Peloton paid the record industry more than TikTok last year, says Goldman Sachs (and 3 more revelations from financial giant’s latest ‘Music In The Air’ paper)

MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. Only MBW+ subscribers have unlimited access to these articles.

Goldman Sachs‘ annual Music In The Air report is arguably the most influential paper on the music business from a financial giant’s perspective.

The theme of this year’s update, published late last month? That might be summed up as “still sunny”.

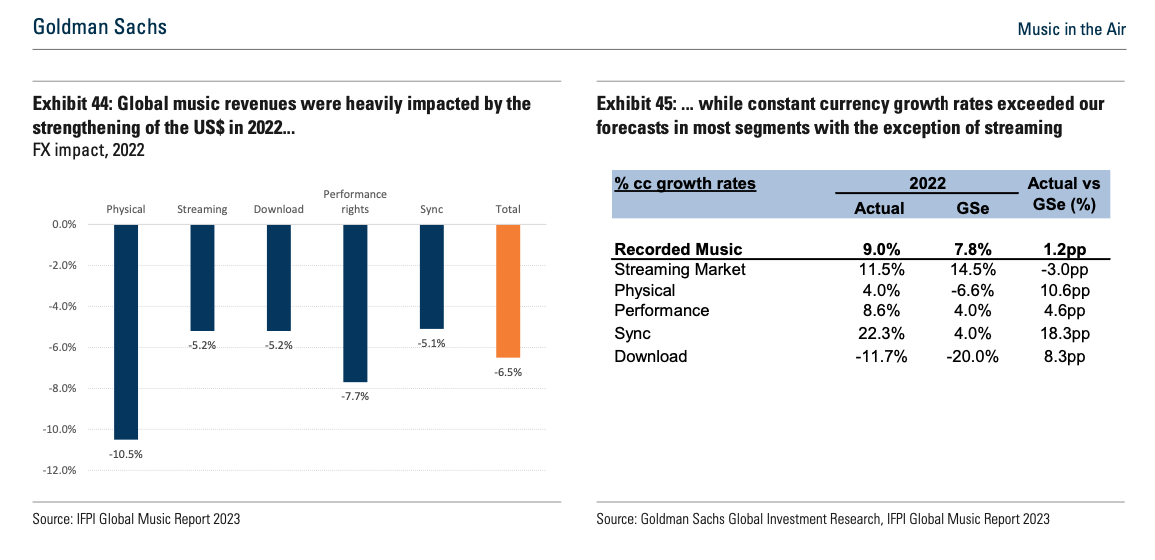

Goldman’s forecasts in its June 2023 paper regarding the future prosperity of the music rights business are significantly downgraded versus their June 2022 equivalent – but this is mostly due to currency alterations made in the latest edition of the IFPI‘s seminal annual Global Music Report.

(As previously explained by MBW, Goldman’s recorded music industry forecasts use the latest IFPI global numbers as their ‘root’. IFPI publishes its annual numbers in USD, so in a year, like 2022, where a strong dollar pulls down USD-converted sums from international territories, Goldman must then adjust its own USD figures to be in line with IFPI’s.)

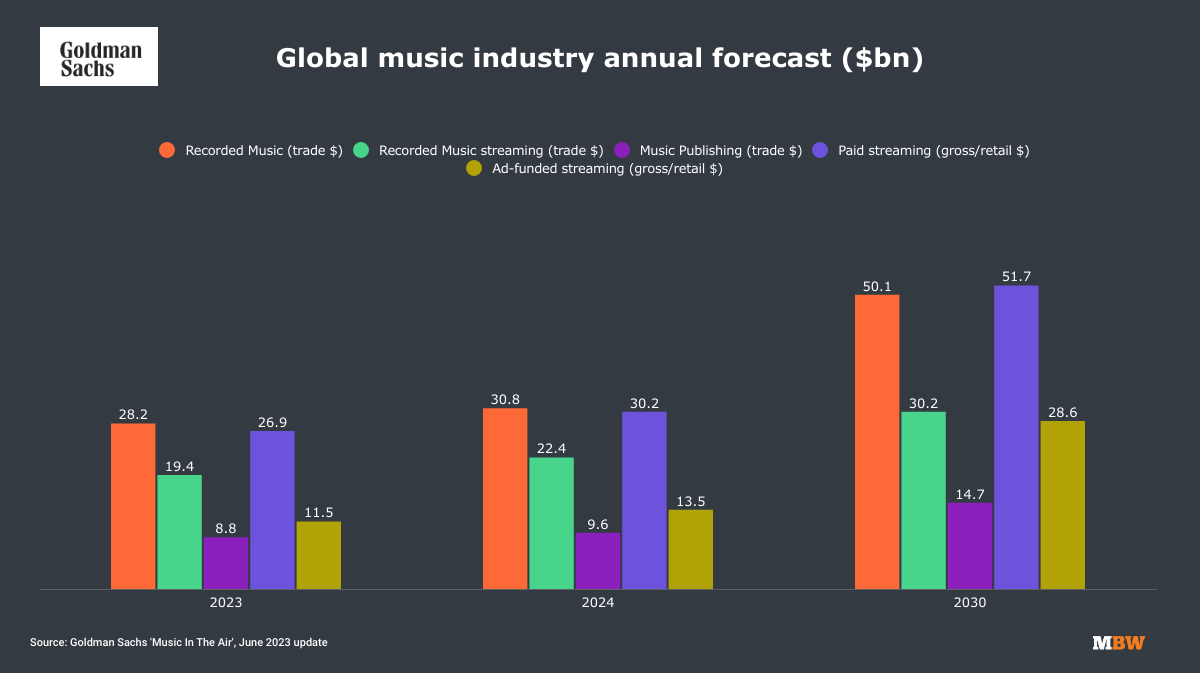

So: Goldman’s new paper suggests that, in 2030, the global recorded music industry will be turning over USD $50.1 billion annually. That’s down by 5.8% in real terms on the $53.2 billion Goldman’s previous paper (published in June 2022) forecast for the same year.

A precipitous decline? Nah.

CAGR, CAGR, burning bright

With the ‘root’ figure of Goldman’s reports liable to change YoY (via IFPI’s USD-constant-currency-tweaking), the best way to fairly monitor movements in Music In The Air’s forecasts is by looking at the yearly CAGR (compound annual growth rate) applied to its predictions.

As Goldman points out in its latest Music In The Air, it’s now forecasting an average CAGR of +8.6% for the recorded music industry between 2023 and 2030, a figure which it calls “broadly unchanged” from its previous predictions.

Its CAGR forecast for recorded music streaming growth in that same period (2023-2030) also remains “unchanged”, says Goldman, at +11%.

Meanwhile, Goldman now forecasts that global music publishing revenues will grow by a7.6% CAGR between 2023 and 2030 – an increase on its previous forecast of 5.9% – and that live music revenues will grow at a 5% CAGR in this period.

That being said, there is one particular factor – beyond all that IFPI currency business, as well as changes in Russia – that has influenced Goldman’s downgrade of its record biz revenue forecasts: because last year (2022) global recorded music streaming revenues didn’t grow as fast as Goldman thought they would.

Overall, recorded music revenues grew by 9.0% YoY at constant currency in 2022, according to IFPI – actually ahead of Goldman’s expectations (+7.8% YoY), thanks to segments such as physical music, performance rights, and sync.

However, the official growth of recorded music streaming revenues last year (+11.5% YoY at constant currency, according to IFPI) was significantly down on Goldman’s forecast for this segment in 2022 (+14.5% YoY).

Goldman has blamed “lower paid streaming ARPU” around the world for this miss, driven by three factors:

“Negative ARPU mix shift towards emerging markets which accounted for half of the subscriber growth but generated less than half the ARPU of developed markets”;

“Lack of major [streaming] price increases”; and

“Dilution from family plans (we estimate 30% dilution) and bundles”.

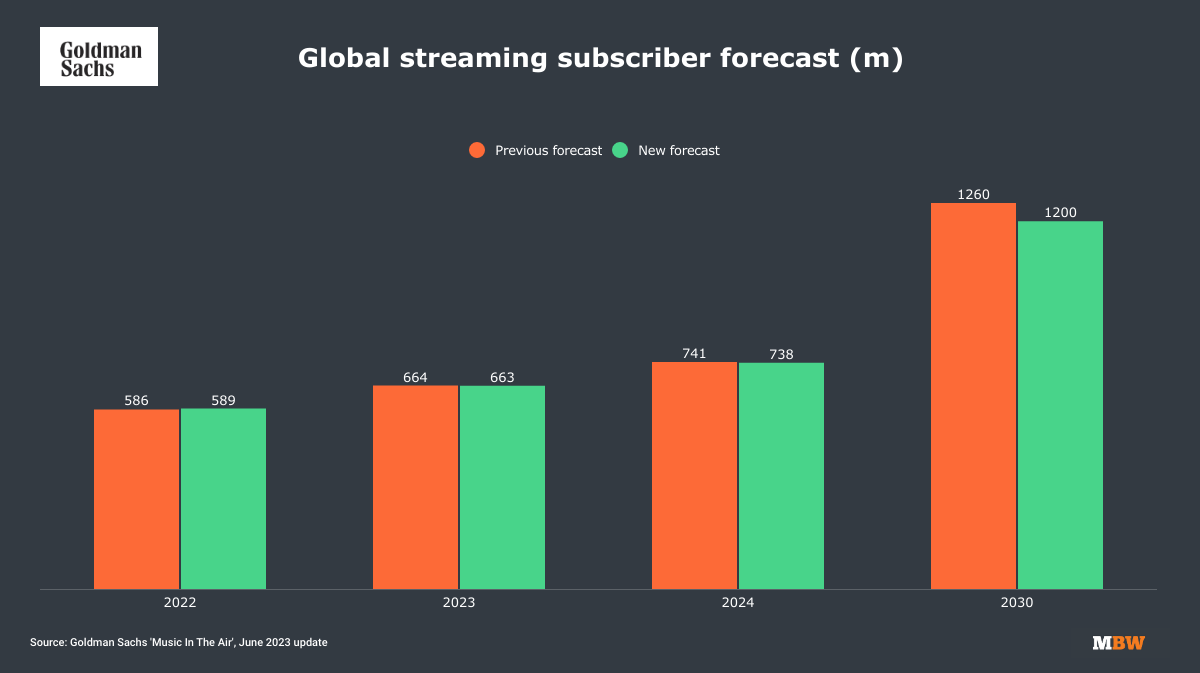

In terms of the number of paying subscribers to music streaming platforms worldwide, Goldman’s forecasts (see below) remain very similar to where they were before – though it’s shaved 60 million off its previous 1.26 billion subscriber forecast for 2030, “partly reflecting the exclusion of Russia from our estimate”.

As for 2023 itself?

Goldman is predicting “resilient” revenue growth of7.5% YoY for the global recorded music industry this year (an upgrade on its 7.3% prior prediction), with the music publishing industry forecast to increase revenues by 8.2% YoY (vs. Goldman’s 5.6% prior prediction).

However, Music In The Air’s prediction for recorded music streaming revenue in 2023 has been pared down: Goldman now expects 2023’s global music streaming revenue (gross) to grow by 11.9% YoY (vs a 13.0%previous forecast).

It also expects net/wholesale recorded music streaming revenue (i.e. the money paid to labels and artists) this year to grow by 12.0% YoY(again, vs. 13.0%in its prior predictions).

Those, then, are the headline numbers from the latest Music In The Air – penned once again by Goldman’s Lisa Yang and team.

The 72-page report offers much more than that, delving as it does into various hot music industry topics, and offering up a few data revelations.

Below, MBW pulls out five other interesting tidbits from the report – including the one in our headline above about TikTok…

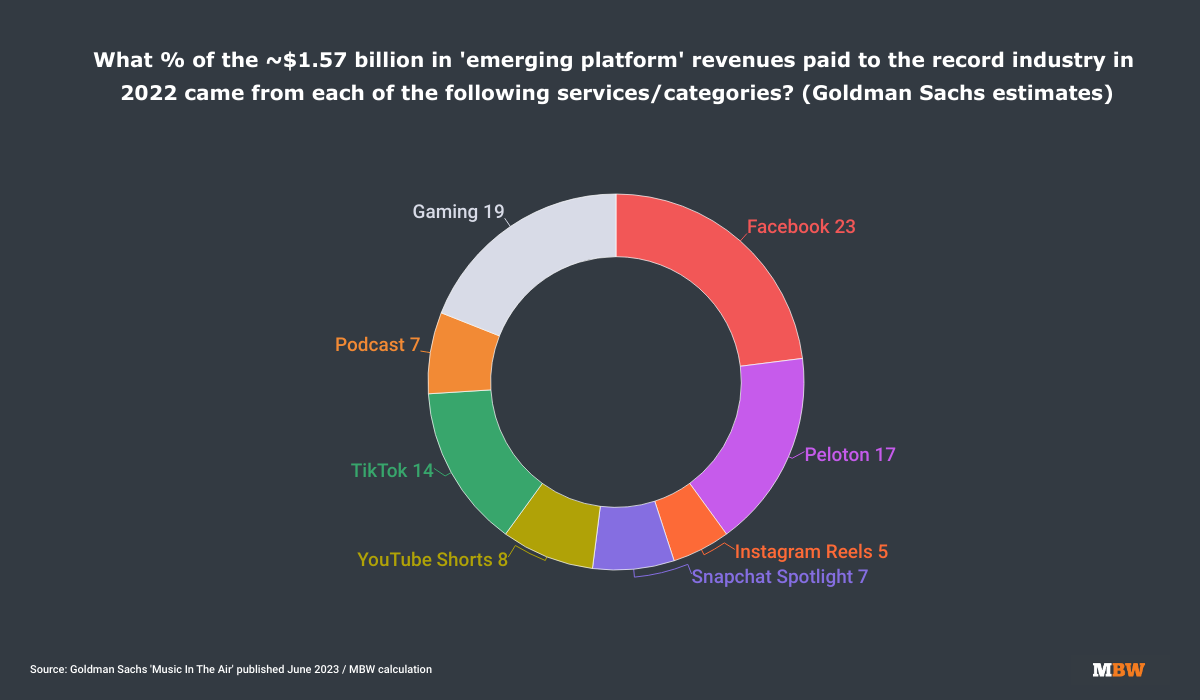

1) TikTok paid the music industry less than Peloton, according to Goldman’s numbers

In its previous Music In The Air report (June 2022), Goldman Sachs estimated that TikTok contributed 13% of the revenue paid to the recorded music industry from ’emerging platforms’ in 2021.

In the latest Music In The Air, Goldman Sachs estimates that 6% of the global recorded music trade’s revenues last year came from these ’emerging platforms’, which would equate to $1.57 billion.

TikTok’s standalone contribution of the ’emerging platform’ revenue total paid to the record industry last year, says Goldman, was 14% – which works out to approximately USD $220 million.

That was bigger than the equivalent estimated contributions from both YouTube Shorts (8%, or $126m) and Instagram Reels (5%, or $77 million).

None of these platforms, however, could match the revenue paid to the recorded music business via Peloton, which Goldman Sachs estimated to contribute 17% of ’emerging platform’ revenue in 2022 – or approximately $267 million (see below).

Goldman Sachs is bullish on the future contribution to the recorded music industry from these ’emerging platforms’: It predicts in the latest Music In The Air that ’emerging platforms’ will account for 14% of global recorded music revenue (up from 6% last year) by 2030.

Goldman also forecasts that ’emerging platforms’ will account for a whopping 47% of the recorded music industry’s revenue from ad-funded streaming by 2030.

(Worth noting: Goldman categorizes all of the above as ‘ad-funded streaming’ revenue, with the exception of Peloton, which it files under subscription revenue.)

(Also worth noting: TikTok’s music boss, Ole Obermann, has publicly said he disagrees with Goldman’s estimates of TikTok’s revenue payouts to music rightsholders from the June 2022 Music In The Air paper. TikTok did not comment when contacted by MBW about Goldman’s latest numbers.)

2) Believe has been upgraded to a ‘buy’ at Goldman Sachs

Goldman Sachs is a believer in the music business’s biggest companies.

In last year’s Music In The Air paper, Lisa Yang and team gave us a snapshot of their view on the publicly-listed stock of various media and entertainment firms.

“We expect Believe to continue gaining market share with its digital-first approach, particularly in the fast-growing emerging markets across Asia.”

Lisa Yang, Goldman Sachs

In the latest Music In The Air (June 2023), Yang and co. have once again rated UMG and Live Nation as a ‘Buy’ – but added Warner Music Group to their ‘Buy’ ratings, too.

Elsewhere, Spotify stays at ‘Neutral’, as TME is upgraded to the same rating.

Perhaps the most interesting shift in Goldman’s view concerns Paris-headquartered Believe (led by CEO, Denis Ladegaillerie, pictured inset).

Rated ‘Neutral’ in the June 2022 paper, Goldman has now upgraded Believe into its ‘Buy’ stocks.

Writes Lisa Yang: “We see Believe as set to benefit from structural tailwinds across the music industry including growth in streaming, new licensing opportunities created by new technologies, and the rise of the indies market.”

She adds: “Believe is one of the largest independent music companies globally, offering distribution services, Artist Services and Label & Artist Solutions to c.850,000 artists in 50+ countries. We expect the company to continue gaining market share with its digital-first approach, particularly in the fast-growing emerging markets across Asia.”

3) Goldman expects streaming prices to grow by 3% per year, on average, in established markets

See those optimistic music biz forecasts from Goldman at the top of this story for 2030?

Their materialization is, in turn, dependent on a specific assumption that Goldman is forecasting within its numbers: that headline prices at music streaming services in developed markets (US, Europe etc.) will increase by an average of 3% per year over the next seven years.

“We acknowledge that not all DSPs will raise prices at the same time and in every market; however, certain years may see larger/smaller price increases on average than others,” writes Goldman, citing recent 10% price increases at Apple Music (November 2022) and Amazon Music (February 2023).

In our Music Industry Model, we assume 3% annual pricing growth in DMs within our global paid subscription revenues… We acknowledge that not all DSPs will raise prices at the same time and in every market; however, certain years may see larger/smaller price increases on average than others.”

Goldman Sachs, Music In The Air (June 2023 edition)

Elsewhere in its headline predictions on changes in streaming monetization, Goldman notes that the “streaming remuneration model needs to adapt to increased supply and fraud”.

It says the ‘pro-rata’ streaming model now “needs to evolve” in order to “cope with the dilution of market share from (i) the ever-increasing number of songs uploaded onto streaming platforms, with the long tail of music being treated equally to premium music content, (ii) the rise of fraudulent/ artificial streams and (iii) the propensity of algorithms to push lower royalty content”.

Goldman further estimates that, having chewed over the available evidence and industry testimonies, “a low single-digit [percentage] of the royalty pool is [currently] lost to streaming fraud every year”.

4) Will the rise of the ‘superfan’ on streaming change the game?

In tandem with its statement that the dominant ‘pro rata’ music streaming royalty model today must “evolve”, Goldman’s latest paper explores potential alternative models.

These include user-centric payments – as deployed by SoundCloud for its ‘fan-powered’ payments today – as well the ‘artist-centric’ model touted by Universal Music Group boss, Sir Lucian Grainge (pictured inset).

Goldman summises ‘artist-centric’ as distributing payouts “based on the value an artist creates and provides for a platform”, and notes that, as such, “the model may differ between platforms, depending on what they consider as ‘value’”.

One component of ‘artist-centric’ that is definitely under discussion – judging by UMG’s most recent earnings call – is for streaming services to better monetize so-called ‘superfans’ of specific artists.

If 20% of paid streaming subscribers today could be categorized as ‘superfans’, says Goldman, and if these ‘superfans’ were willing to spend double what a non-superfan spends on digital music each year, it implies a $4.2 billion (currently untapped) annual revenue opportunity for the record biz.

That $4.2 billion figure, however, represents a ‘Total Addressable Market’ (TAM).

Goldman models out a scenario whereby things start off much slower, with just 10% of ‘superfans’ (i.e. 2% of total subscribers) paying a X2 price for their streaming service in the first year following the launch of a ‘superfan’-orientated product.

However, if this percentage of addressable ‘superfans’ paying for extra access could gradually be bumped up to 70% by 2030, says Goldman, it could end up bringing in an extra $4 billion-plus to the recorded music industry annually.

“Beyond headline price increases, we believe that there is an opportunity for the industry to improve monetisation through a premium segmentation of their user base.”

Goldman Sachs, Music In The Air (June 2023 edition)

Goldman doesn’t lay out exactly what this ‘superfan’ streaming product might entail, but it does nod in that direction, suggesting it would allow subscribers to “lean closer in to their favourite artists through their streaming platform”.

“Beyond headline price increases, we believe that there is an opportunity for the industry to improve monetisation through a premium segmentation of their user base, which would better align monetisation with the value created by an artist or a song for the platforms,” writes Goldman.

“The current streaming model does not distinguish between its users, charging each the same flat monthly fee, independent of the level of engagement with the platform and its artists.”

Goldman does not factor in this potential ‘monetized superfan’ upside into its headline forecasts, as outlined at the start of this report.Music Business Worldwide