David Ellison has his New Paramount. Now Bill Ackman wants his New UMG.

That’s not just a turn of phrase.

‘New UMG’ is what Ackman literally calls his proposed restructured Universal Music Group – apparently taking a page from Ellison‘s playbook. (When Skydance completed its takeover of Paramount last year, it dubbed the combined company ‘New Paramount’ during the deal process.)

Ackman‘s proposal to acquire Universal Music Group landed with the music company’s board this morning (April 7). Whether it goes anywhere is another matter.

The Pershing Square proposal is non-binding, UMG‘s board hasn’t approved it, and the path to closing — requiring a two-thirds shareholder vote, regulatory sign-off, and a new employment deal for Sir Lucian Grainge — is a long one.

But the more immediate question may be what Ackman‘s move does to the market for UMG itself.

Could it invite competing proposals? Bolloré Group, sitting on an 18% stake in UMG, has its own calculations to make. Might the likes of Blackstone or Apollo — who have themselves committed billions to music assets in recent years — also now see a window?

Few in the music biz will dispute Ackman’s central logic when he says that “UMG’s stock price has languished due to a combination of issues that are unrelated to the performance of its music business”.

UMG‘s share price has fallen by 30%+ over the past year. Ahead of today’s news, that valued Universal at approximately EUR €31 billion (USD $36 billion) — roughly 11 times its 2025 adjusted EBITDA.

Premium music catalog assets regularly change hands at high-teens to 20-plus times EBITDA multiples on the private market.

The world’s largest music company, Ackman argues, is not currently being valued like one – and he has a point.

MBW covered the headline terms of Ackman‘s takeover proposal here – but a more in-depth letter from Pershing Square to UMG‘s board of directors reveals some important additional details.

Here are three of them…

1. This deal would finally trigger the sale of UMG’s $3B+ Spotify stake — and artists would get up to €750 million ($866 million).

UMG first acquired equity in Spotify at the streaming platform’s launch in 2008. In the years since, as Spotify has grown into a company worth tens of billions of dollars, UMG has held onto every share.

That changes under Ackman‘s proposal.

The Pershing Square letter confirms that €1.5 billion ($1.7 billion) in net proceeds from the monetization of UMG‘s €2.7 billion ($3.1 billion) Spotify stake — “after taxes and net of the artists’ share of Spotify proceeds” — will be used to fund the cash consideration of the bid. The stake will be “sold in the market or in a block transaction.”

For UMG‘s artists, the implications are direct. The letter states that “artists will also benefit from the Transaction by receiving up to €750 million ($866 million) in proceeds from the sale of Spotify shares.”

That commitment has a history.

In 2018, as part of a new deal with Taylor Swift, UMG confirmed it would distribute any Spotify sale proceeds to artists on a non-recoupable basis — meaning artists would receive their share regardless of any outstanding unrecouped advances.

Swift wrote on Instagram at the time that she had asked UMG to ensure “any sale of their Spotify shares result in a distribution of money to their artists, non-recoupable.”

The major agreed.

2. Ackman wants Michael Ovitz as UMG’s Chairman of the Board — citing a 40-year relationship with Sir Lucian Grainge.

Under Ackman‘s proposal, UMG‘s board “will be refreshed to include Michael Ovitz as Chairman and two representatives from Pershing Square in addition to members from the current UMG board”.

As such, Ovitz would presumably succeed Sherry Lansing, the current Chair of UMG’s board.

Ovitz co-founded Creative Artists Agency in 1975 and served as its Chairman until 1995, building the agency into what Pershing Square describes as the world’s leading talent agency. He subsequently served as President of The Walt Disney Company from 1995 to 1997.

Ackman notes that Ovitz “has a 40-year relationship with Sir Lucian Grainge“, and describes Ovitz as “one of the most recognized global entertainment executives, having represented many of the most important and iconic music, film, and entertainment acts in the world.”

“Since UMG’s listing, Sir Lucian Grainge and the company’s management have done an excellent job nurturing and continuing to build a world-class artist roster and generating strong business performance,” added Ackman today – a telling personal compliment for UMG’s long-term boss.

Ovitz is currently a director of Pershing Square SPARC Holdings, Ltd., the acquisition vehicle through which the transaction would be structured.

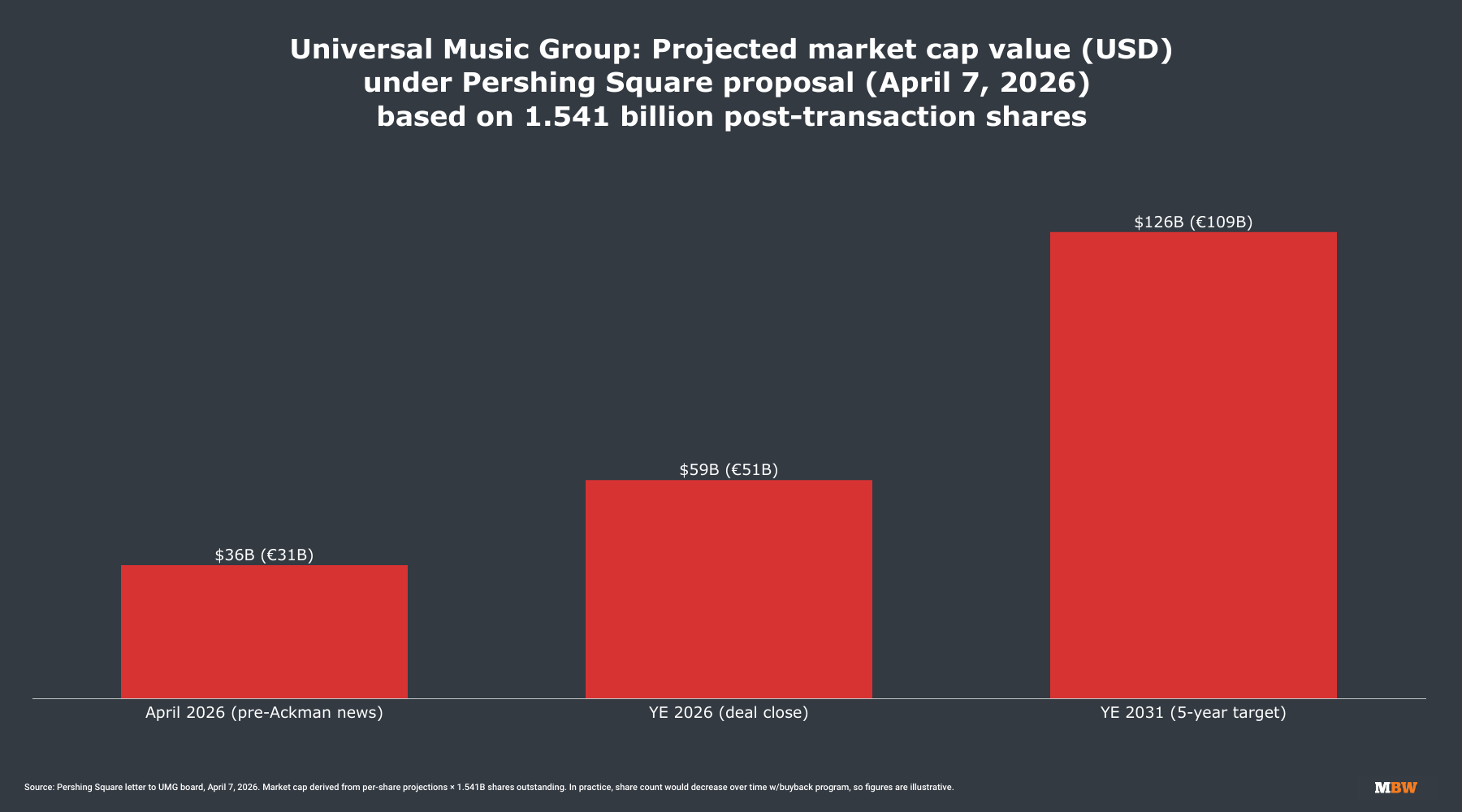

3. ‘New UMG’ could be worth over USD $100 billion by 2031. It was valued at $36 billion last week.

The Pershing Square board letter includes a detailed five-year valuation model for UMG — and the headline numbers are striking

UMG carried a market cap of approximately EUR €31 billion (USD $36 billion) before today’s news, reflecting a share price that has fallen by around a third over the past year.

Ackman argues this public valuation is deeply wrong — and that the structural issues his proposal is designed to fix are all that stand between UMG and a significant re-rating by investors.

By year-end 2026 — roughly when Ackman expects his deal could close — Pershing Square projects ‘New UMG’s’ share price could reach EUR €32.90, a 92% premium vs. UMG’s April 2nd closing price of €17.11.

Based on the 1.541 billion shares that ‘New UMG’ would have outstanding post-transaction, this implies a market cap of approximately €51 billion ($58.5 billion) by the end of this year.

Continuing the logic, Ackman projects that ‘New UMG’s’ share price could reach EUR €71 by year-end 2031 – more than four times its share price last week.

Applied to the same post-transaction share count, that implies a market cap of approximately €109 billion ($126 billion) by 2031.

(In practice, the share count would shrink thanks to the buyback program at the heart of Ackman’s proposal, meaning the actual 2031 market cap would be lower, but the per-share value for remaining investors would be higher. My market cap figures here are illustrative.

In Ackman’s mind, UMG’s growing earnings could combine with a NYSE listing that would attract a new pool of institutional investors currently unable to buy a European-listed stock.

Central to Ackman’s projection is a new approach to capital.

Rather than paying out 50% of net income as dividends — UMG‘s current policy — ‘New UMG’ would redirect surplus free cash flow toward buying back its own shares, a strategy that typically drives a company’s value higher over time.

Pershing Square estimates New UMG will generate approximately €15 billion ($17.3 billion) in total cash over the next five years available for acquisitions and buybacks – roughly half the company’s entire market cap today.

Music Business Worldwide