Chinese tech and media conglomerate Tencent Holdings, and its music subsidiary Tencent Music, have been making music-business headlines over the past few years.

From Tencent Music inking an equity swap with Spotify and touting an unconventional, tipping-driven business model, to both Sony Music and Warner Music owning stakes in Tencent Music as well, to Tencent Holdings purchasing a minority stake in Universal Music Group and being the target of an antitrust probe from the Chinese government, the global music business is now inseparable from Chinese money.

But there’s one big caveat to this whole narrative: Tencent Music and Tencent Holdings are not actually Chinese companies on paper. Instead, they’re both incorporated in the Cayman Islands — over 8,100 miles away from Beijing.

A British Overseas Territory in the Caribbean Sea with notorious ties to offshore financing and tax fraud (see the Panama Papers and Paradise Papers), the Cayman Islands also serves as the headquarters for many other tech conglomerates in China. Aside from Tencent, the likes of Alibaba, Baidu, JD.com and Sina Corporation also call the territory “home.”

Moreover, because of its offshore incorporation, Tencent Music doesn’t actually own any of the music services it operates — namely QQ Music, Kugou, Kuwo and WeSing — and, crucially, neither do its shareholders.

Instead, Tencent Music merely maintains a series of “contractual arrangements” with said music services through a legal structure known as a variable interest entity (VIE) — which gives the parent company effective operational control over the services and the ability to consolidate their financial and operational results in quarterly financial statements, but does not give Tencent Music’s shareholders any voting rights.

Moreover, many legal sources have previously claimed that due to the relative underdevelopment of securities law in the Cayman Islands, the contracts that Tencent Music holds with its services through VIE arrangements may be unenforceable — or, in legal terms, void ab initio (“to be treated as invalid from the outset”). If accurate, this would leave little to no protection for Tencent Music’s investors, which, remember, include major music-industry stakeholders. The Chinese government has yet to speak out in formal endorsement of VIEs, nor in confirmation of their enforceability.

Why is no one in the music industry talking about this, and what could it mean for their own future?

To start, it’s worth unpacking why in the world Tencent or any of its big-tech peers in China would want to incorporate in the Cayman Islands in the first place, instead of in their own country.

As revealed in part by the investigations of the Paradise Papers and the Panama Papers, the Cayman Islands is a popular offshore tax haven for both wealthy individuals and larger companies from around the world, as the territory charges no income, corporation or capital gains tax. (Two of Spotify’s board members, CEO Daniel Ek and co-founder Martin Lorentzon, have both incorporated their own holding companies — D.G.E. Holding and Rosello, respectively — in the Republic of Cyprus, another popular offshore financial center.)

As Tencent Music discusses in its F-1 filing, incorporating in China would have required the company to pay to a “standard worldwide income tax rate” of 25% as a “resident enterprise” in the People’s Republic of China, a much more expensive situation than the Cayman Islands’ tax-free environment.

“For Tencent, the issue of obfuscating ownership is especially interesting in light of recent rumors that Tencent Holdings turned to sovereign wealth funds from Singapore and other countries to help rescue its equity deal with Universal Music Group.”

Another reason a Chinese company might want to incorporate in the Cayman Islands is to obfuscate its corporate ownership structure. This motivation has precedent among Chinese elites — as the New York Times found in multiple investigations of local conglomerate HNA Group, which used offshore incorporation to help hide the extent to which top executives and their relatives controlled the company and its subsidiaries.

For Tencent, the issue of obfuscating ownership is especially interesting in light of recent rumors that Tencent Holdings turned to sovereign wealth funds from Singapore and other countries to help rescue its equity deal with Universal Music Group, after major potential funders left the negotiating table. At large, territories like the Cayman Islands are now being forced to consider public registries that show who owns all locally-registered companies.

But for most Chinese companies, the top reason to incorporate offshore is purely practical: If they want to achieve a certain level of international scale and popularity through attracting foreign investors, they almost don’t have any other choice.

According to Tencent Music’s F-1 filing, the latest version of the list prohibits foreign investors “from investing in companies engaged in certain online and culture related businesses, internet audio-visual programs businesses, internet culture businesses and radio and television program production businesses.”

Music- and audio-streaming platforms are included in this mix. This is likely why, for instance, Spotify has not yet launched in China and decided to invest in Tencent Music instead, as a way of having an upside in the local music market’s growth without dealing with the country’s political complexities directly.

“For now, the only way that a Chinese internet, telco or media company can get foreign investment is by incorporating in an offshore territory, and then establishing a VIE structure locally.”

A foreign venture-capital firm or startup accelerator can technically launch a local Chinese arm to access investments in non-prohibited sectors, as the likes of Walden Venture Capital and Lightspeed Venture Partners and Sequoia have done in the past. But for many Chinese startups, it’s actually become more lucrative — and less culturally and politically risky — to go with homegrown private firms or government-backed initiatives rather than international ones, a phenomenon that has forced the likes of Y Combinator to back out of the country in recent months.

For now, the only way that a Chinese internet, telco or media company can get foreign investment is by incorporating in an offshore territory, and then establishing a VIE structure locally.

As Serena Shi explains in a 2014 article in the Fordham Law Journal, a basic VIE structure consists of three different entities: 1) a company listed on a U.S. stock exchange and headquartered in an offshore financial center, 2) a foreign-owned entity based in China and 3) a third company with operating business in China. The U.S.-listed, offshore company owns 100% of the second China-based entity, but the latter “has only a series of contractual agreements with the [third] operating company,” writes Shi. As a result, “U.S. investors buying stock in Tencent Music are shareholders in the Cayman Islands listed company, not in the end operating company.”

This can all sound rather confusing to people who aren’t VIE experts — so, what does this look like for Tencent Music?

First, a little more background: Tencent Music (run by CEO Cussion Pang, pictured main) was formerly China Music Corporation (CMC), an independent company that owned Kuwo and Kugou and was incorporated in the Cayman Islands in 2012.

According to Tencent Music’s F-1 filing, CMC became a wholly-owned subsidiary of Tencent by issuing a 61.6% stake to a Tencent-owned subsidiary called Min River Investment Limited (which is also incorporated offshore, in the British Virgin Islands) in July 2016. Five months later, CMC merged with QQ Music, and the brands collectively changed their name to Tencent Music Entertainment.

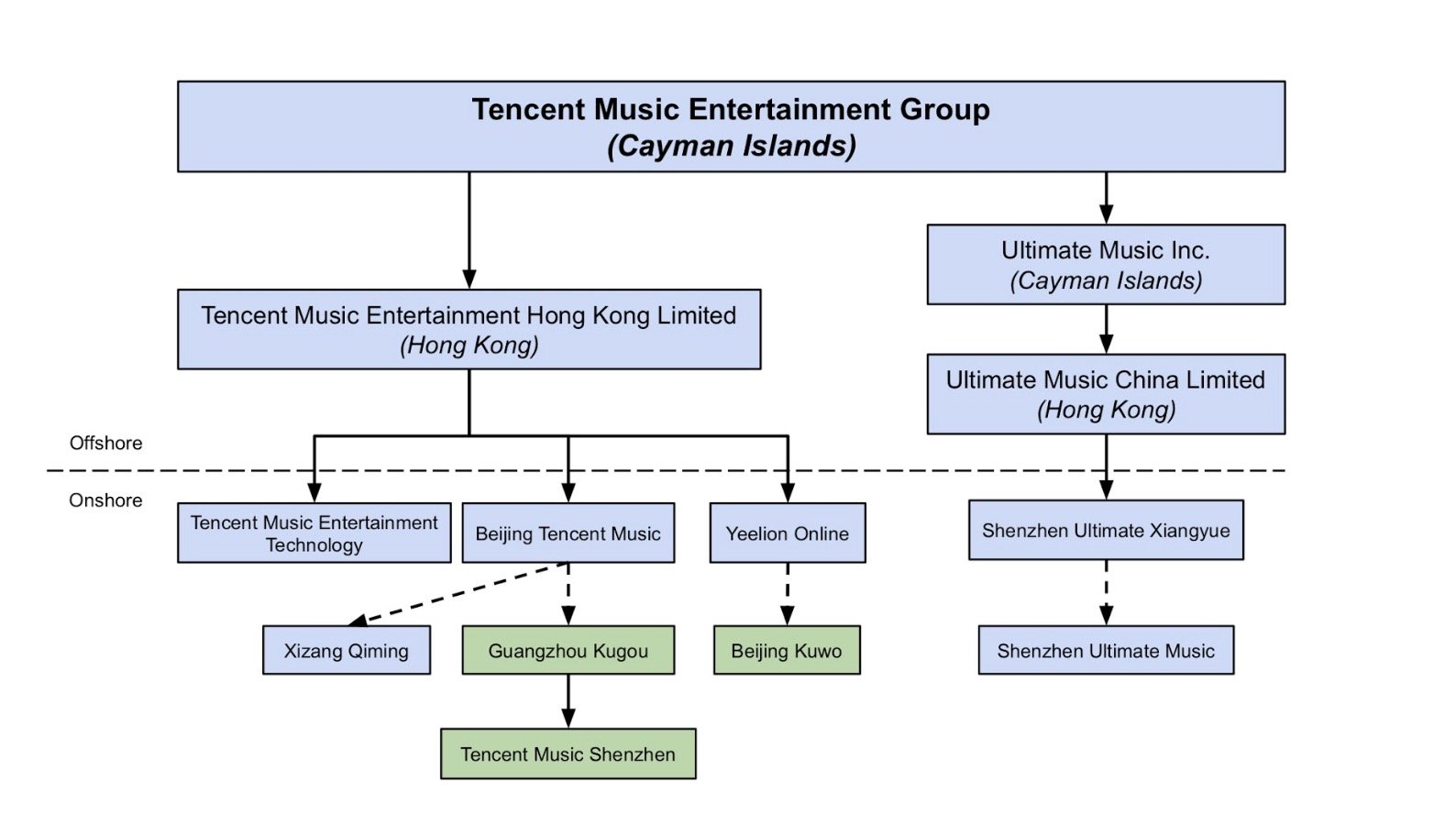

Now, let’s look at Tencent Music’s corporate structure. The below diagram is adapted from the company’s own visualization in its F-1 filing, which is much lower-quality. Solid arrows in this diagram refer to majority or full equity interest, while dotted arrows refer to contractual arrangements with VIEs:

This diagram shows, for instance, that Tencent Music doesn’t actually own any of Kuwo. Instead, it owns 100% of a local subsidiary called Yeelion Online, which in turn has a contractual arrangement with Kuwo that gives the former operational control over the latter, but not actual ownership. Similarly, the subsidiary Tencent Music Shenzhen operates QQ Music and WeSing, while Tencent Music Beijing operates Kugou, according to the F-1 filing — but none of these arrangements give Tencent Music any ownership over those services.

Crucially, this implies that shareholders in Tencent Music — including Sony Music, Warner Music and Spotify — are shareholders in the Cayman Islands shell company, not in any of its underlying services (Kuwo / Kugou / QQ Music / WeSing).

Again, this is a rather common organizational structure among larger Chinese companies; the market cap for Chinese corporations that are publicly-traded in the U.S. and utilize the VIE structure currently sits at over $1.5 trillion. As Shi writes in her paper, aside from offering access to foreign investment, the VIE structure also “proffers a shortcut to overseas investment by eliminating the need to obtain central government approval of cross-border acquisition of Chinese assets and equity” (e.g. Tencent Music doesn’t need approval from the Chinese government for every company interested in buying its stock).

But, as previously mentioned, the VIE contracts are likely void ab initio, and rest on shaky legal ground with potentially negative implications for shareholders.

In the case of Tencent Music, that means that services like QQ Music and WeSing may be earning a lot of cash, which is consolidated in Tencent Music’s financial statements, but it remains unclear whether any of that cash will actually travel back to the Cayman Islands-incorporated shell company to be able to pay off as dividends to shareholders like Warner Music, Sony Music and Spotify.

The only sense of guaranteed “return” for said shareholders is the appreciation of Tencent Music’s stock on the secondary, public market. In Shi’s words: “The investor derives economic benefits solely from the contractual agreements between the listed entity and the underlying PRC [People’s Republic of China]-domiciled business. As such, a VIE investment is only as good as the validity of its underlying contracts.”

Speaking of contracts, another downside lies in the lack of shareholder protections in the case a VIE fails — whether from a Chinese governmental decree (e.g. upon finding out that the contractual arrangements in place do not comply with national restrictions on foreign investment), from managerial conflict or from other operational problems.

For instance, if you are a U.S. investor in Tencent Music stock, “it may be difficult or impossible for you to bring an action against us … in the event that you believe that your rights have been infringed under the U.S. federal securities laws or otherwise,” reads Tencent Music’s F-1 filing. “Even if you are successful in bringing an action of this kind, the laws of the Cayman Islands and of China may render you unable to enforce a judgment against our assets or the assets of our directors and officers.”

The best-known example of investors losing control over a VIE because of unenforceable agreements took place in 2011.

That year, Alibaba’s founder and former CEO Jack Ma transferred payment subsidiary Alipay to a separate company in China under his own name, allegedly to obtain an important business permit from the Chinese government. The move had not been approved ahead of time by any of Alibaba’s investors from abroad — particularly Yahoo and SoftBank, who eventually reached a settlement with Alibaba Group that involved Alipay either giving a significant stake to Alibaba, or paying the parent company up to $6 billion.

Yahoo’s stock price dropped significantly during the dispute, which drew criticism from commentators and financial analysts in the following years. “Once it hits the fan, your rights as a BABA shareholder are virtually non-existent,” finance blog Deep Throat wrote in 2016. “There are no assets. Nobody to sue or send to jail. There’s nothing to liquidate and sell off. As a member of the wronged class of Investors you’re looking at a stack of breached contracts and untraceable money trails from empty paper/shell companies.”

More recently, when Ma relinquished control over Alibaba’s VIEs in 2018 and still didn’t give international shareholders any more control of said VIEs, short-seller Carson Block reminded Bloomberg that the general VIE structure is “rife with abuse. You have effective impunity.”

Tencent and its music subsidiary haven’t received nearly the same scrutiny yet, even though its VIE structure does theoretically make it possible for Tencent Music’s owners to, say, spin off QQ Music or WeSing into a separate company under the CEO’s ownership without investors’ permission. And there’s not much the company will say on the matter, at least officially. When I reached out to Tencent Music for comment, a rep provided only the following statement: “Like all other major Chinese companies listed overseas with a VIE structure, information relating to TME’s VIE structure and its legal risks has been fully disclosed in TME’s SEC filings.”

As Tencent becomes increasingly influential on the global music stage, I think major industry players should start taking those legal risks more seriously — not by terminating their relationships or investments entirely, but rather by asking simply what they really do, and do not, own in the Chinese music-streaming landscape.Music Business Worldwide