The MBW Review offers our take on some of the music biz’s biggest recent goings-on. This time, we take the microscope to Universal Music Group‘s latest Q1 results, which were up by double digits year-on-year. The MBW Review is supported by Instrumental.

It’s no secret that Universal Music Group is commercially smashing it right now.

The company’s latest Q1 results, announced by parent Vivendi last month, showed that its recorded music revenues were up 19.2% year-on-year, with streaming specifically up 28.1%. UMG’s overall revenues – including publishing, recorded music and other income – grew 18.8%.

Universal’s biggest rival in recorded music rights, Sony Music Entertainment, saw smaller streaming growth of 8.2% in the quarter versus the prior year, while overall label revenues dipped 6.5%, primarily owing to the company’s transition away from physical formats (of which sales fell 36.8%).

All of this will be music to the ears of Vivendi, of course, as the company looks to sell up to 50% of UMG (or, possibly, even more), for a princely sum.

There is, however, one question which analysts probing that deal might wish to look at more closely – something which the global music industry itself may also be wise to ponder.

We are often told that music streaming has made the recorded music industry more global than ever, ‘switching on’ potentially huge markets such as Brazil and China after they were dominated by piracy for decades. This maxim, to a degree, is undoubtedly true: both Brazil and China, in addition to South Korea, featured in the IFPI‘s Top 10 commercial recorded music markets in 2018.

Yet it is often therefore additionally assumed that the relative proportional power of the United States, traditionally the world’s No.1 recorded music market, will have been reducing, as other corners of the earth begin to prosper to a greater degree.

MBW has crunched the numbers and found that, actually – both at Universal Music Group and in the wider global recorded music industry – the opposite is true. In fact, since the birth of streaming, the United States has consistently become a more commercially important, and therefore powerful, global player.

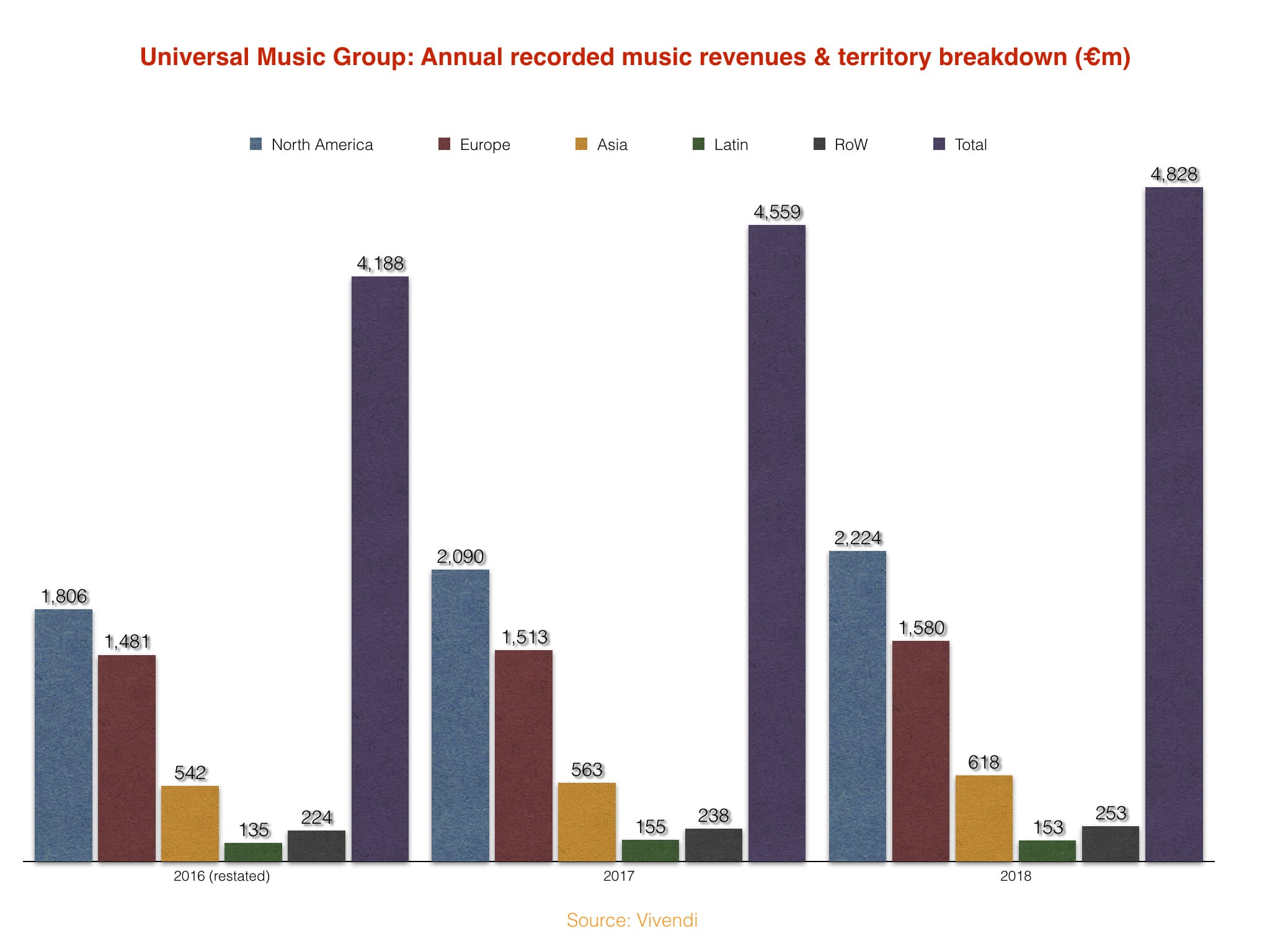

Let’s tackle Universal first. The firm’s total recorded music revenues last year stood at €4.83bn, up 9.8% year-on-year (Paris-based Vivendi reports in Euros).

2018 was a dominant year for Universal in the United States, as it claimed eight of the Top 10 bestselling artists across all formats, led by the likes of Drake and Post Malone.

It’s therefore no great surprise that, according to Vivendi’s data – which breaks down UMG’s revenues on a territorial basis – Universal grew its annual revenues in North America by 9% in the year, to €2.22bn.

What is perhaps more surprising: those North American revenues made up 46.1% of Universal’s overall global sales in 2018 – the biggest annual percentage claimed by that market in recent history.

What’s more, of the €269m growth achieved by Universal across the world last year, its growth in North America contributed the majority (€184m = 68.4% of UMG’s global annual growth).

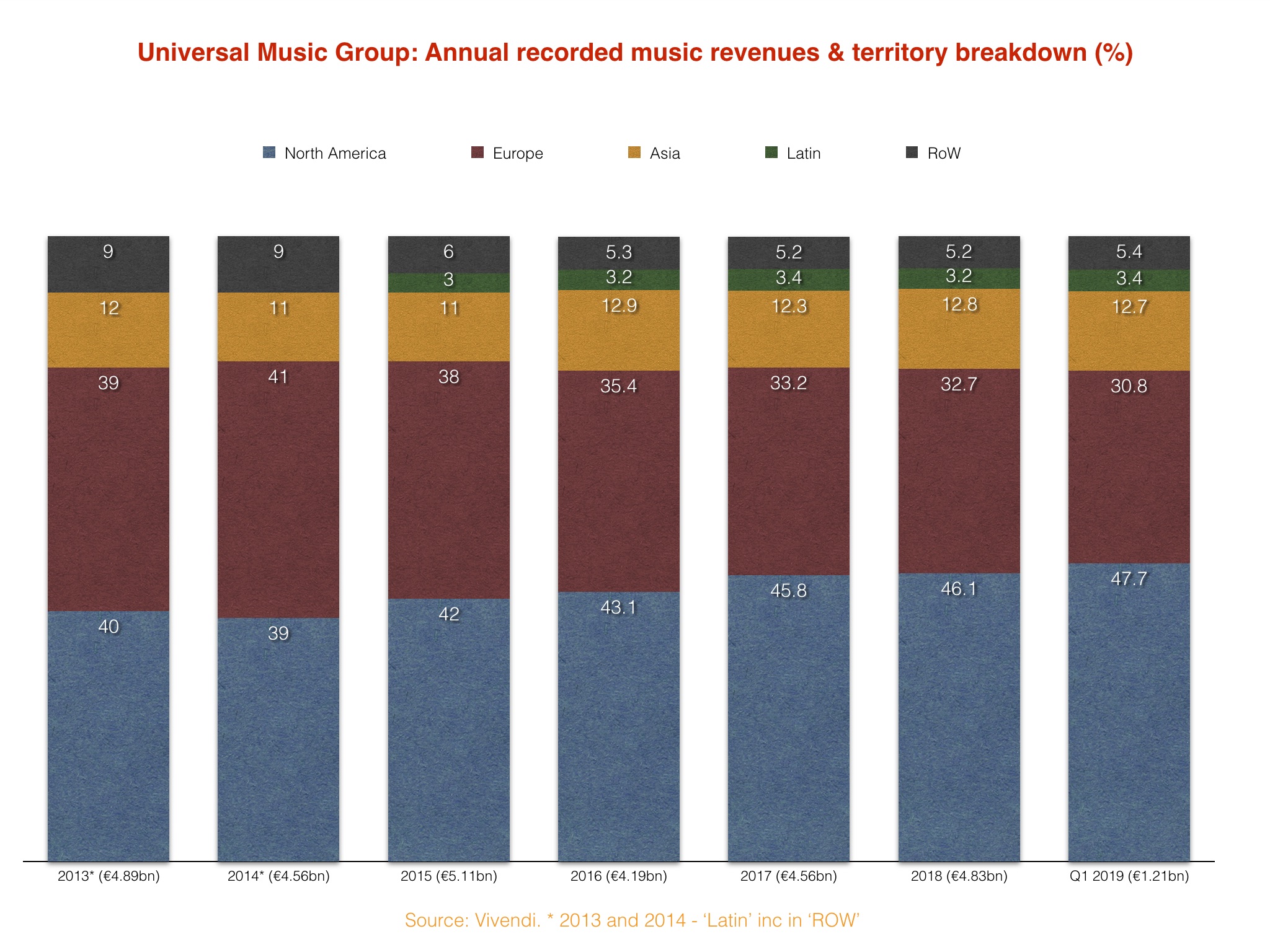

This trend has been consistent in recent times, as demonstrated by the percentage breakdown of UMG’s annual revenues by territory over the past few years.

According to MBW calculations based on Vivendi data, since 2013, North America’s share of Universal’s yearly recorded music revenues has grown by 6.1%.

That growth appears to have come entirely come at the expense of Europe, which claimed 41% of UMG’s total recorded music revenues in 2014 – but just 32.7% (-6.3%) in 2018.

As for ‘globalization’? In truth, UMG revenues from Asia (+0.8% in 2018 vs. 2013) and Latin America (+0.2% in 2018 vs. 2015) simply haven’t moved Universal’s financial needle anywhere near as much as the USA.

(A quick note on the below graph: Vivendi didn’t start breaking down revenues into ‘Latin America’ until 2015, and prior to 2016, it only presented whole number percentages for its territorial breakdown.)

The hope for Vivendi in the future years, no doubt, is that as the likes of China, India and Brazil continue to grow financially, the contribution made by non-North American markets to UMG’s annual sales will materially expand.

Yet even in Q1 this year, the trend continued: North America claimed 47.7% of UMG’s €1.2bn recorded music revenues in the quarter, with Europe on 30.8%. The rest of the world combined claimed 21.5%.

(UMG’s biggest-selling artist in the quarter was North American, too – Ariana Grande, pictured.)

Although Universal’s recent dominance of the USA’s blockbuster charts makes this trend more pronounced, the company is not alone.

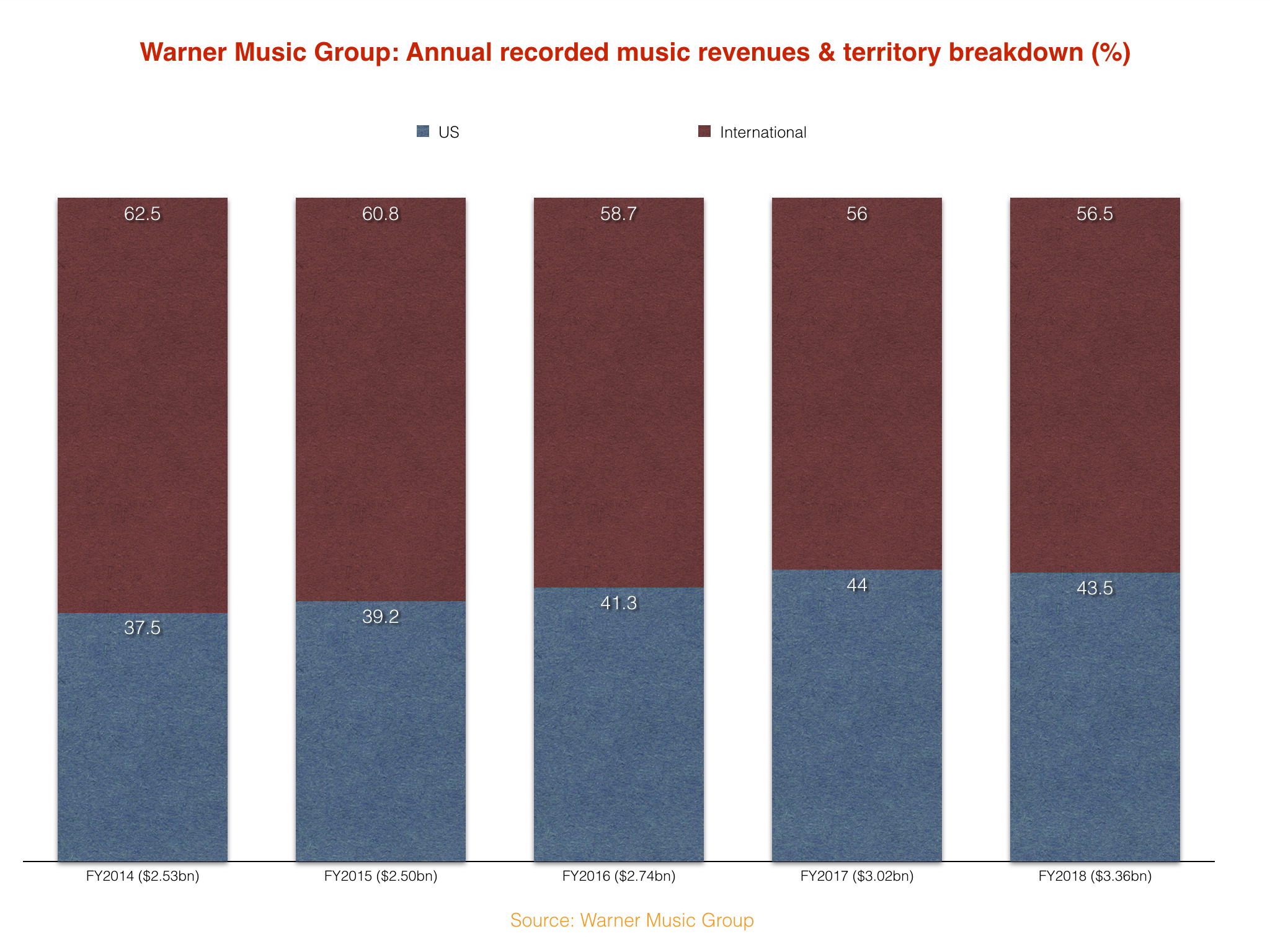

Warner Music Group breaks down its recorded music revenues into those which come from the USA and those which are derived from all other nations (‘International’).

As you can see below, in Warner’s financial year (to end of September in each case), the USA’s contribution to its revenues increased its percentage of the pie annually from 2014 to 2017.

However, last year (FY2018), WMG’s international performance tipped the balance, claiming 0.5% more of worldwide revenues than it did in the prior 12 months.

Time will tell if this is an anomaly, or an indication that the US will continue to lose share within WMG’s global revenue mix in the years ahead.

All of this is happening against a backdrop of the United States becoming increasingly powerful in the global recorded music market more generally.

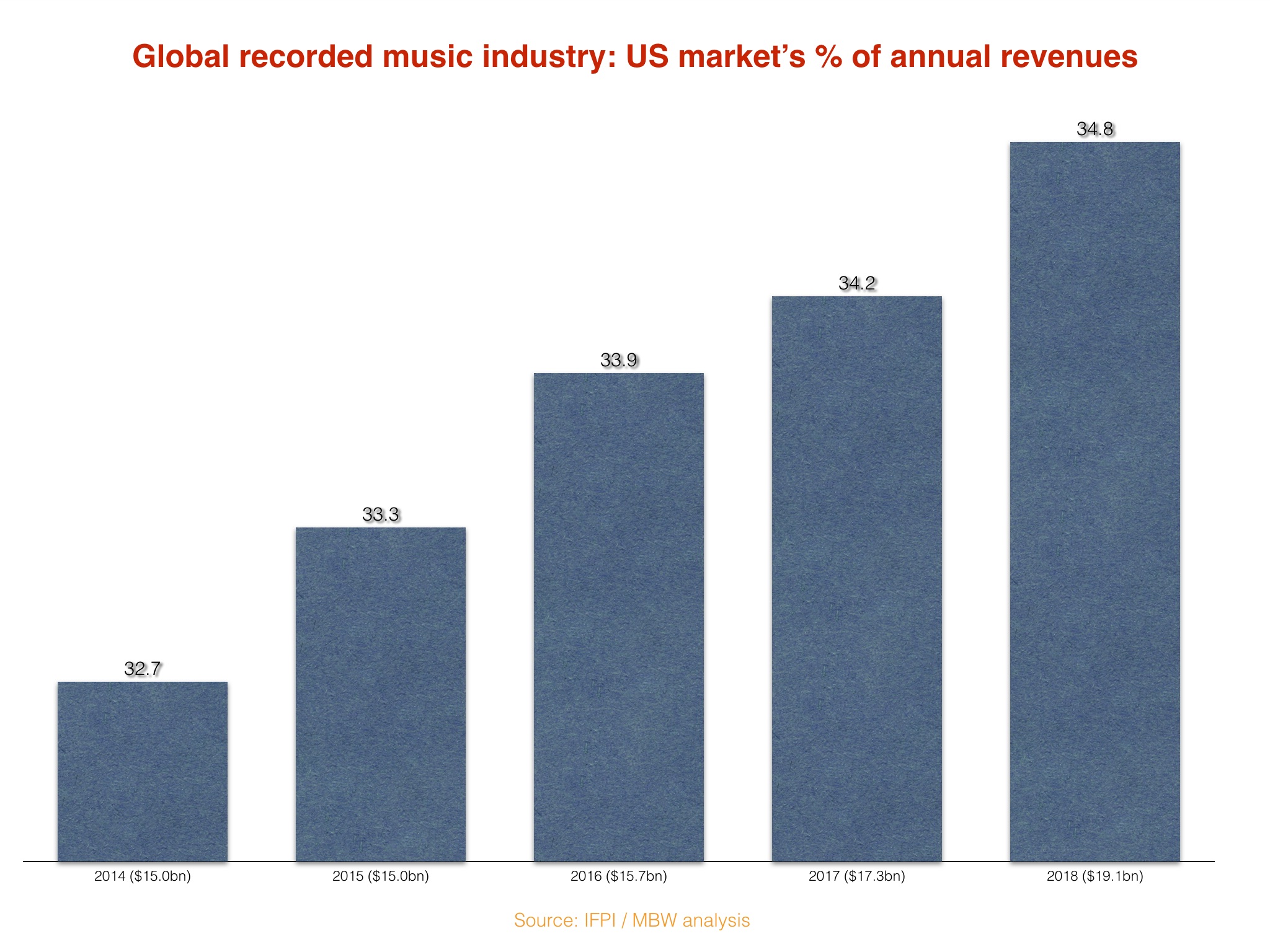

According to IFPI data crunched by MBW, the USA’s percentage of annual global recorded music revenues (from all formats) has continued to ramp up year-over-year since 2013.

Last year (2018), the US market contributed $6.64bn of a $19.1bn total worldwide market, says IFPI, which amounted to 34.8% of the overall pie – up over 2% on the same figure from 2014.

The USA’s growing market share has likely been boosted by Japan, whose own portion of the global recorded music market fell from 17.6% in 2014 to 15% last year.

There are also signs of the US’s dominance beginning to fall in streaming revenue terms: although the USA’s percentage of total streaming revenues grew significantly in 2017 (up to 42% from 39% in the prior year), it dipped slightly in 2018 to 41.4%, according to IFPI. (IFPI did not breakout specific streaming % figures until 2016.)

Yet, as experts predict a slowdown in streaming subscription growth in the USA over the next year and beyond, one thing is clear: the global recorded music industry, and its biggest companies, might have increasingly relied on North America in the first decade of the Spotify era – but it’s a strategy with an impending expiry date slapped all over it.