Welcome to the latest episode of Talking Trends from Music Business Worldwide (MBW) – where we go deep behind the headlines of news stories affecting the entertainment industry. Talking Trends is supported by Voly Music.

In this episode, MBW founder Tim Ingham discusses the recent quarterly results of music industry giants such as Universal Music Group, Sony Corp, Warner Music Group, and Believe.

Ingham notes that Q2 2022 saw something of a consistent slowdown in streaming revenue growth for the ‘Big Three’ major record companies.

With macro-advertising spend now set to soften online in the months ahead, Ingham suggests that we now may be moving into a new era for the majors when it comes to streaming growth.

Says Ingham: “It looks to me like we’re seeing the first signs of a new chapter for the recorded music industry: single-digit recorded music streaming revenue rises, following years of double-digit growth across the board.”

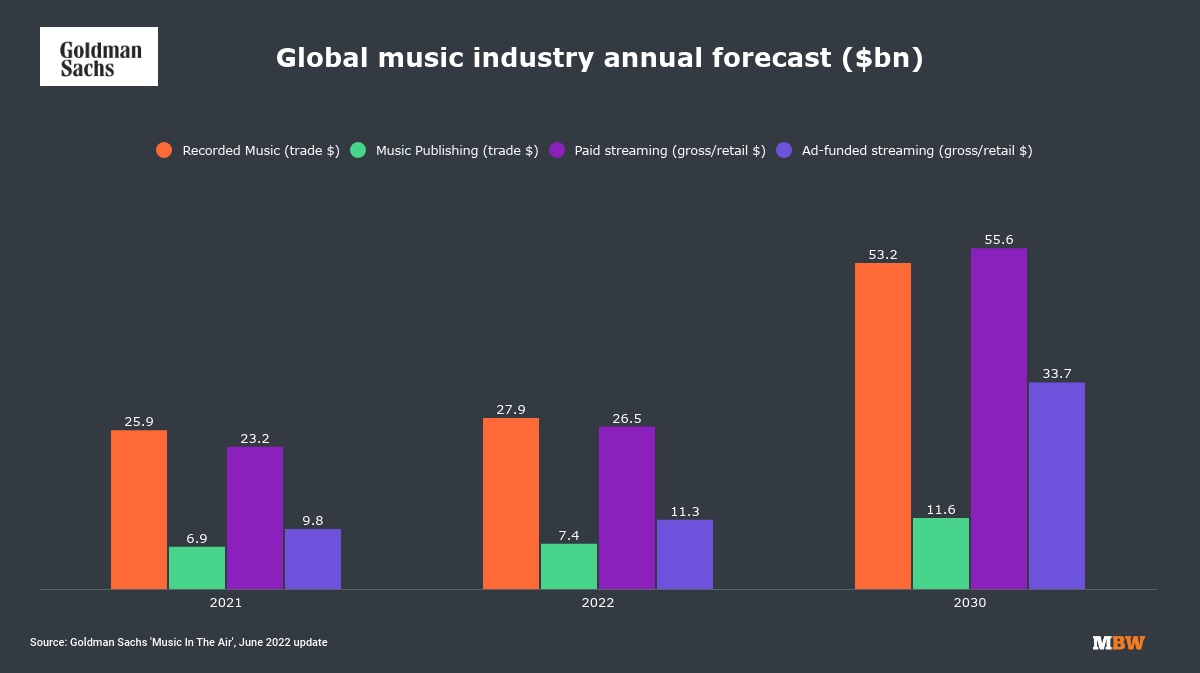

You can read an abridged transcript of this episode of MBW’s Talking Trends, complete with illustrative charts, below.

There’s been a mixed bag of news for the wider music industry in the past month. It’s gotten me thinking that the second half of 2022 is going to represent a new era of decelerated growth for the music industry.

I should clarify upfront that when I say ‘the music industry’, I’m referring to the music rights industry – the live music industry currently, and I’ll say it quietly, is looking nigh-on recession-proof.

You might have seen MBW’s Stat Of The Week the other week that was from Live Nation’s Q2 results: the company sold more tickets in the first half of 2022 than it sold in the whole of 2019.

Live Nation is now stating that, partly due to pent-up demand post-Covid, 2022 will be “the biggest year in live music history”.

Over in the recorded music industry, however, things aren’t looking quite so record-breaking.

To foreshadow the numbers on that, I turn to Goldman Sachs’ latest Music In The Air report – something of a bible for those following the trends of the commercial music business.

That report, released in June, suggested that on a gross basis, global music subscription streaming would be up 14% YoY to $26.5 billion in 2022.

It also predicted that ad-funded streaming revenues, again on a gross basis, would be up 15% YoY to $11.3 billion in 2022.

Yet looking at the latest set of music results for large-scale music companies in Q2, however, perhaps leads us to a less bullish forecast.

I should clarify at this point that, again, Goldman’s numbers are on a gross basis – they’re looking at what the streaming services are going to turn over in revenue, not what they eventually pay out to record companies.

But still, listen to this: In Q2 2022, each of Universal Music Group, Sony’s music division, and Warner Music Group, saw single-digit revenue growth in streaming year-on-year:

- Universal was up 7.0% year-on-year in terms of subscription streaming revenue in the quarter;

- Sony was up 7.9% year-on-year in terms of overall music streaming revenue in the quarter;

- Warner was up 2.7% year-on-year again in terms of overall music streaming revenue in the quarter.

All of those percentage rises are at constant currency.

Now, there are some little caveats in there, not least a one-time “catch up” payment that was delivered to both Warner and Universal by a streaming service in calendar Q2 2021.

Without that one-time, for example, Universal says that its subscription streaming revenues in calendar Q2 2022 would actually have been up by 12.1% year-on-year.

Regardless, it looks to me like we’re seeing the first signs of a new chapter for the recorded music industry: single-digit recorded music streaming revenue rises, following years of double-digit growth across the board.

Compounding this slowdown is the wider trend in digital advertising.

In Q2, Meta, the parent of Facebook, delivered total revenue of $28.8 billion down 1% YoY; and Alphabet, parent of Google, saw quarterly YouTube advertising grow by just 4.8% YoY, to $7.3 billion.

We’re more used to seeing year-on-year growth from YouTube ads in the 20-percents.

These slowdowns in macro advertising spend are being driven by – what else – wider economic difficulties, from inflation to rising interest rates, and a general feeling that businesses will be more conservative with their cash in the second half of this year than they have been in a long while.

That, inevitably, will have a knock-on effect on the music industry.

We’re already seeing it show up in music’s numbers:

- Warner Music Group just told its investors it witnessed a “market-related slowdown in ad-supported revenue” in Q2;

- Believe, the French company that works with independent artists and labels, has upped its overall forecast for FY 2022. It remains bullish on subscription streaming. However, it’s also warned investors of a softer macro advertising market in the second half of this year.

According to the IFPI, advertising on streaming services and social media generated just under $5 billion for the global record industry in 2021. That was just under a fifth of the $25.9 billion generated by the industry in total.

As I said at the start, growth is still growth.

The crucial year-on-year numbers are still all likely to be pointing in the right direction for the record industry come the end of 2022.

But those same year-on-year numbers are also likely to be smaller than the ones we’ve gotten used to seeing over the past decade.