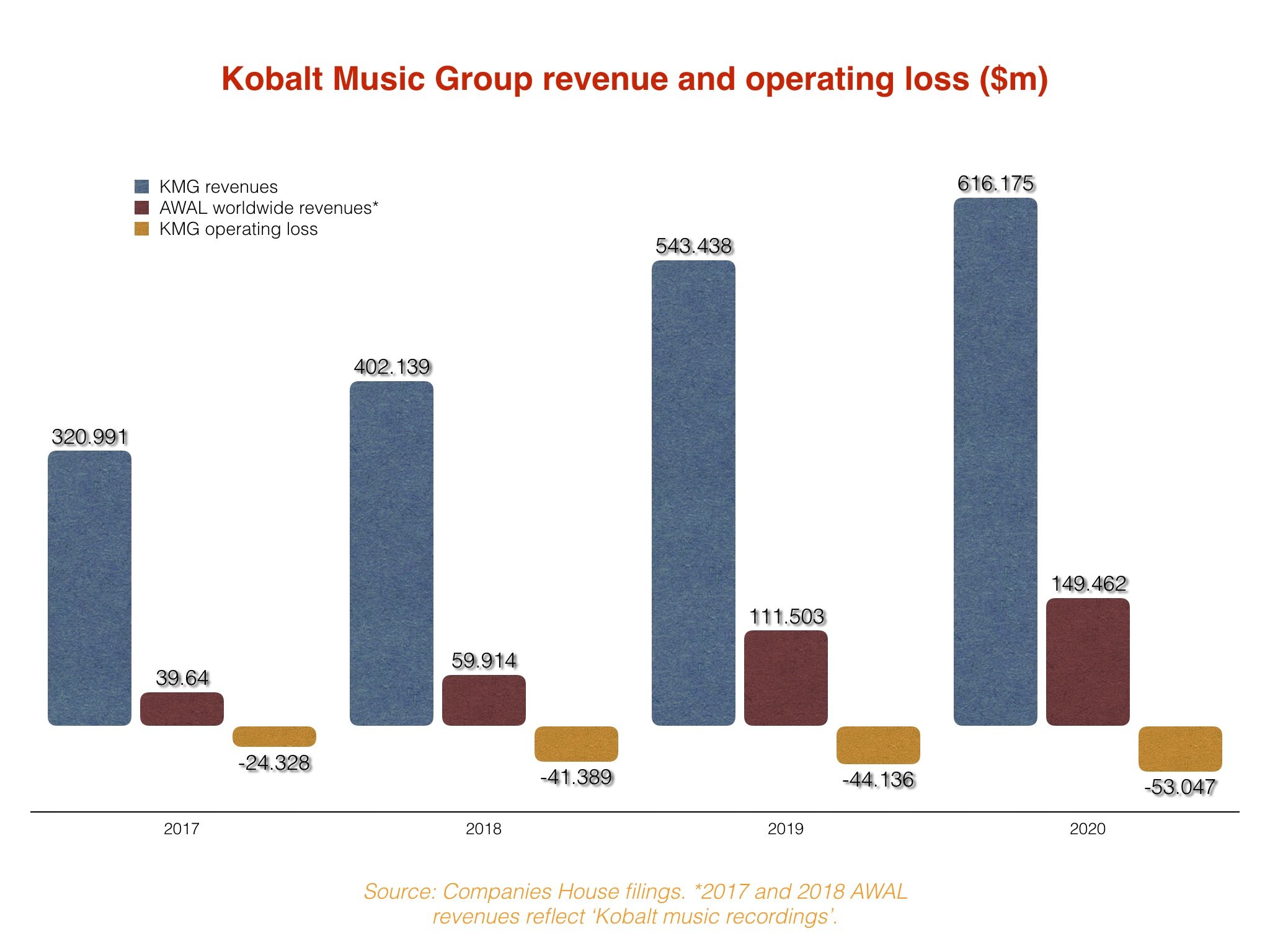

Thirdly, Kobalt says that, after years and years of posting annual losses – including a $53 million operating loss in FY2020 – it became a profitable entity during its last fiscal year, to the end of June 2021 (i.e. the year it sold AWAL to Sony).

This is all good news for anyone who wants to see one of the music industry’s most transformative companies in rude, rather than vulnerable, fiscal health.

But it doesn’t take away from this fact: If Kobalt hadn’t sold AWAL to Sony Music, it’s not obvious to see a way in which it would have turned around its net liabilities balance – especially with the clock ticking down to the 2023 pay-back date of that $185 million loan.

An important fact at this juncture: Although Kobalt’s competitors in the industry have long liked to titter and point at the company’s annual loss-making status, Willard Ahdritz has stated for years that the firm’s publishing operation is profitable.

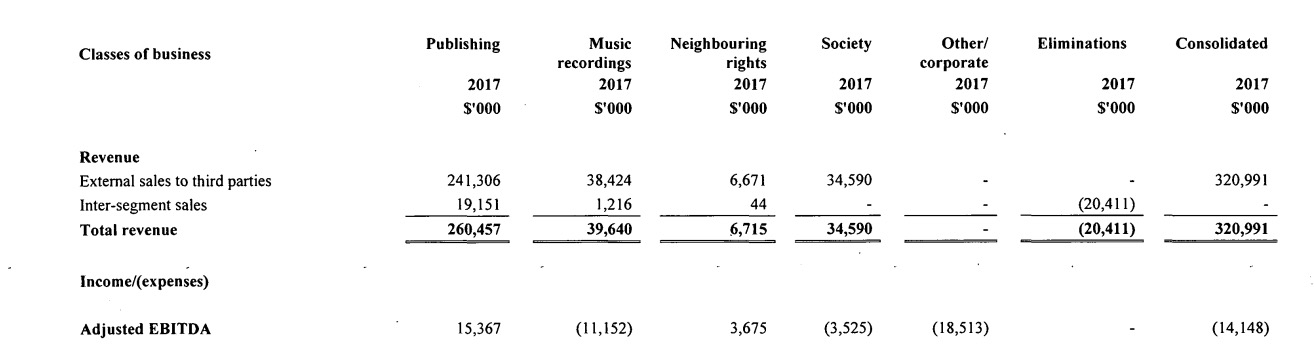

The numbers back him up: Kobalt’s accounts show that as far back as 2015, Kobalt’s publishing division was posting positive EBITDA numbers as a standalone entity – and that by FY2017, it was posting an adjusted annual EBITDA of $15.4 million.

Kobalt Music Group, though – across all of its divisions – was still perennially making a loss.

And a large part of that story was its music recordings division, which in FY2017 posted an $11.1 million adjusted EBITDA loss on $38.4 million in revenue.

Then, in 2018, Kobalt transformed its recorded music business, completely rebranding it to AWAL, and trusting its future to AWAL’s innovative tiered system of artist investment.

(You can read more about that tiered system here, but in essence: DIY artists upload their music to a gated system. If AWAL likes it, they take on distribution and basic services; if that goes well, they charge a bit more and give you more services; and if that goes well, they charge you a bit more still and invest in you much like an indie record label would.)

That wasn’t the only thing that changed: From FY2018 onwards, Kobalt no longer printed an Adjusted EBITDA number for each of its divisions in its annual accounts.

Instead, it reported a revenue figure for each division, and – aside from a ‘contribution margin’ number – gave little clue as to the profitability or otherwise of each part of its company.

What we do know, however, is that Kobalt Music Group itself continued posting material annual losses in FY2018, FT2019, and FY2020 – despite its publishing division seemingly being profitable since 2015.

So where were these losses coming from – and how much was down to AWAL?

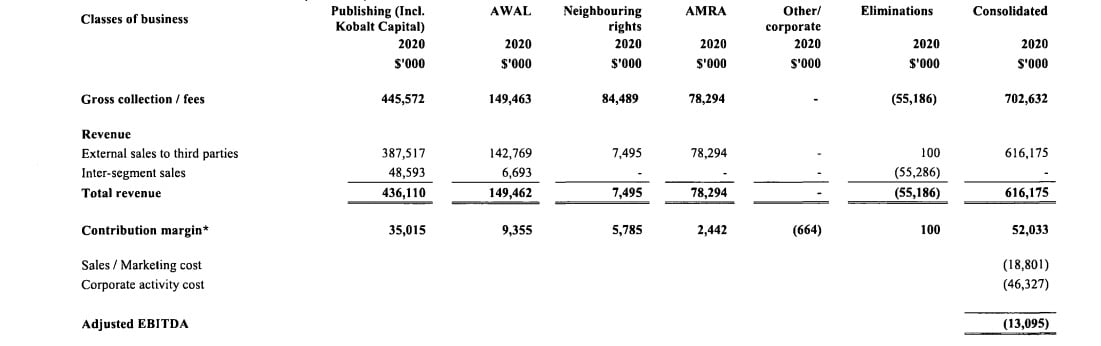

Kobalt’s FY2020 results show that AWAL posted a $9.4 million ‘contribution margin’ – defined as gross profit minus ongoing service costs.

But Kobalt also counted company-wide “sales/marketing costs” and company-wide “corporate activity” costs separately to its various music divisions (see below).

This complicates things. Not least because had even a sixth of Kobalt’s total “sales/marketing costs” and “corporate activity” costs in FY2020 ($65m) been attributed to AWAL, then AWAL’s ‘contribution margin’ would have gone negative.

(Kobalt Music Group – as in, the whole group – posted a +$52m ‘contribution margin’ in FY2020; it also posted a $53m operating loss.)

We can perhaps get a better steer of AWAL’s profitability in FY2020 by looking at the accounts of the two main UK subsidiaries of Kobalt that bear its name: AWAL Recordings Ltd and AWAL Digital Ltd.

Unfortunately, it’s hard to tell how much of AWAL’s total worldwide costs these two UK limited companies reflect and, indeed, share.

Adding to the fogginess of AWAL’s numbers, Kobalt also owned two registered AWAL-branded incorporated companies in the United States, whose accounts are unavailable.

Still, it’s a start.

- AWAL Digital Ltd was operationally profitable in FY2020, posting GBP £100 million in revenues, alongside a £2.99 million operating profit – a slim margin of a whisker under 3%.

- AWAL Recordings Ltd, however, was not profitable: it posted FY2020 revenues of £30.7 million, alongside a £7.06 million operating loss.

Why are we fumbling around trying to ascertain the level of AWAL’s profitability (or, more likely, unprofitability) in Kobalt’s last available fiscal year?

Simple: If Kobalt owed $185 million plus interest for a loan, didn’t have to cash to cover it, and had net liabilities of over $110 million… and if AWAL was materially contributing to Kobalt’s annual losses, despite the profitability of its publishing division… it becomes much, much harder to argue that AWAL had a bright future ahead of it before Sony Music snapped it up this spring.

As such, it is now incumbent on the CMA’s independent panel to look closely at AWAL’s finances – especially if they’re in the red – and keep one question front and center:

AWAL was a company built to challenge and destroy the major record companies’ “stupid deals”. So much so, it was literally named Artists Without A Label. So why would Kobalt Music Group sell it to the world’s second biggest major music company… unless it really had to?

(While I’m here, I’d also encourage the CMA’s independent panel to avoid getting too Brexit-y by over-relying on UK-only market data. Music is a globalized business: economic research from Spotify shows that four in every five streams of the average UK artist happens outside the borders of their own country.)

None of the above, by the way, takes away from AWAL’s electric impact on the global recordings market, nor diminishes the sheer disruption its low-margin, artist-friendly business has had on the record industry’s biggest players.

In its initial report about the Sony deal, the CMA rightly asserts that “AWAL had the ability and incentive to become a more significant competitor in digital music distribution in the UK”.

That’s not in dispute.

The more crucial question: Did it have the money?