Credit: BIGHIT MUSIC / NETFLIXBTS's comeback performance in Seoul's Gwanghwamun Square in March

MBW Views is a series of op-eds from eminent music industry people… with something to say. The following op/ed comes from author and music economist Will Page, and Jeongbeom ‘JB’ Kim, Chief Data Officer at the Korean-based KreatorsNetwork (pictured L-R, inset).

Page and Kim argue that K-pop is now a global phenomenon, entering mainstream charts and conversations alike, yet, when fans are asked to count how many K-Pop artists they actually follow, “don’t be surprised if they don’t need to use all the fingers on one hand”.

They ask: “Why, unlike genres like rap and rock, is K-Pop’s attention being paid to the few, and not the many, and will BTS’s return to stages and screens help or hinder the broader genre?”

Will Page and Jeongbeom ‘JB’ Kim explore this K-Pop dilemma in the exclusive analysis below…

Laying out the long tails of K-Pop

Doing a data deep dive on K-Pop sounds easy in theory, but becomes very tricky in practice for one simple reason: ambiguity-in-definition.

What actually is K-Pop?

Not all Korean music counts, of course. And further muddying the waters is the rise of J-Pop, so infused with Korean training on stage (and Korean executives backstage) that it is often termed ‘J-K Pop’.

Working with Luminate’s excellent streaming data platform, we’re able to isolate K-Pop to music performed by teen idol acts, chiefly a boy or girl band (BTS, BLACKPINK) from Korea’s idol system, with a strong focus on charismatic visuals and captivating choreography.

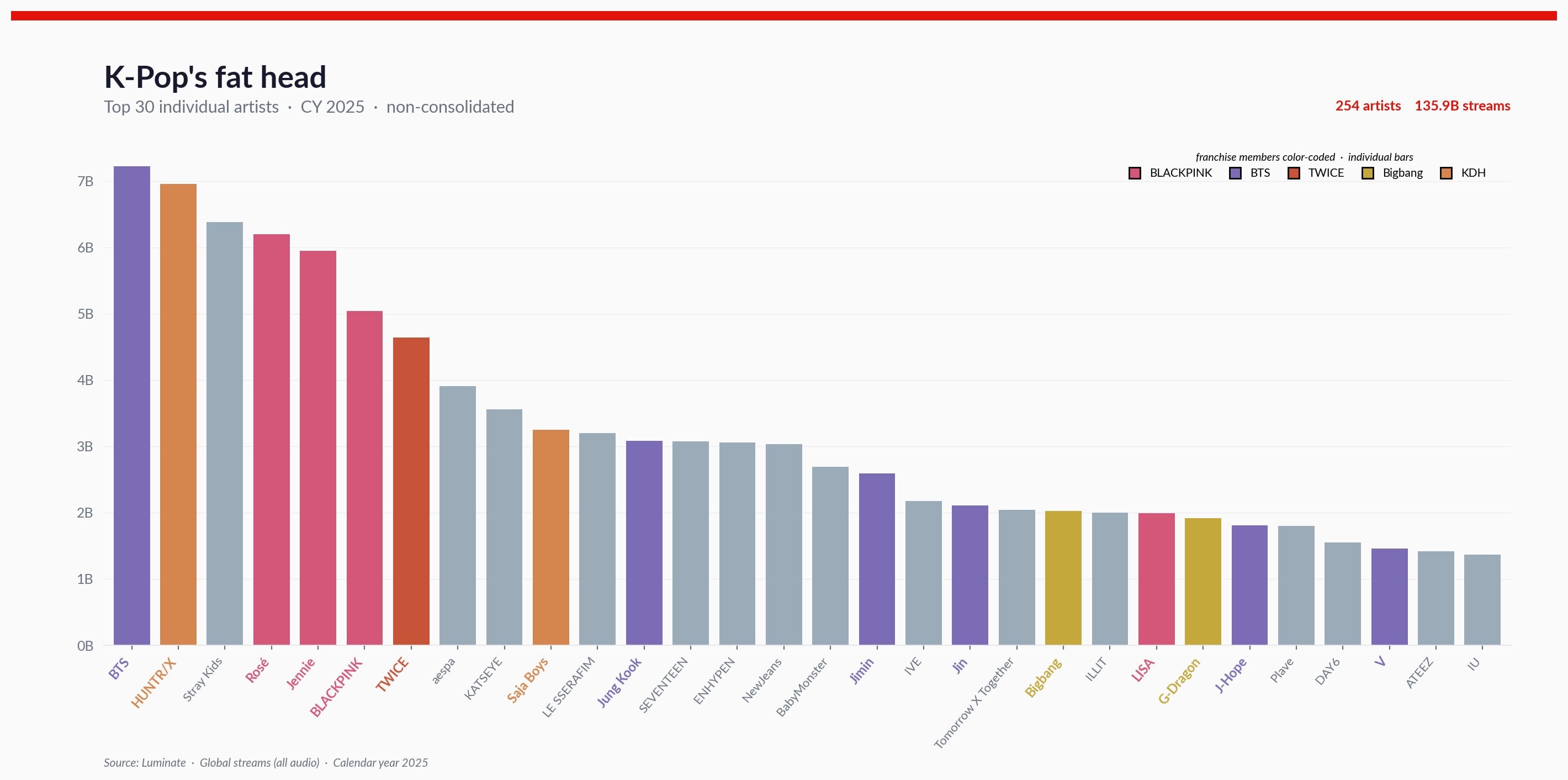

A redefined deep-dive on the data that strips out all the noise (including hyper-local Korean genres like ‘Trot’) leaves us with 254 K-Pop artists who tallied 136 billion total global streams last year.

That means K-Pop got just a 2% market share of global streaming.

What’s even more striking is that K-Pop streaming volumes are actually down a touch on the prior year.

At first glance, ranking those 254 artists by global streams, it appears the top 30 captured 72% of the K-Pop streams in 2025. BTS were still the leaders of the pack, despite being on hiatus since 2022.

Sliced and diced this way, though, the data is deceptive.

There’s a ton of bundling to be done, with many solo artists on the list featuring alongside their own established ‘franchise’ groups. Rosé and JENNIE are part of BLACKPINK, Jungkook and Jimin are members of BTS, and HUNTR/X and Saja Boys are part of the K-Pop Demon Hunters.

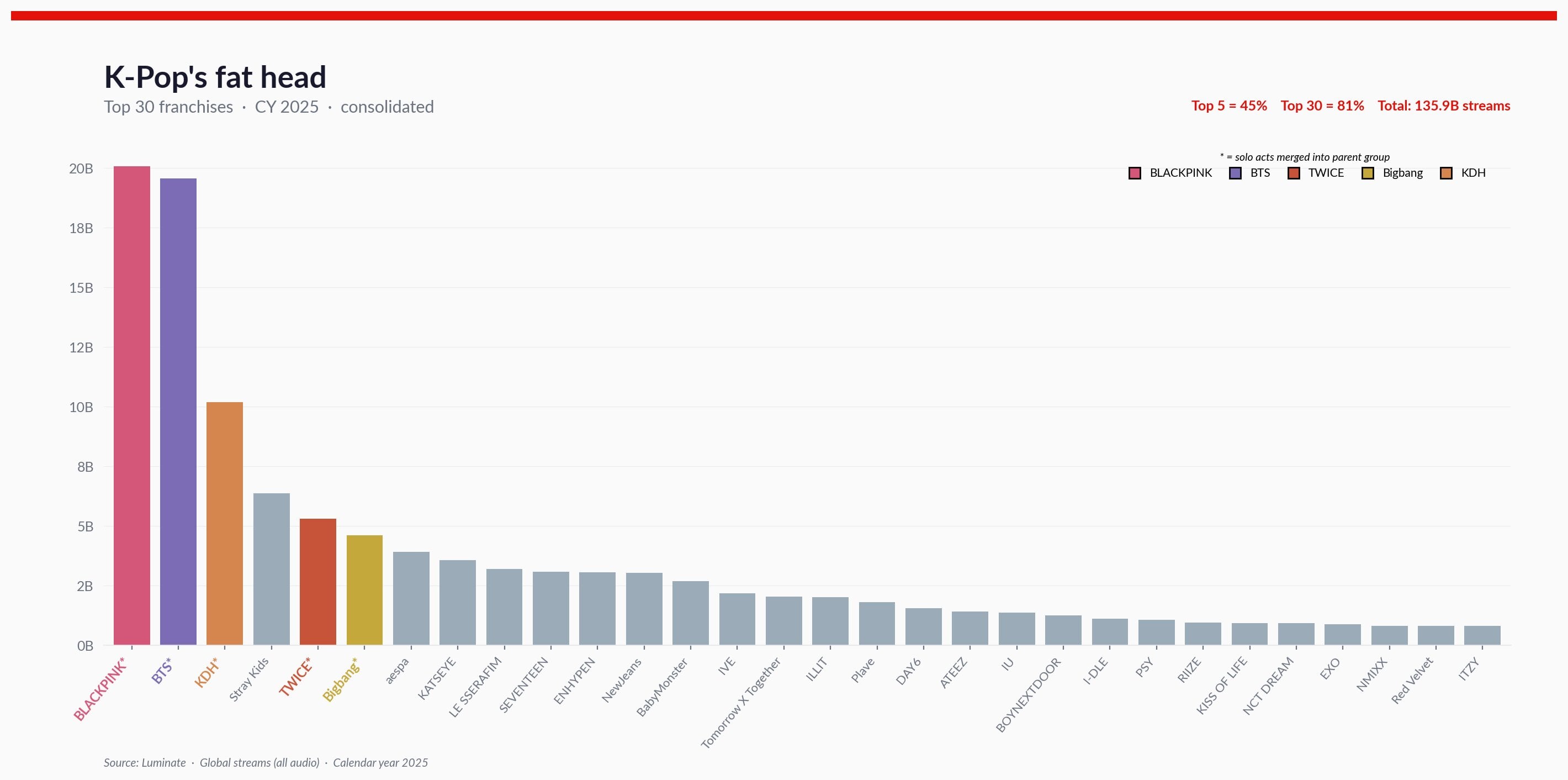

Once you roll them into their respective franchises, the top five entities (ordered BLACKPINK, BTS, KPDH, Stray Kids and TWICE) capture a whopping 45% of K-Pop’s demand.

JH Kah, former CEO of HYBE Latin America, stresses this is where the hierarchy becomes clear: “Within the fandom economy, attention and money flows upward to the most culturally dominant acts.”

“Within the fandom economy, attention and money flows upward to the most culturally dominant acts.”

JH Kah (former CEO of HYBE Latin America)

There’s deja vu to observe too.

A Korean-created market that is dependent on just five large players reminds us of the Chaebols – where the big five Korean conglomerates (Samsung, SK, Hyundai, LG, and Lotte) dominate the Korean economy.

Now what, so what?

BTS are back with a bang.

The Netflix show BTS Comeback Live | ARIRANG covering their return drew 18.4m viewers, and their new album, ARIRANG, has topped the Billboard album charts for a record-setting third week (their other six each spent only one week at No. 1). The boy band even penetrated the previously impenetrable Brazilian charts with the top slot. On July 19, they will reach the pinnacle, sharing the stage with Madonna and Shakira to headline the first-ever World Cup half-time show.

The question is: will a rising BTS tide help lift all boats or will BTS grab attention (and streams) at the expense of other K-Pop artists?

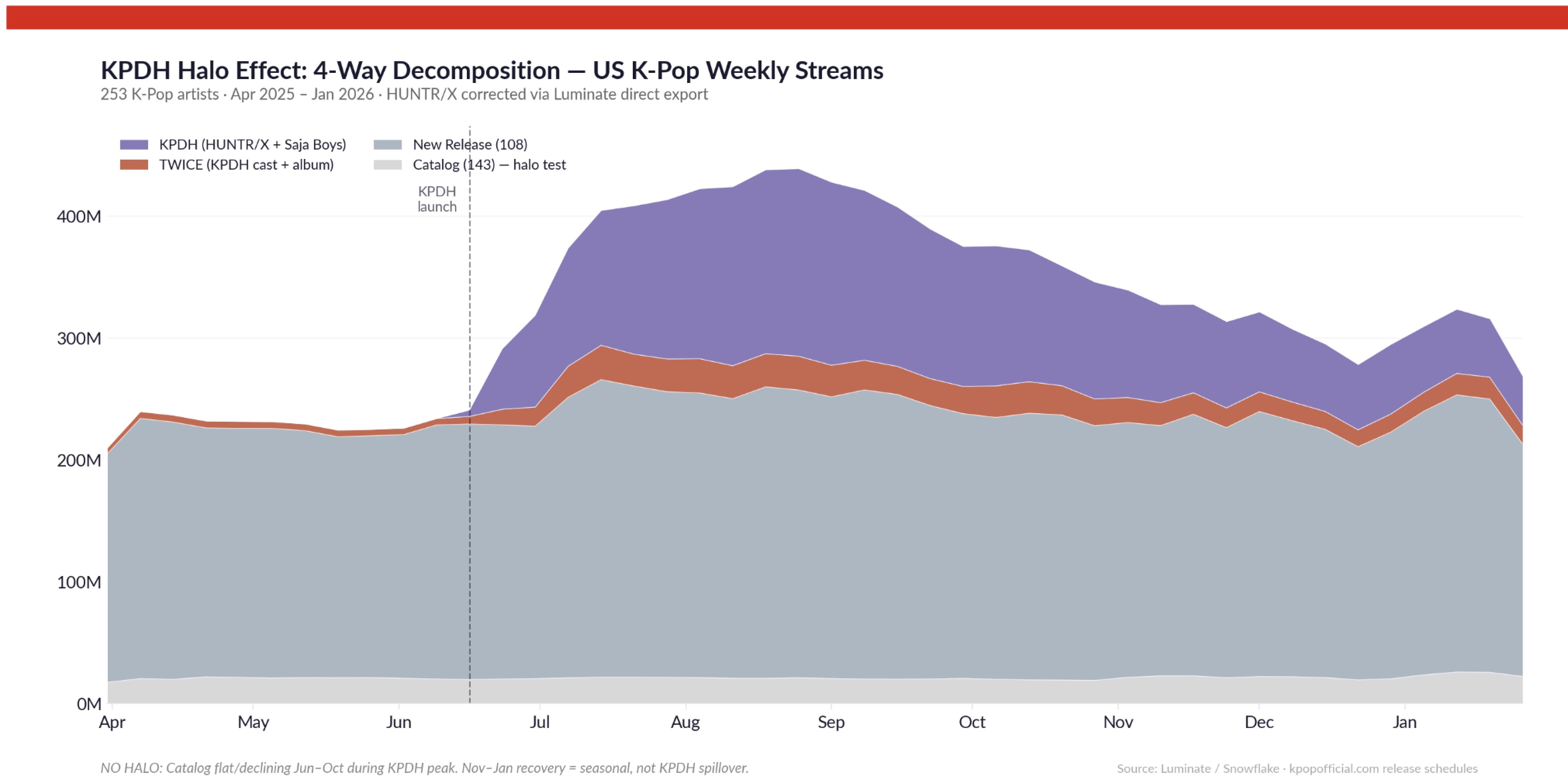

Smoke signals can be seen in the global success of K-Pop Demon Hunters. Plotting the Demon Hunters alongside other K-Pop tracks shows a rising Demon Hunters tide had little effect on other boats.

A ceiling on superfandom?

Economics is all about allocating finite resources given imposed constraints.

That finite resource could be either time or money. To maximize time or attention, K-Pop has pioneered the superfan strategy that now obsesses Western labels and analysts alike. But the data here indicate that this approach eventually runs up against constraints, and that becoming a superfan of one artist may come at the expense of others.

In addition to streams as a proxy for attention, there are monetary constraints, too — superfandom is an expensive hobby and disposable income is finite, so something has to give.

A lot of K-Pop artists have yearly membership fees. BTS offers two tiers: ARMY membership at 25,000 KRW ($17) and a (now discontinued) ARMY Merch Pack at 175,000 KRW ($115) KRW a year.

For context, an annual subscription to YouTube or Spotify costs only 143,000 KRW ($95).

What’s more, there are demographic constraints, especially in Korea with its shrinking population.

“BTS fans are not necessarily all-in, all-around fans of K-Pop.”

Bernie Cho

A country with 50 million people and roughly 15 million unique music subscribers feels like there’s a lot of headroom for growth, but the addressable market of 16-39 year olds is only 13.4 million — meaning its subscription market is saturated.

Together, these help explain why Korean domestic streaming revenues are no bigger now than they were in 2023.

K-Pop industry veteran Bernie Cho unpacks this band-or-brand conundrum: “BTS fans are not necessarily all-in, all-around fans of K-Pop. The challenge and opportunity is akin to converting Korean fans of Tottenham Hotspur into enthusiastic fans of the entire English Premier League…sans former captain Son Heung-min”:

If ‘superfan’ was the phrase du jour of the music industry in ‘25, then perhaps ‘constraints’ needs to be in ‘26.

Even if BTS does what Demon Hunters didn’t and lifts more K-Pop boats, that still doesn’t put aside that time and money are finite resources.

One band’s gain may be another’s pain.

A note from the authors: “Since publishing this article, South Korea’s global ranking has slipped. At the Latin Rio conference [from May 18-20], it was announced that Brazil (which overtook Canada last year) has already overtaken South Korea this year to become the seventh biggest music market in the world”. They note that this “will be one of many tipping points” explored at SXSW in London on June 5 during the session, Betting Big on Brazil: How Brazilian Musical Identity Became a Global Currency.