MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. Only MBW+ subscribers have unlimited access to these articles. The below article originally appeared in Tim Ingham’s latest ‘Tim’s Take’ email, issued exclusively to MBW+ subscribers.

Have you ever heard the story of the Hollywood maverick and the talking parrots?

It’s a perfect parable for why forecasting anything in the entertainment business is usually a waste of energy.

In 1934, an industrious press agent at Paramount Pictures was dreaming up stunts to promote Mae West’s upcoming theater release, It Ain’t No Sin.

He settled on a doozy: painstakingly training 50 parrots to repeat the movie’s title (‘It Ain’t No Sin! It Ain’t No Sin!’). The birds, he thought, would be ideal promoters of the flick in theater lobbies.

Then, at the eleventh hour, higher-ups at Paramount got worried that the film’s title might be too saucy for Hollywood censors. They changed the movie’s name to Belle Of The Nineties.

Legend has it that the 50 parrots, now useless as Tinseltown props, were released into the South American jungle – where they could be heard squawking “It Ain’t No Sin! It Ain’t No Sin!” for decades to come.

The moral of the story? In entertainment, unforeseen events (and corporate timidity) will often massacre best-laid plans.

But, hey, we’re at the start of a new year – so I’m gonna stick my neck out on three predictions for the music biz in 2026 regardless.

If I’m wrong, you’ll find me this time next year in the Bolivian rainforest, wide-eyed and be-beaked, repeatedly shouting the below at passing macaws…

1. The major ‘labels’ will lean more heavily into live music

“I think [major music companies] will be full service companies in [5 years]. Today we don’t offer management; we don’t offer live promotion. There are a lot of services like that we’re not in the business of here in the United States… And I think that is going to change.”

This off-the-cuff comment from Warner Music Group boss, Robert Kyncl, in an October interview with Bloomberg, is worth remembering.

The three major music companies have long ceased simply being ‘music rights’ operations. The growing value to Universal, Sony, and Warner from adjacent income streams – particularly merch, name & likeness licensing, and live events – has been one of the stories of the past decade.

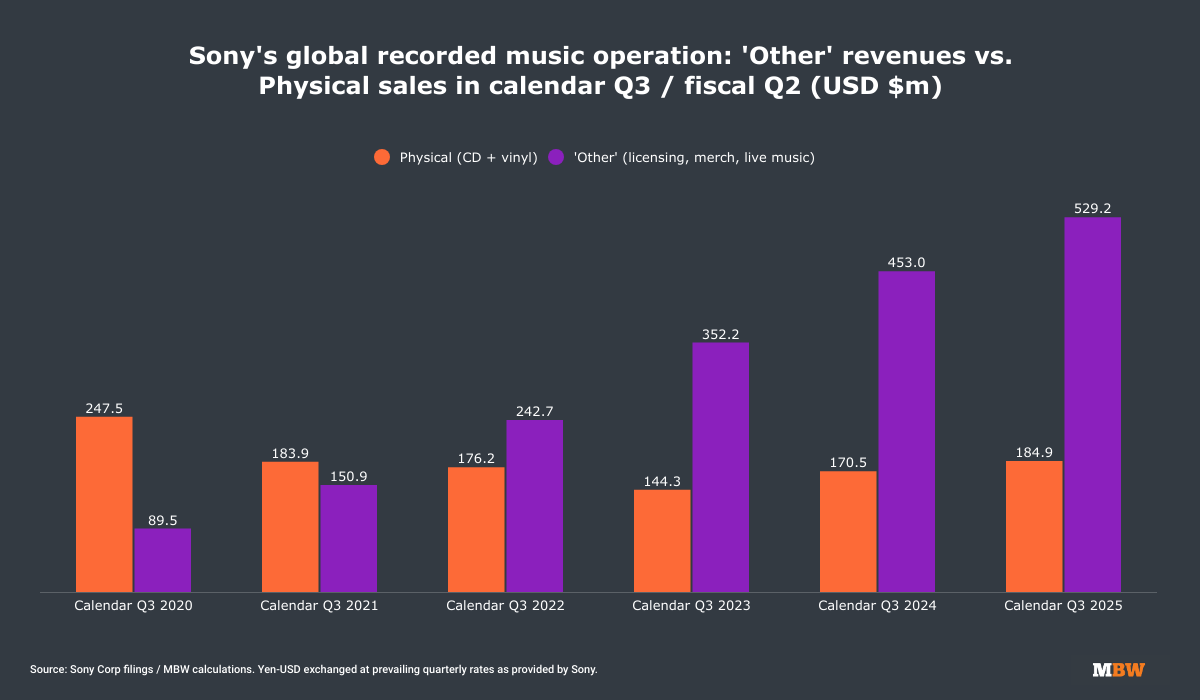

Case in point: In Sony’s financial accounts, its ‘Other’ category of recorded music income represents revenue generated from license revenue (public performance, broadcast, and sync) plus merch sales, and ticketing/live performances.

In calendar Q3, this ‘Other’ category generated over half a billion dollars (USD $529M) for the first time, up 16.8% YoY.

In fact, ‘Other’ generated nearly three times the revenues of global physical music sales for Sony in the same period ($184.9M).

As recently as 2021, physical sales generated a larger figure at Sony than ‘Other’. Just look how that’s changed since:

Some of the story in the chart above is explained by a post-Covid bounceback for public performance licensing (bars, clubs, restaurants etc.). But much of it has been driven by ‘non-traditional’ areas for a record company… particularly merch.

It’s no fluke that Sony acquired merch powerhouse Ceremony Of Roses – now believed to generate over $500 million annually – in 2022, just before the ‘Other’ revenue figure in the chart above exploded. (Also consider the impact of Sony’s acquisition of 50% of the Jackson Estate in 2024, and the continued income stream that deal provides from the live MJ musical.)

We’ve seen comparable live/merch revenue growth stories at Warner and Universal Music Group, as both majors look to offer services to artists far beyond the mainstay of music rights exploitation.

Universal’s merch arm, Bravado, is expected to generate around USD $900 million this year, while Warner’s ‘expanded rights’ business (which includes merch, in addition to touring and sponsorship income) generated USD $639 million in the first nine months of 2025, partly thanks to WMG providing merch services for Oasis’ global tour.

As per Robert Kyncl’s suggestion, don’t be surprised to see the three majors attempt to build on their success in merch by expanding further into live music promotion over the next 12 months.

Especially in a world where streaming is settling into single-figure growth patterns, and better monetization of so-called ‘superfans’ becomes an increasing fixation in major-land.

As WMG’s latest annual report says: “We believe that entering into expanded-rights deals [including] areas such as merchandising, VIP ticketing, fan clubs, concert promotion and management has permitted us to diversify revenue streams and capitalize on other revenue opportunities. This provides for improved long-term relationships with our recording artists and allows us to more effectively connect recording artists and fans.”

2. Universal gets Downtown – but who gets Curve?

A few months ago in this column, I called out Merlin for not buying FUGA back in 2020 — for allowing it to be acquired by Downtown and, ultimately, enabling UMG to swallow it via M&A.

Well, here comes a second bite at the apple.

Universal Music Group now seems resigned to divesting Curve Royalty Systems to get the Downtown deal approved in Europe.

The EC flagged concerns that UMG could use Downtown-owned Curve to “gain access to commercially sensitive data” from indie labels; in response, UMG has formally committed to selling it.

The proposed terms include strict purchaser criteria: Curve’s buyer must be financially robust, genuinely independent from UMG, with ‘proven expertise’ to run the business.

If Merlin is bold enough, this could be its moment. A collective of powerful independents, whose primary purpose is licensing and royalty collection, acquiring a platform that already services many of its members.

Then again, would UMG — bruised by Merlin members vocally opposing the Downtown deal — look kindly on their bid?

Other potential suitors could include B2B service providers like SESAC/AudioSalad, or royalty processing specialists such as Vistex or Milana Lewis’ Tone.

One wrinkle worth watching: under the proposed package, UMG gets to keep its own duplicate of Curve tech — “sanitized” of third-party customer data, but fully functional and free to develop independently.

In other words, Universal walks away with a battle-ready royalty accounting platform built on years of Curve’s R&D – albeit with a time-limited ban on poaching Curve’s existing standalone customers.

Meanwhile, for UMG, the main prize — Downtown’s publishing administration empire, FUGA’s B2B infrastructure — appears firmly within grasp.

3. The Suno deals get done

There are things in the WMG/Suno deal that unnerve me.

The fact that Suno’s own fundraising pitch deck, released before the agreement, was so light on financial commitments for music licensing. The fact that Suno now says it will “deprecate” its previous models post-WMG license… but no-one seems to be able to precisely confirm what “deprecate” means. The fact that compensation for Suno’s past infringement is unclear – a crucial distinction for songwriters and artists whose work was hoovered up without permission.

However, two headline facts from the Suno/WMG pact make me think other key rightsholders will, eventually, come on board.

Firstly, it sets a vital precedent that music must be licensed by gen-AI platforms… and that provably derivative future AI hits must send royalty cash back to the musicians they’ve ripped off (and who opted in to being ripped off).

Secondly, I’m increasingly convinced that Warner Music Group grabbed a minority equity slice in Suno as part of the deal. Expert industry whisperers are only solidifying my belief that’s what’s played out here.

Whatever concerns and brickbats are being aired between Suno and the likes of Universal, Sony, and Merlin, one thing’s for sure: if a chunk of ownership is on the table, all parties will be that much more motivated to lay down their litigious weapons, and make the peace.

Music Business Worldwide