MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. Only MBW+ subscribers have unlimited access to these articles. The below article originally appeared in Tim Ingham’s latest ‘Tim’s Take’ email, issued exclusively to MBW+ subscribers.

It’s no secret that Warner Music Group – like Universal Music Group and others in the business – has significantly cut costs in the past couple of years.

What’s less appreciated by many in the industry is how long this process has been going on at WMG, how large it is, and how visible its impact is becoming.

Example: WMG now has no dedicated recorded music head in either the UK or Germany – the world’s third and fourth largest recorded music territories, per IFPI data.

(UK boss Tony Harlow exited last year, as did the duo who oversaw Warner’s German/Central Europe outfit: Doreen Schimk and Fabian Drebe. Warner Music’s combined Central Europe and Benelux business unit is now run by Netherlands-based Niels Walboomers.)

Warner Music also has no in situ recorded music boss in another Top 10 territory, Canada: New York-based Eric Wong leads its Canadian operation from the US (alongside his two additional roles!). Former WM Canada boss, Kristen Burke, exited in October.

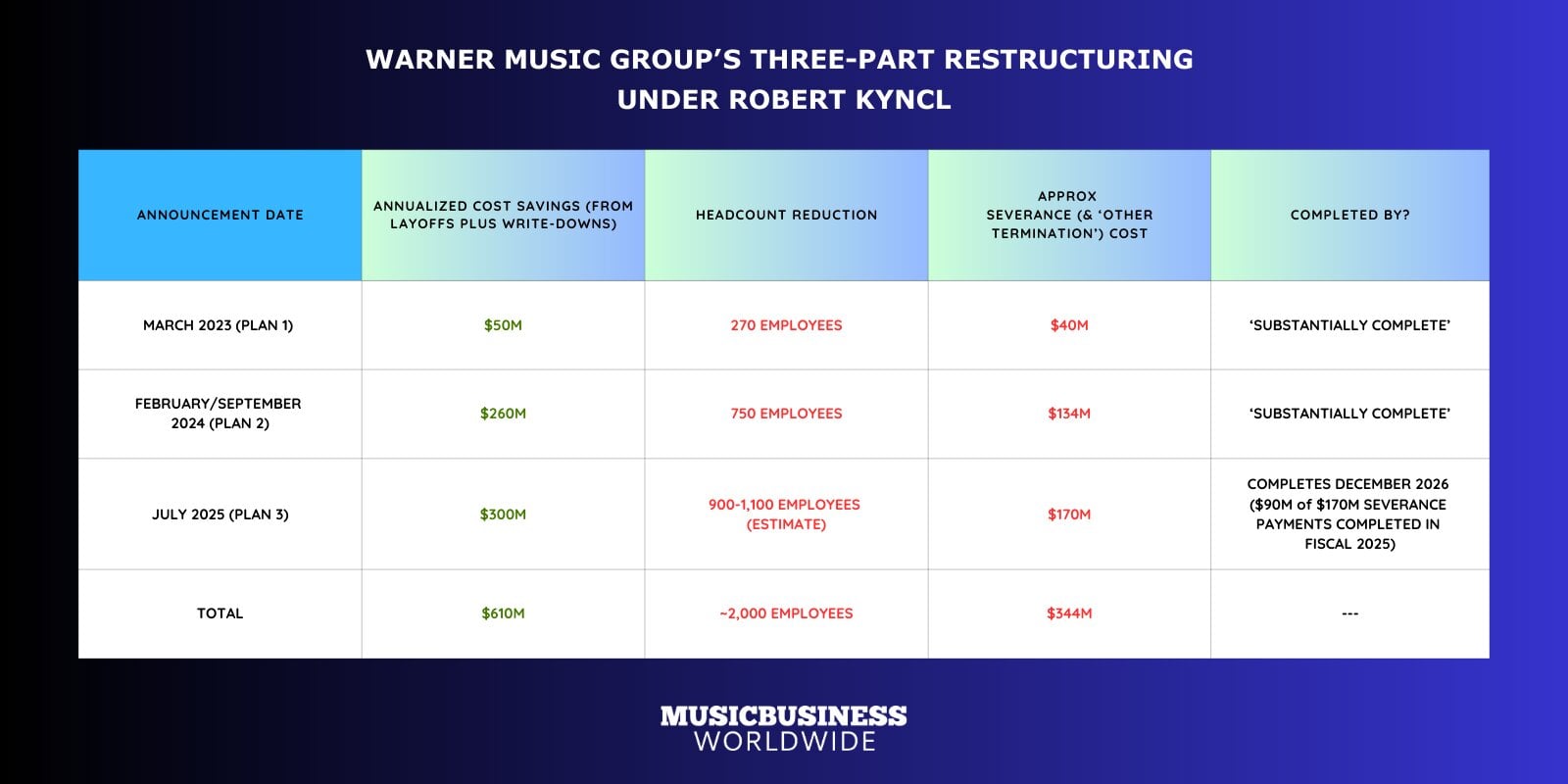

These are just a handful of significant changes that have sprung from a three-part restructuring program launched after Robert Kyncl became WMG CEO in January 2023:

- In March 2023, Kyncl announced WMG was laying off 270 people, a move which slashed $50M from the firm’s annual pre-tax costs;

- In September 2024, Warner confirmed it was cutting a further 750 employees, the majority from its ‘owned and operated media’ subsidiaries, resulting in additional annual cost savings of $260M;

- And in July 2025, Kyncl announced a further $300M of annual cost-savings, of which $170M would be achieved via layoffs. (Coincidentally, $170M is also the amount WMG expects to pay out in severance as a result of these changes.)

WMG didn’t reveal a specific number of roles that would be eliminated in its 2025 round – possibly because it would have been large enough to gobsmack.

Based on what we know from 2023 and 2024’s WMG cutbacks (and their average per-employee severance), I’d estimate 2025’s round will result in the loss of around 1,000 additional roles.

To recap: ~1,000 roles cut in 2023-24, and a further ~1,000 targeted in the 2025 plan.

These cuts have concentrated in WMG’s label business: through the program to date, 91% of redundancy expense has landed in Warner’s Recorded Music division, with 2% in publishing, and 7% in Corporate.

WMG’s most recent annual report confirms that the 2023 and 2024 restructuring plans are now both “substantially complete” – i.e. the ~1,000 roles earmarked for redundancy in stages one and two have already been extinguished.

As for the additional estimated ~1,000 job cuts mapped out in 2025?

Over half the associated severance – $90M of $170M – was paid before the end of September 2025, suggesting Warner is largely done.

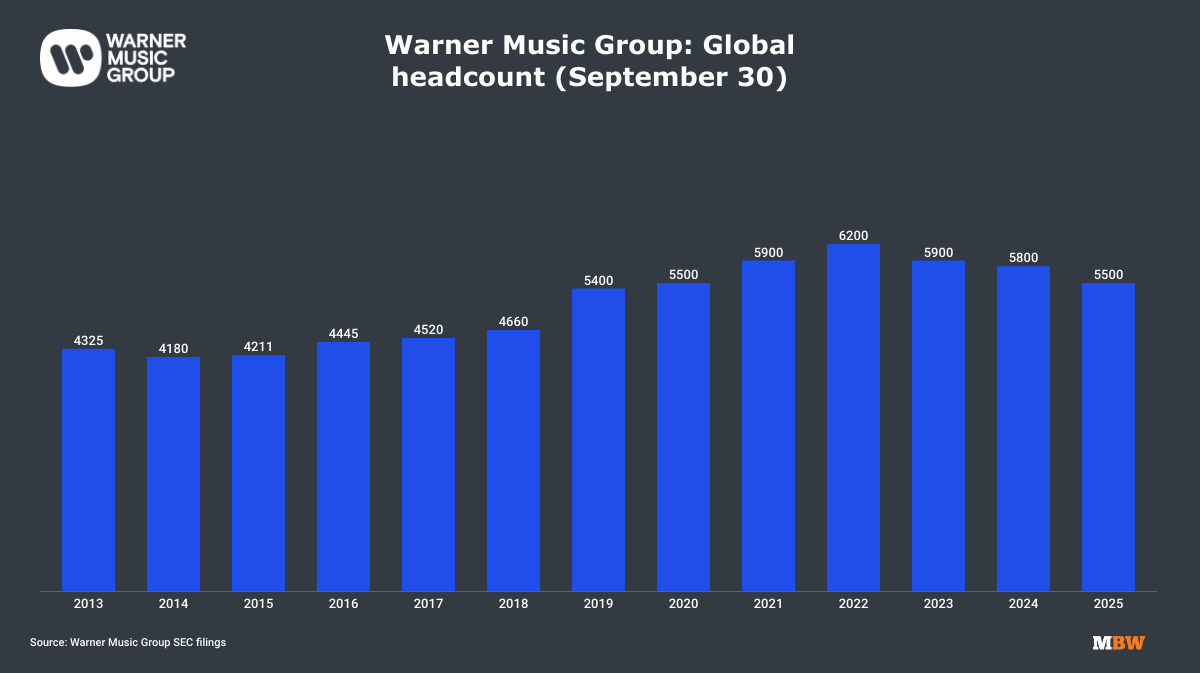

The impact of the restructuring is starting to show up in WMG’s public numbers.

At the close of its FY 2025 (September), Warner counted 5,500 employees around the world, according to its annual SEC report.

That was down by 700 people versus the equivalent figure in 2022.

Factoring in new hires, I expect Warner’s three-pronged restructuring program will ultimately reduce total staff volume by about 25% – from 6,200 employees before Kyncl’s arrival in 2023, closer to 4,700 by the end of this year.

Not all of that headcount reduction will be achieved through layoffs; some will come from asset disposals.

As I’ve written before, Warner’s recent sale of Songkick to Suno jettisoned 25 staff. Other employees exited when WMG offloaded its non-core media assets including UPROXX in 2024.

A further asset sale appears imminent: recent WMG filings confirm that merch platform EMP is being “held for sale” by the major.

(MBW first told you in August that Warner was looking to sell EMP, complete with a $70 million write-down in the asset’s value.)

Why the cuts – and where’s the money going?

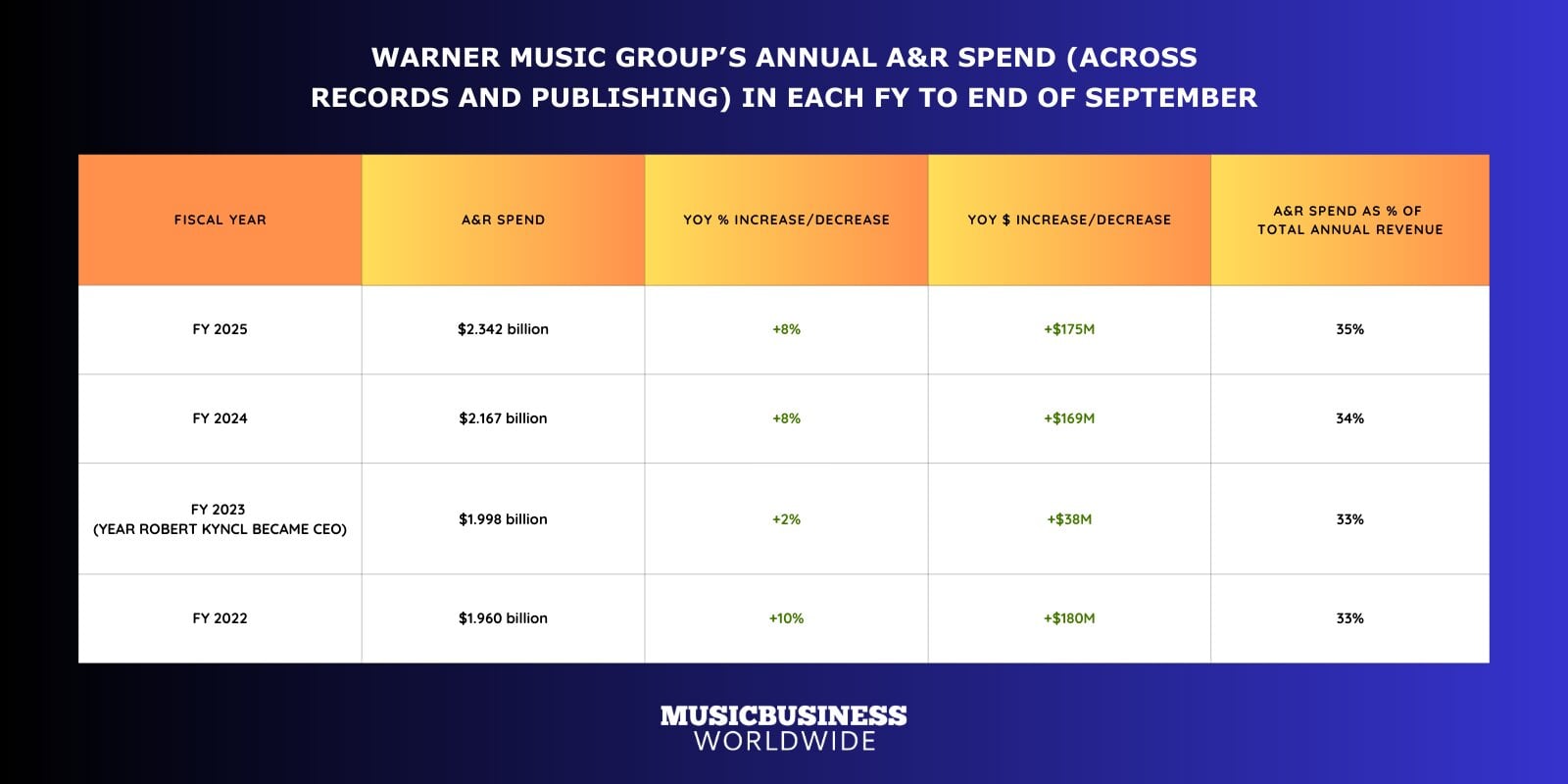

Throughout WMG’s three-year cutbacks program, Robert Kyncl has insisted that – in addition to being accretive to margin – Warner would look to reinvest a portion of the savings into A&R.

The numbers show Kyncl is coming good on this promise.

In FY 2025, according to its SEC filings, Warner Music Group spent USD $2.34 billion on ‘A&R’ across records and publishing (this figure includes royalties and advances paid to talent, plus studio costs).

That A&R figure was up 8%, or by $175 million, versus the prior year.

It was also up by $382 million vs. the equivalent figure in the year before Kyncl joined WMG (FY 2022).

Most importantly to Warner’s shareholders, WMG’s restructuring program has also helped drive up the firm’s margins.

In FY 2022, WMG’s Adjusted OIBDA (Operating Income Before Depreciation and Amortization) represented 19% of its annual revenues. By FY 2025, that figure had climbed to 22%.

An OIBDA margin in the mid-twenties will be next on investors’ wish list.

The bigger picture – and a platform for growth

Of course, Warner isn’t alone in making cutbacks to its workforce. Multiple industry players are sharpening their focus on profitability – while taking better advantage of technological efficiencies, and recalibrating resource towards high-growth markets.

Universal Music Group, as mentioned, has its own ‘realignment’ program underway, designed to produce EUR €250M (around USD $290M) in annual cost savings. UMG’s Boyd Muir confirmed last summer that UMG expected to be around two-thirds of the way through this two-phase plan by the end of calendar 2025.

Elsewhere, BMG boss Thomas Coesfeld has been open about restructuring headcount in the past few years – while significantly improving profitability.

Efficiency-seeking moves can also be seen at firms like Believe, which just this week eliminated the CEO role at key subsidiary TuneCore. (Following the departure of long-time TuneCore boss, Andreea Gleeson, the DIY platform will now be CEO-less – overseen by Believe’s global head of music, Romain Vivien.)

Warner, though, is arguably making the most visible reductions, and the most material cuts in terms of percentage of total workforce affected.

Far from being a barrier to growth, this rapid restructuring under Robert Kyncl could yet prove to be a launchpad for expansion.

Warner can now look to drive topline revenue growth through inorganic means – without risking the dilution of its margin to levels that might trouble public investors.

Part of this inorganic revenue drive will, no doubt, come from catalog acquisitions via WMG’s $1.2 billion JV with Bain Capital.

But, as I’ve previously pointed out, Warner also has a serious issue on its hands when it comes to servicing independents – with ADA struggling to compete with the scale of The Orchard (and AWAL) at Sony, and Virgin Music Group at UMG.

Robert Kyncl has previously expressed a preference to “build” rather than “buy” WMG’s independent distribution operation. And in a service-based (rather than rights-ownership-based) field, there are arguments for why this makes sense.

But with WMG‘s turnover now roughly half the size of UMG’s – and UMG set to swallow Downtown/FUGA in the weeks ahead – is now the time for Kyncl’s team to make an acquisitive move in the expanding indie space?

Obvious targets for such a swoop would include ONErpm, UnitedMasters, Symphonic, and the fast-growing TooLost.

But I heard a whisper over the festive break that Bruno Guez’s Revelator was attracting heavy acquisitive interest. It could be a good fit for Warner.

Revelator would come with a respected tech stack that WMG could ingest and develop.

It also specializes in FUGA-esque white label services for indie labels – a potential turn-key solution for a major music company looking to rival FUGA when/if it falls under Virgin Music Group’s umbrella.

Meanwhile, Warner will be hyper-aware of its status in the global industry pecking order right now.

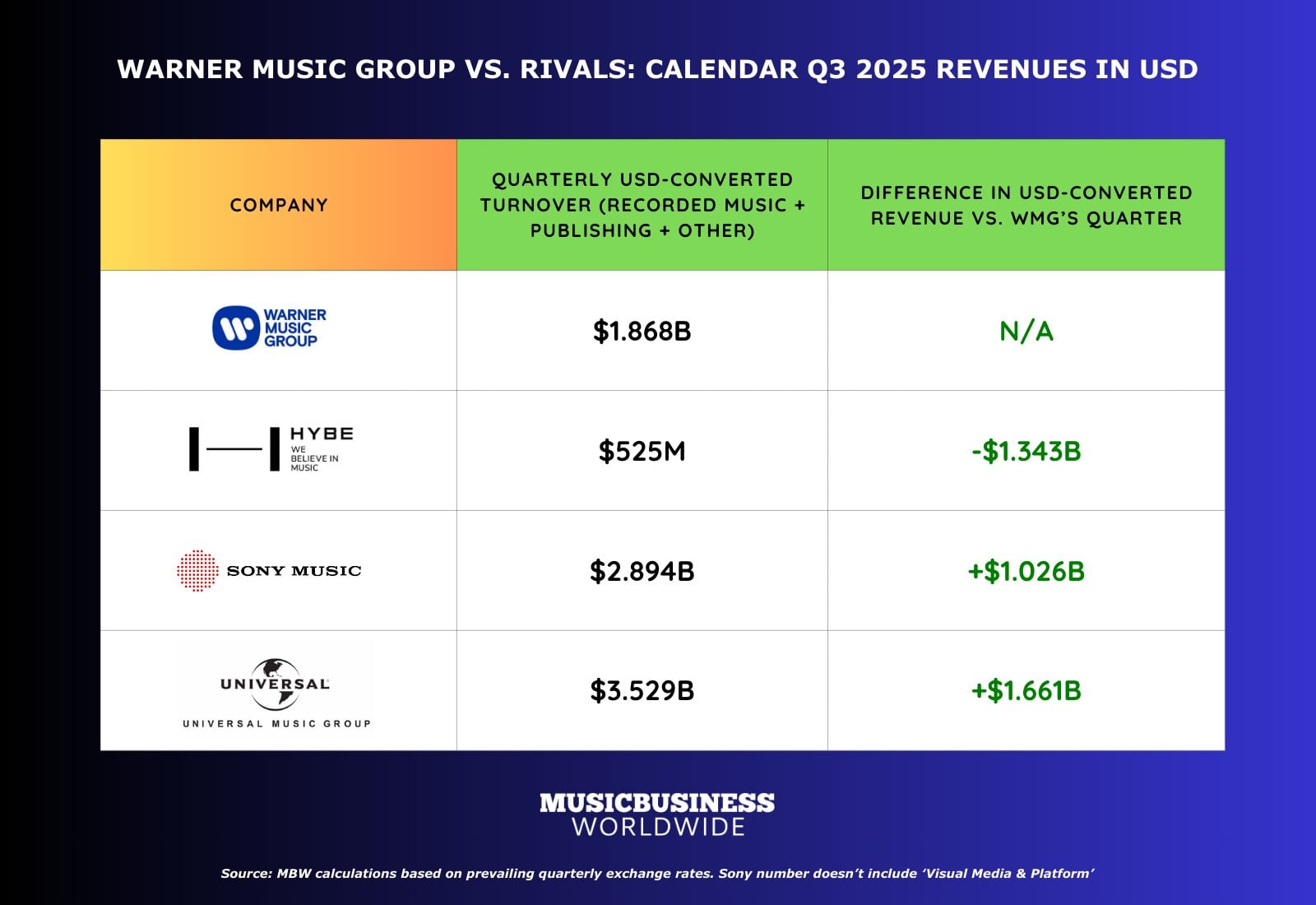

As I reported in November, WMG is nudging nearer to the day when its revenues are, in real terms, closer to those of HYBE than they are to Sony’s music rights business.

This year, HYBE will manage one of the most hotly-anticipated (and hotly-monetized) live shows of all time: the return of BTS after four years away, via a 79-date world tour.

In 2019, Michael Rapino, CEO of Live Nation, said that a billion people (!) had visited his company’s platforms to try and grab tickets to BTS’s then-concert run.

I’m not fully convinced an eighth of the world’s population were crazed about J-Hope and co (there would have been plenty of bots – and plenty of K-pop megafans willing to use them).

But it certainly sets the scene for what will be one of the worldwide industry’s biggest blockbuster money-makers in 2026.

With a supposed ‘independent’ in HYBE pulling the strings, expect plenty more discussion about the definition of ‘major’ music companies and ‘non-major’ music companies in the months ahead – and where both Warner and HYBE fit on the spectrum.

Music Business Worldwide