We are pleased that MBW has taken such interest in the figures recently released on investment in British music, but we’d like to give our perspective on a few points in the coverage.

On November 5th, MBW argued that publisher investment in A&R is almost as high as that of labels, and appeared to speculate that this could justify a higher share of royalties for publishers from streaming services.

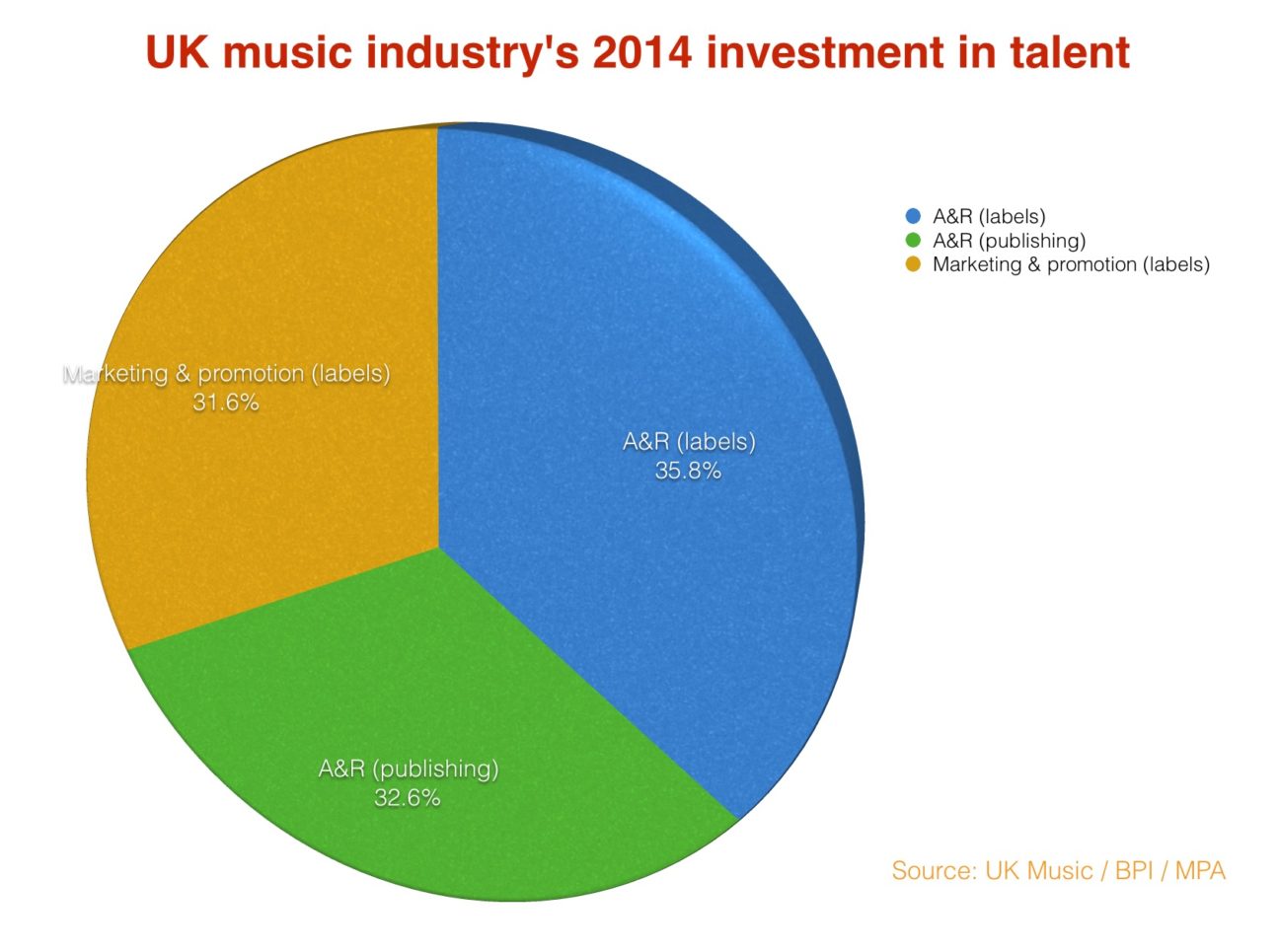

A broader comparison of label and publisher investment would reflect that total label investment of £335m (£178m on A&R and £157m on marketing) remains more than double publisher investment of £162m.

We would also add that a high percentage of label advances represent investments in new recordings by new or developing artists, where the risk of non-recoupment is very high.

By contrast, publishers’ advance figures include both high-risk payments to new writers and low risk annual pre-payments to established songwriters that are based on a songwriter’s previous royalty earnings across a range of rights.

“Total label investment remains more than double publisher investment.”

Earlier this week, MBW also analysed the 2014 A&R investment figures and drew conclusions about the majors’ 2015 hit rate.

Our figures don’t really facilitate such an analysis because the investment figures relate to the whole market while the new deals numbers are for majors only, but more importantly we don’t think it would be realistic to expect that A&R investments made in 2014 should already have produced hit records by November 2015.

Most in the business would recognise that A&R spend is a longer term investment that may take several years to produce a return, if it does at all.

Investing in new recordings is by nature a high risk business.

We think that the figures we released represent a very positive story for the UK music industry. The fact that labels and publishers are investing more in UK talent is great news for the future.

It may take more than 11 months for those investments to yield results – in the streaming era, breaking artists may take longer than used to be the case.

But we believe most in the industry will welcome the fact that our industry is confident in its future and is sowing the seeds for future success.

MBW’s Tim Ingham writes a few quick points in response:

- On the ‘record label A&R vs. publisher A&R spend’ issue, MBW didn’t speculate anything. I extracted the pure A&R numbers from a recent UK music report, and compared them like-for-like: labels at £178m last year, and publishers at £162m. Fact: they are closer figures than many would have expected. As Geoff acknowledges, the total £335m record label investment he talks about includes marketing and promotional spend – something that was separated out of MBW’s figures, but still clearly reported. This expenditure definitely shouldn’t be dismissed, least of all by lawmakers currently concocting the future formula by which rightsholders will get their slice of the digital royalty pie. It is arguably even more crucial than artist development funding in some cases. But A&R is A&R, or in a wider context ‘R&D’. The marketing spend of a car company isn’t the same as the cash it uses to facilitate the design and manufacture of its vehicle. I don’t understand why the BPI wants to pretend it is.

- As for the issues around what this A&R money is actually used for on both sides – and whether, for instance, the publishing side of the business’s A&R cash was eaten up by big catalogue renewal deals rather than risk capital on new artists – I have a simple answer: these are the numbers the BPI and MPA provided. If you want more granular analysis, provide more granular numbers. But you won’t.

- Which brings us onto the second story, about the level of breaking artists in the UK. First things first: forget the BPI numbers for a second. Just read these stats and think. Think about what they mean for music’s place in the wider entertainment ecosystem. Think about what they mean for hugely talented young artists out there who have already given up on a system that makes sticking their savings in a fruit machine look like a far better career choice. Think about the inevitable cultural paucity which will ensue from this fact: So far this year, the UK music business has broken three debut artist albums to gold. Three. That’s 100,000 sales. In a country of 64 million people. 0.16% of those people would need to buy an album to get it to gold.

- Only one of these debut albums – Virgin EMI’s James Bay – has surpassed platinum this year. One! That seems like a commercial abomination. If this trend repeats next year, something is in crisis. It might be ‘blockbuster’ A&R, it might be the album format, it might be unit sales-led metrics, it might be the public’s disinterest in new talent. But if you actually care about who’s going to be headlining your festivals in five years, the sensible thing to do isn’t to button your lip and pretend everything’s hunky dory. Because, sorry, but the act behind the UK No.1 album last week, Elvis Presley, ain’t gonna be playing Glastonbury anytime soon.

- So let’s look at the MBW numbers. The BPI said 156 new artist deals were signed last year. I argued that nine debut artist albums reached gold (100,000 sales) in the same 12 months. That’s a 5.7% ratio. Had I based the analysis on platinum sellers (300,000) in any given year of late, that percentage would have dropped to 2-3%.

- I’m not naive enough to definitively state that those exact 156 artists put out any records, let alone definitely put out albums the following year. What I’m saying is this: as a ballpark figure, the UK major labels are signing over 150 new artists each year. In a ‘good’ year, three will eventually release platinum albums. Maybe a further seven will release gold albums. Is that good enough? More crucially, is it cost-effective? No.

- So let’s talk about it. Let’s ask why Sam Smith and George Ezra and Ed Sheeran become the chosen few. Let’s ask why 94.3%, or 96.1%, or 90.2% or 89.333333% or… fewer than one out of ten new major label signings ever justify the money spent on them.

- Finally, Geoff has a fair point on the BPI’s label A&R spend figure in 2014 being misleading if you apply it only to new artists. (Which is why in the original MBW analysis I said, explicitly: “It is more difficult to derive accurate conclusions from this monetary figure, as there’s no way of knowing how much of the cash went on new artists alone – rather than re-signed deals, advances to catalogue acts etc.”)

- In reality, I’m told that majors spend an average of around £300,000 on a new artist. Here we go again: we know, thanks to the BPI, that last year the UK major labels signed 156 new artists. 5.7% of that number (not those specific artists…) released gold albums. My calculator’s slightly bored of me. You do the maths. And then ask: is the answer a healthy one?

Jane Dyball, CEO of the MPA, adds her perspective:

“These figures come out of a UK Music report based on data. It is a good news story about the level of investment in talent by labels and publishers. It is not supposed to be a competition as to quantity or quality of risk.

“As an industry our whole is better than the sum of our parts and we should always bear that in mind if we want to do the best job for our talent.”Music Business Worldwide