MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. Only MBW+ subscribers have unlimited access to these articles. The below article originally appeared within January’s MBW+ Monthly Review email, issued exclusively to MBW+ subscribers.

Universal Music Group essentially confirmed on Friday (January 12) that a round of redundancies is coming/underway at the company. Said confirmation followed a report in Bloomberg, whose headline suggested UMG will be laying off “hundreds” of staff globally.

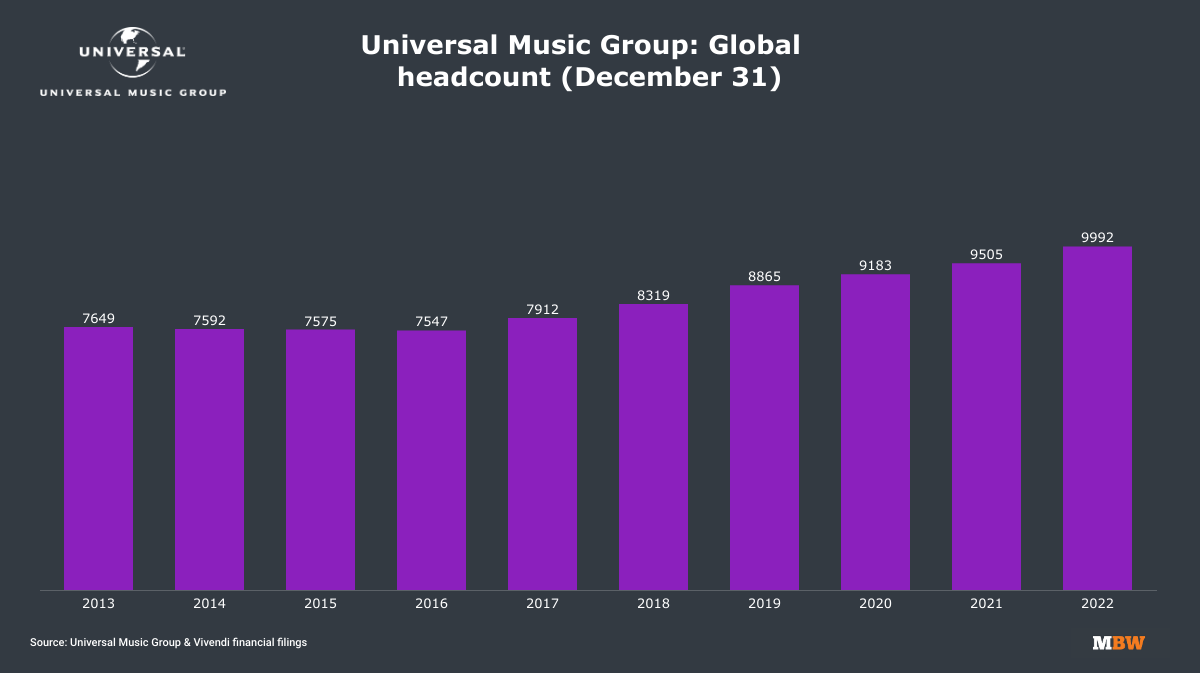

In truth, this was all quite predictable: UMG top brass told investors in October that they were preparing a “cut to grow” strategy for the start of 2024 that would see a trimming back of global employees. And while “hundreds” of layoffs deserve a certain amount of media hubbub, the mathematical reality offers useful context: at the end of 2022 (we don’t yet have updated stats for 2023), UMG employed 9,992 people, a figure that was up by 487 net employees YoY. UMG’s employee base also swelled the previous year (2021), up by 322 net employees YoY.

Last year, against a backdrop of widespread media layoffs, the music industry saw Warner Music Group lay off 4% of its global staff, SoundCloud lay off 8%, and BMG lay off around 3-5%.

Warner’s 4% reduction, as an example, saw approximately 270 roles cut.

By nature of Universal Music Group’s scale (9,992 employees at close of 2022, remember), a 4% reduction in headcount would see around 400 layoffs. A SoundCloud-style 8% cut would see 800 roles gone.

Don’t forget, though: In 2021 and 2022 alone, UMG added 809 net new employees. So we may be watching a company effectively erasing the additional headcount it added during the pandemic.

Much more interesting than ‘how many’ in this story is the ‘why’ and the ‘where’.

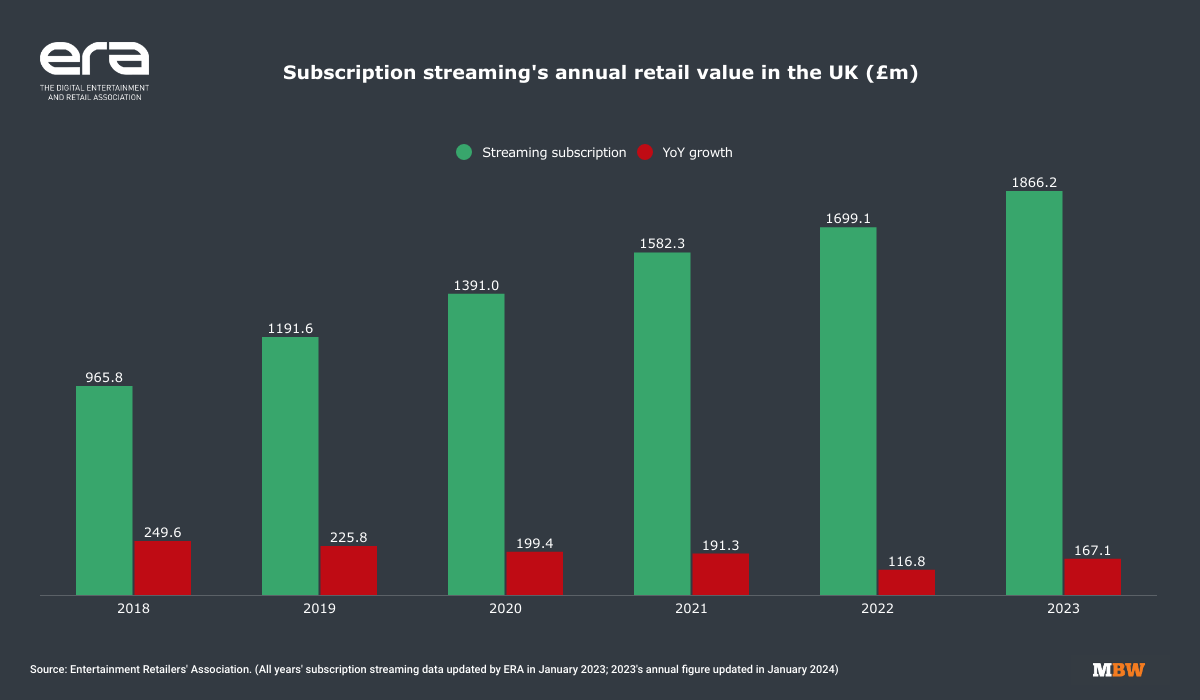

The ‘why’: The other week, we learned that UK consumer spending on the subscription music streaming market grew by 9.8% YoY in 2023.

That seemed like good news, but you have to factor in price rises by the likes of Spotify, Amazon Music, and Apple Music in the same year – price rises that saw flagship subscription costs for consumers rising by around 10% (i.e. from £9.99 per month to £10.99 per month). Conclusion: Without these price rises, the market would have been somewhere between flat and up by low single-digits.

Evidently, the trend of major music companies easily sailing to double-digit annual streaming revenue growth is getting bumpier, as mature markets edge closer to saturation point for paid streaming subscriptions.

In addition to investments in emerging markets, new skillsets are required within the three majors to steer them towards fresh areas of monetary opportunity beyond streaming – including the D2C opportunity, the music-plus-AI opportunity, and the much-discussed potential of ‘superfans’ who may be willing to pay more for access to a richer digital experience from the artists they love.

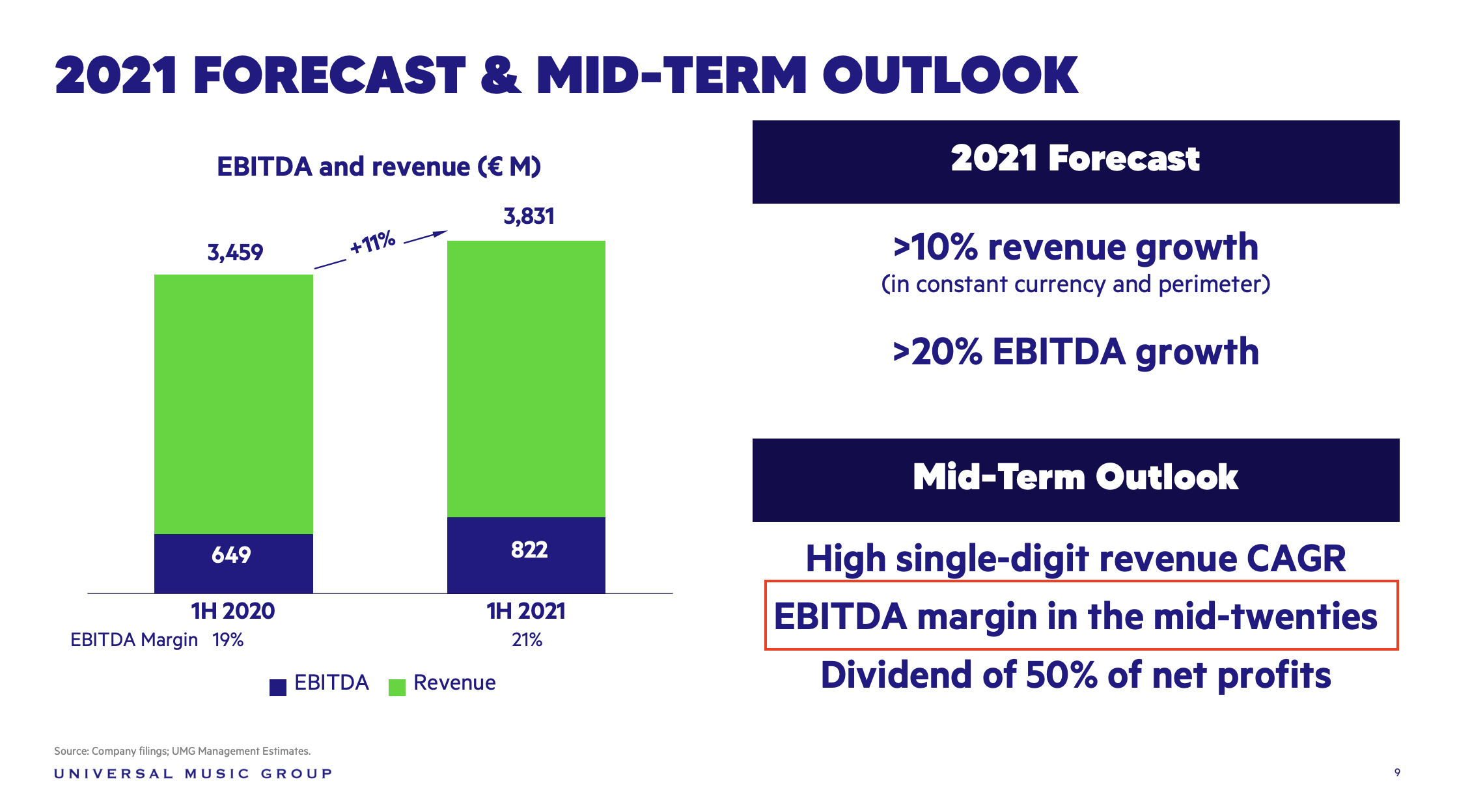

UMG also has a promised margin expansion to achieve: ahead of its 2021 float, the company pledged to investors that a mid-20% (i.e. 25%) EBITDA target was possible in the “mid-term”.

That “mid-term”, if we’re permitted to see it as a five-year-ish unit of time, is not far away. UMG’s adjusted EBITDA margin in the first nine months of 2023 was 21.4%, so it still has some profitability ground to make up.

The ‘where’: I’ve heard a lot of guesswork in the past few weeks about how UMG’s setup in the US might be affected by the new restructuring. For example, in the recent past, UMG has shown a willingness for certain frontline labels to share back-office services while maintaining separate and autonomous A&R functions (see: Motown’s re-enveloping into Capitol Music Group last year). In its statement to media last week, UMG was very clear that it would be “maintain[ing] our industry-leading investments in A&R and artist development… [while] creating efficiencies in other areas of the business”.

Naturally, with UMG’s operational HQ in Santa Monica, much of the focus of said guesswork has been the United States. Yet according to UMG’s financial reports, 42% of the company’s headcount at the close of 2022 was in Europe – a bigger proportion than North America, which housed 39%.

The first major departure from UMG that I’ve seen announced on LinkedIn this month is Cornelius Ballin, MD of Universal in Austria and Western Balkans, who leaves at the end of January.

Ballin says that he exits Universal after 23 years with “immense gratitude for the people I met, the things I learned and the fun I had along the way”.

![]()