Welcome to the latest episode of Talking Trends from Music Business Worldwide (MBW) – where we go deep behind the headlines of news stories affecting the entertainment industry. Talking Trends is supported by Voly Music.

We expected streaming subscription growth to slow in 2022 – but not this much.

That’s the key takeaway from MBW’s analysis of stats released by the Entertainment Retailers’ Association in the UK yesterday (January 10), and discussed by MBW founder Tim Ingham on the latest Talking Trends podcast (listen above).

As Ingham explains on the Talking Trends podcast, annual growth in the money spent on subscription streaming services in the UK last year was less than half the size it was in 2021… and less than a third of the size it was in 2018.

Such numbers highlight the urgency for major rightsholders, suggests Ingham, of Spotify in particular raising its prices in key markets.

You can read an abridged transcript of this episode of MBW’s Talking Trends below, and/or listen through here:

![]()

The data I specifically want to focus on today has just been published by the UK’s Entertainment Retailers’ Association, which both monitors the commercial entertainment market in Britain, and represents companies like Spotify, YouTube, Deezer and Amazon.

Each year, the Entertainment Retailers’ Association, or ERA for short, releases stats showing how much money consumers paid annually for various formats of recorded music in the UK – including subscription streaming.

“Music biz trends in Britain are a fairly reliable bellwether for what’s coming to the States in the next year or two.”

Before I get on to the numbers themselves, a bit of important context about the UK, and why it’s such an illuminating music streaming market in the modern era.

The UK has had paid-for streaming available for around a decade and a half now, with Spotify launching in Britain in 2008. That’s particularly significant for US listeners because that 2008 UK launch was three years before Spotify eventually hit the US in 2011.

In other words, the UK is an even more mature music streaming market than the United States. But with many cultural and commercial similarities between the US and UK, emergent trends in Britain are a fairly reliable bellwether for what’s coming to the States in the next year or two.

The second important thing to know about the UK is that according to IFPI statistics, Britain is both the third biggest recorded music market in the world in terms of trade value, and it’s also the second biggest recorded music market in the world if we’re just talking about streaming dollars.

In nutshell: The UK is a market that indicates the trends that are about to hit the US, and it’s also a mature streaming market that can be considered a global commercial heavyweight in its own right.

So let’s dig into these numbers.

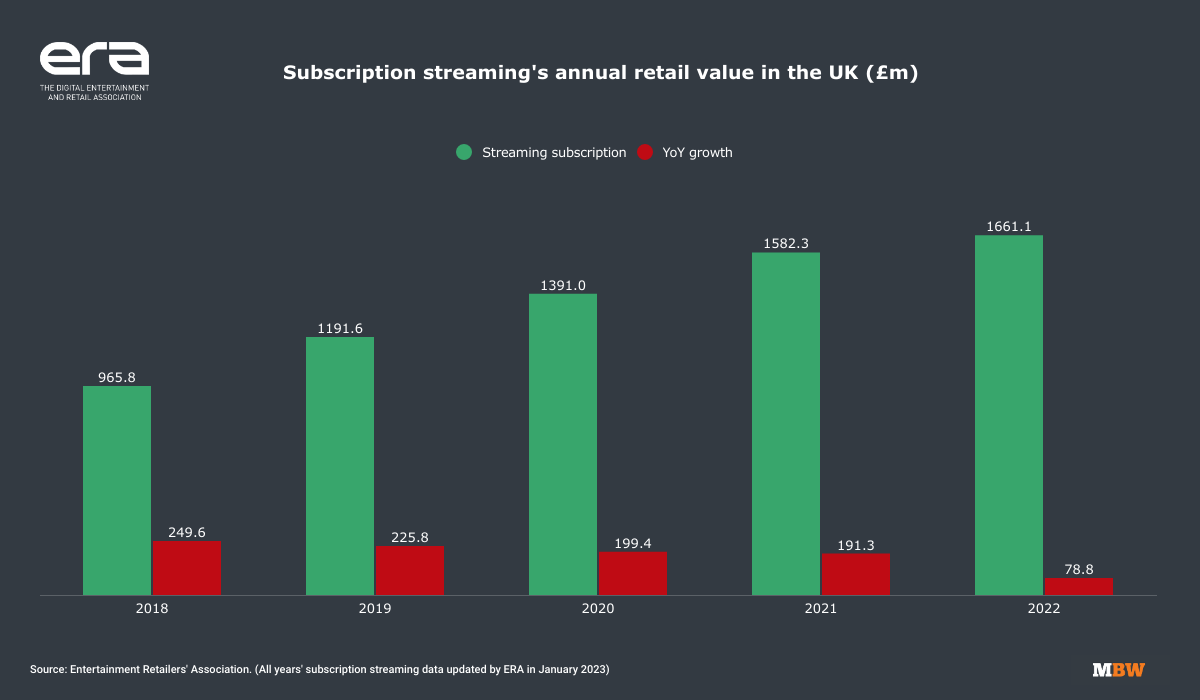

According to ERA, in the UK across the course of last year, the amount spent on music streaming subscriptions hit £1.661 billion British pounds (see below). And the amount spent on recorded music overall by UK consumers – across streaming, physical formats and downloads – was just shy of £2 billion.

For the purposes of this podcast we don’t need to pay those numbers much mind. Instead, what’s really important here is the ominous lack of growth in the UK streaming market in 2022.

According to Music Business Worldwide’s calculations based on updated stats that ERA has verified, the amount of money spent by UK consumers on music streaming subscriptions in 2022 grew by just 5.0% – or around £79 million – year-on-year.

In the prior year, 2021, according to ERA’s stats, the equivalent year-on-year growth stood at £191.3 million – close to quarter of a billion US dollars.

“In simple terms, the year-on-year growth in music subscription streaming spending in the UK in 2021 was more than double the size it was in 2022.”

To couch that in simpler terms, the year-on-year growth in music subscription streaming spending in the UK in 2021 was more than double the size of that we saw in 2022.

The annual growth in 2022 was also less than half the size of the growth we saw in both 2020 and 2019, and was less than a third of the size of annual growth we saw in 2018.

I’ll put a chart up on Music Business Worldwide alongside this podcast (see below) so you can see this dramatic slowdown in growth for yourself.

But you don’t a visual aid to know: This is hardly good news for music rightsholders.

What makes matters worse for the UK market’s figures is inflation.

According to the Bank of England / CPI, the annual inflation rate on consumer goods in the 12 months to November 2022 stood at 10.7%. (We’re waiting on figures for the full calendar year.)

If we apply that 10.7% inflation uplift to the total amount spent by consumers on music streaming subscriptions in 2021, we can work out what those same consumers would have had to spend in 2022 for the market to have stood still, in real economic terms (when you factor in inflation).

“when you factor in inflation, the value of the annual UK music subscription streaming market actually shrunk last year.”

The upshot there: To have kept pace with inflation versus 2021, the UK music streaming market would have had to generate £1.75 billion in 2022. It didn’t. It generated about £100 million less than that (£1.66 billion).

In other words, when you factor in inflation, the value of the annual UK music subscription streaming market actually shrunk last year.

The major music rightsholders obviously won’t be in love with these stats. Let’s not forget that two of them, Universal Music Group and Warner Music Group, are now both publicly traded, with investors looking for significant growth each year that ticks by.

Indeed, Bill Ackman – who runs Universal Music Group’s minority owner Pershing Square – has said he’s looking for at least 10% revenue growth from Universal each year over the next decade.

So where is that kind of growth going to come from? Especially when statistics in a market as important as the UK suggest it’s now nearing so-called ‘peak streaming’ – i.e. it’s running out of new customers willing to pay £9.99 a month, or whatever deal they get through their telco, on a music subscription service.

Well, one answer is obvious: The time has surely come for significant music streaming price rises across the board in the UK and US markets.

To a degree that’s already happening: Apple Music has recently upped its individual standard subscription price in the US and UK from $9.99 / £9.99 to $10.99 or £10.99.

We’ve also seen YouTube in the past few months raise its YouTube Premium Family Plan up from $17.99 per month to $22.99 in the US and up £17.99 per month to £19.99 in the UK.

Spotify raised its Premium Family and Duo prices in the UK two years ago, but has so far resisted making any more changes to the standard £9.99 per month price for its flagship Premium individual tariff.

That monthly £9.99 price has been in place, unchanged, despite inflation, since 2008 – 15 years ago!

You don’t need to be an economics whiz to realize that even if Spotify now raises its price by 10% – from £9.99 to £10.99 – and UK inflation was above 10% last year, Spotify’s price rise will fail to keep pace with inflation baked in from 2022 alone.

Why am I particularly picking on Spotify?

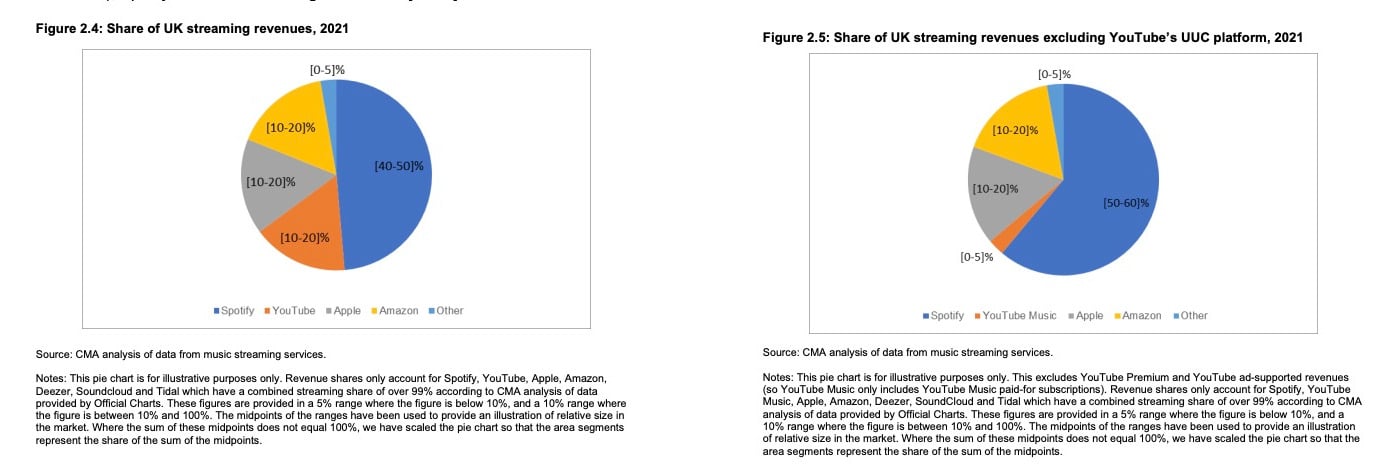

For one thing, according to a thorough report on the UK music market from the Competition and Markets Authority last year, Spotify is responsible for a 40-50% share of all streaming revenues in the United Kingdom; when you remove YouTube’s user-generated videos from that equation, Spotify’s market share of revenue moves up to between 50%-60% in the UK.

At the same time, last year, we know that due to macroeconomic factors, there was a material slowdown in the growth of ad-supported streaming revenues – heaping further pressure on the need for labels to see growth in the amount of dollars/pounds spent on subscription music streaming services.

The past few years have seen the music rights industry enjoy benefit hugely from something of a streaming music growth fairytale.

If it wants to enjoy another chapter in that fairytale, it’s going to need to see price rises from the likes of Spotify in 2023 – and fast.

MBW’s podcasts are supported by Voly Entertainment. Voly’s platform enables music industry professionals from all sectors to manage a tour’s budgets, forecasts, track expenses, approve invoices and make payments 24/7, 365 days a year. For more information and to sign up to a free trial of the platform, visit VolyEntertainment.com.