There’s an interesting shift taking place in the power dynamic between ‘major’ music rightsholders and DIY aggregators on the world’s largest subscription music streaming service, Spotify.

Spotify published its earnings for Q4 and FY 2023 last Tuesday (February 6), revealing that its Premium Subscriber base grew to 236 million paying users in Q4 2023 (ended December 31).

SPOT has since also filed its 2023 annual report with the SEC.

MBW has dug through the annual document, which provides details of already-widely-reported events at the company from the past 12 months, including rounds of layoffs in Q1 and Q4, impacting 6% and 17% of the company’s global workforce, respectively.

The report also confirms that Spotify made zero material acquisitions in 2023.

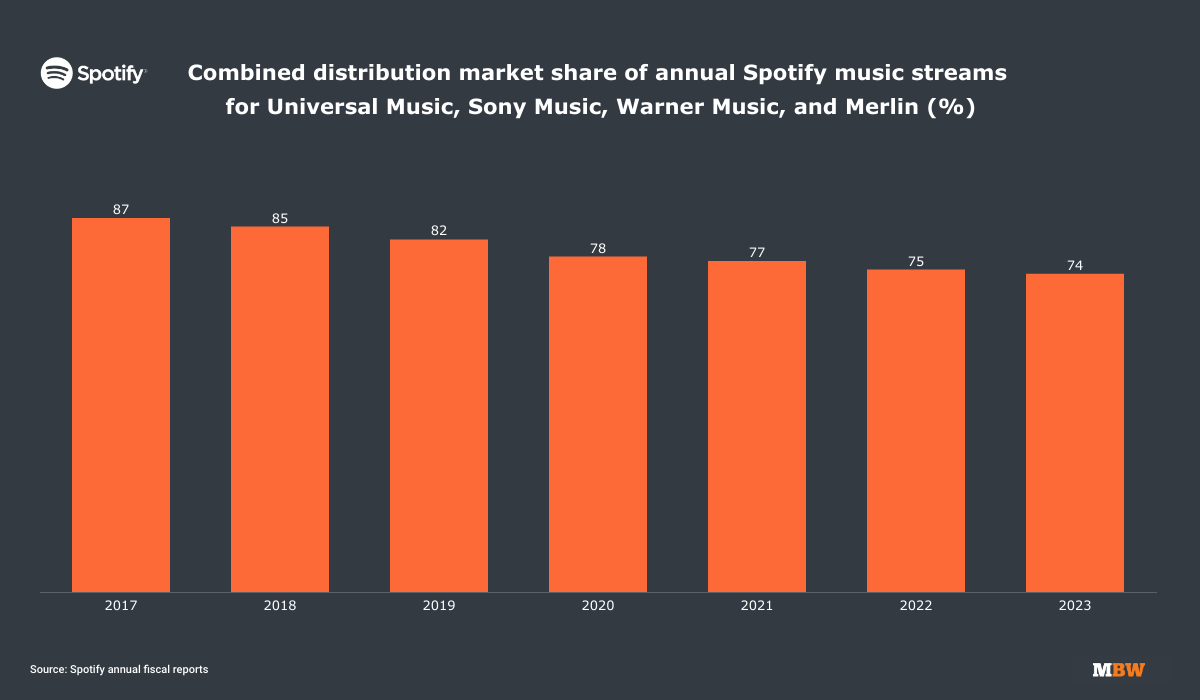

Perhaps the biggest takeaway from the document is this one: According to Spotify’s annual report, the joint market share of music represented by the three major record companies (Universal, Sony, Warner), plus independent label licensing representative Merlin, fell below three-quarters (74%) on Spotify for the first time in 2023.

Conversely, the global market share of recordings uploaded by DIY aggregators and indie labels with direct Spotify deals rose to an all-time high of (26%) in the same year.

In its 2023 annual report, under the section related to ‘Risks Related to Securing the Rights to the Content We Stream‘, Spotify explains that “the music industry has a high level of concentration, which means that one or a small number of entities may, on their own, take actions that adversely affect our business”.

It adds: “For example, with respect to sound recordings, the music licensed to us under our agreements with Universal Music Group, Sony Music Entertainment, Warner Music Group, and Music and Entertainment Rights Licensing Independent Network (“Merlin”), makes up the majority of music consumed on our service”.

For the year ended December 31, 2023, Spotify confirms that content from UMG, WMG, SME, and Merlin accounted for approximately 74% of streams of audio content delivered by the recorded music industry.

This means that UMG, WMG, SME, and Merlin’s joint market share on Spotify fell for the sixth consecutive year in 2023.

In 2022, UMG, WMG, SME, and Merlin’s joint market share was 75%. Back in 2017, it was 87%.

The most interesting thing about the 74% stat for 2023? The majors-plus-Merlin market share decline is slowing down versus previous years – as you can see from the chart below.

It’s important to highlight here that this 74% ‘majors plus Merlin’ stat does not reflect a simple partitioning of ‘majors’ vs. ‘indies’. If anything, it’s more ‘majors and large indies at Merlin’ vs. ‘DIY aggregators and non-Merlin indie record companies’.

An important clarification: Despite Merlin counting various independent aggregators as members (including DistroKid and CD Baby), the 74% stat only includes those Merlin members who have deals in place with Spotify via their affiliation with Merlin – as in, negotiated by Merlin and signed by Merlin on behalf of its members.

Non-major music companies amongst the 26% who did deals outside of Merlin include Paris-headquartered music company Believe (which is not a Merlin member) as well as its independent distro subsidiary TuneCore, plus rival aggregators such as DistroKid and CD Baby.

According to Spotify’s annual report: “We [have] direct license agreements with hundreds of independent labels, as well as companies known as ‘aggregators’ (for example, CDBaby, Distrokid, and TuneCore).”

Spotify notes that “the majority of these agreements have a multi-year duration, are generally automatically renewable, and apply worldwide” but that others, “with local repertoire, are limited to specific territories”.

Conversely, included in the 74% stat is music from independent labels who distribute their music via the indie arms of the three major music companies (i.e. Sony’s The Orchard, UMG’s Virgin Music Group, and Warner’s ADA).

Spotify is launching royalty changes this quarter (Q1 2024) that are expected to benefit artists signed to major music companies and premium independent labels (i.e. core Merlin members) – i.e. those artists whose recordings contribute to the 74% share of audio recordings licensed via recorded music rightsholders to Spotify in 2023.

Conversely, indie aggregators included in the other 26% face potential challenges from the introduction of these new ‘artist-centric’ royalty policies at Spotify – not least the 1,000 annual stream threshold and unique listener threshold (for which Spotify hasn’t shared the number).

Yet as you can see from the slowing decline of the three ‘majors-plus-Merlin’ market share on Spotify versus the market share of indie aggregators and “hundreds” of indie labels with whom SPOT has direct deals, the decline started slowing for some time before these ‘artist-centric’ changes came into effect.

This trend perhaps fits with the idea that “professional and professionally aspiring artists” continue to drive the vast majority of streams on Spotify, despite the continued rise of DIY acts.

Last week, speaking on his company’s fiscal Q1 earnings call with analysts, Warner Music Group CEO, Robert Kyncl, argued that, rather than becoming less relevant, the major music companies are now more relevant to the wider business than ever.

“As the music business has grown larger, faster, noisier, and more complex, with democratized distribution creating a flood of content on platforms, the role of large music companies is growing exponentially more relevant,” he said.

“It’s harder than ever for any one artist to break through the clutter. And that’s where we come in. We collect and process large volumes of data and make it usable and actionable, driving repeatable results – a task that is very difficult for any individual artist or small business, because of the resources and skill sets it requires.

“Our global marketing footprint and expertise, combined with deep technical capabilities to build systems and data insights, enable us to differentiate ourselves in this regard. In fact, looking at the last quarter, songs from the major music label groups represented 94% of the songs on Billboard Hot 100.”Music Business Worldwide