The major record companies are on course to generate over $14bn in total – with approximately $8bn from streaming alone – this calendar year.

That’s according to an MBW forecast based on recent fiscal results from Vivendi/Universal Music Group, Sony Corp and Warner Music Group.

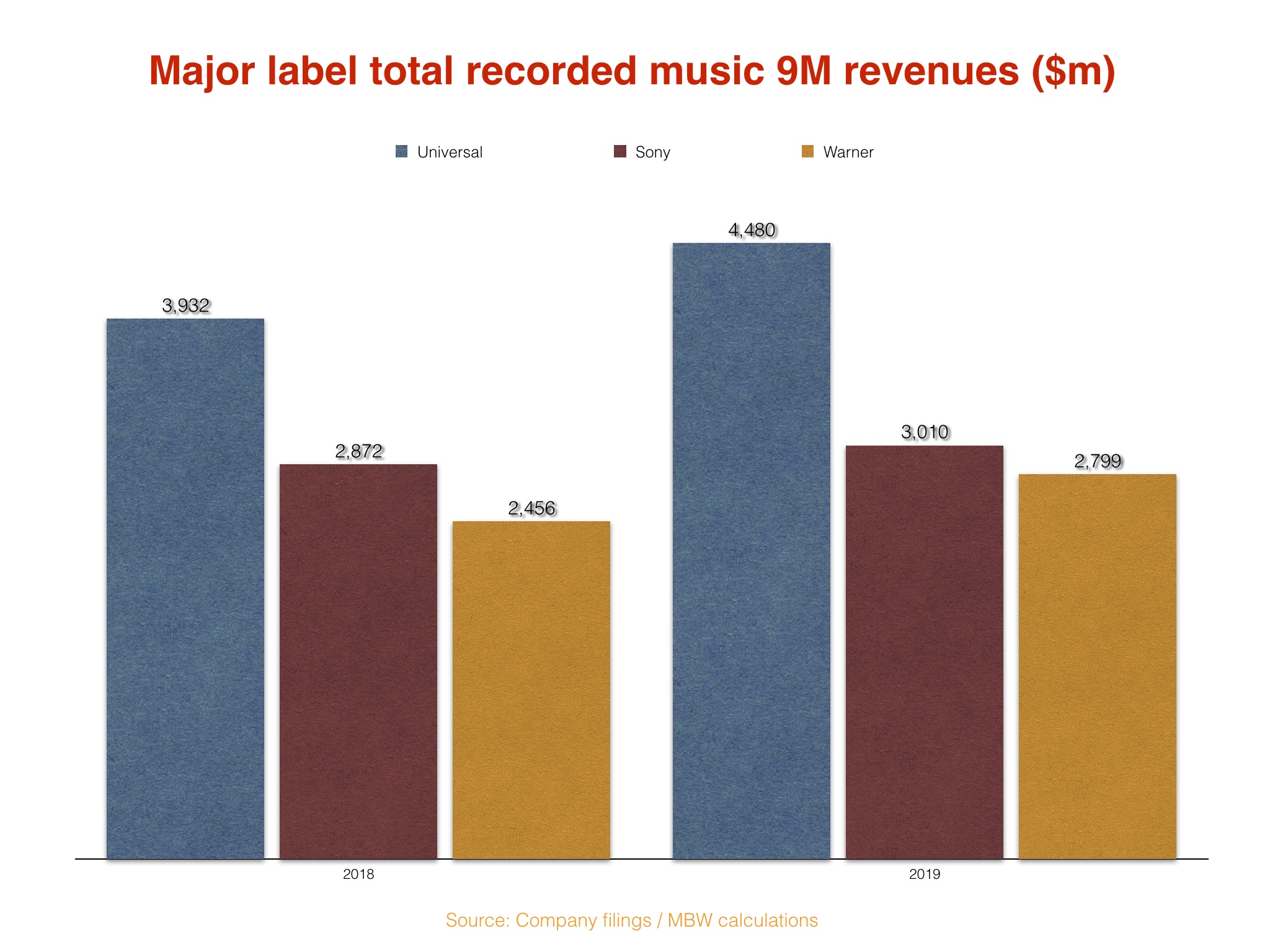

Our number-crunching shows that total recorded music revenues across the ‘Big Three’ in the first nine months of 2019 hit $10.29bn, significantly up on the $9.26bn they posted in the same period of 2018.

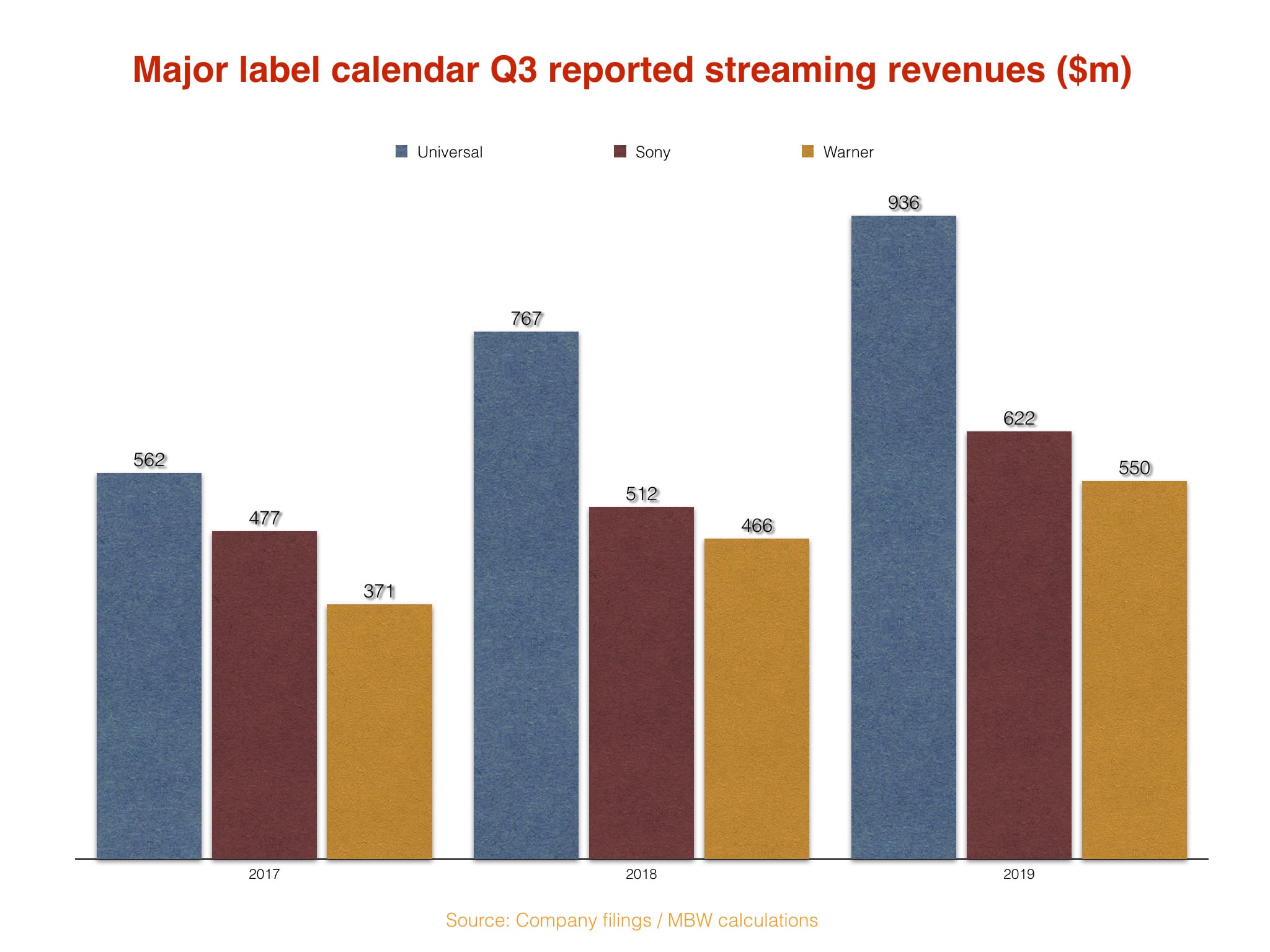

Collectively, in the final calendar quarter (Q4) of last year, the three majors generated $3.86bn from recorded music.

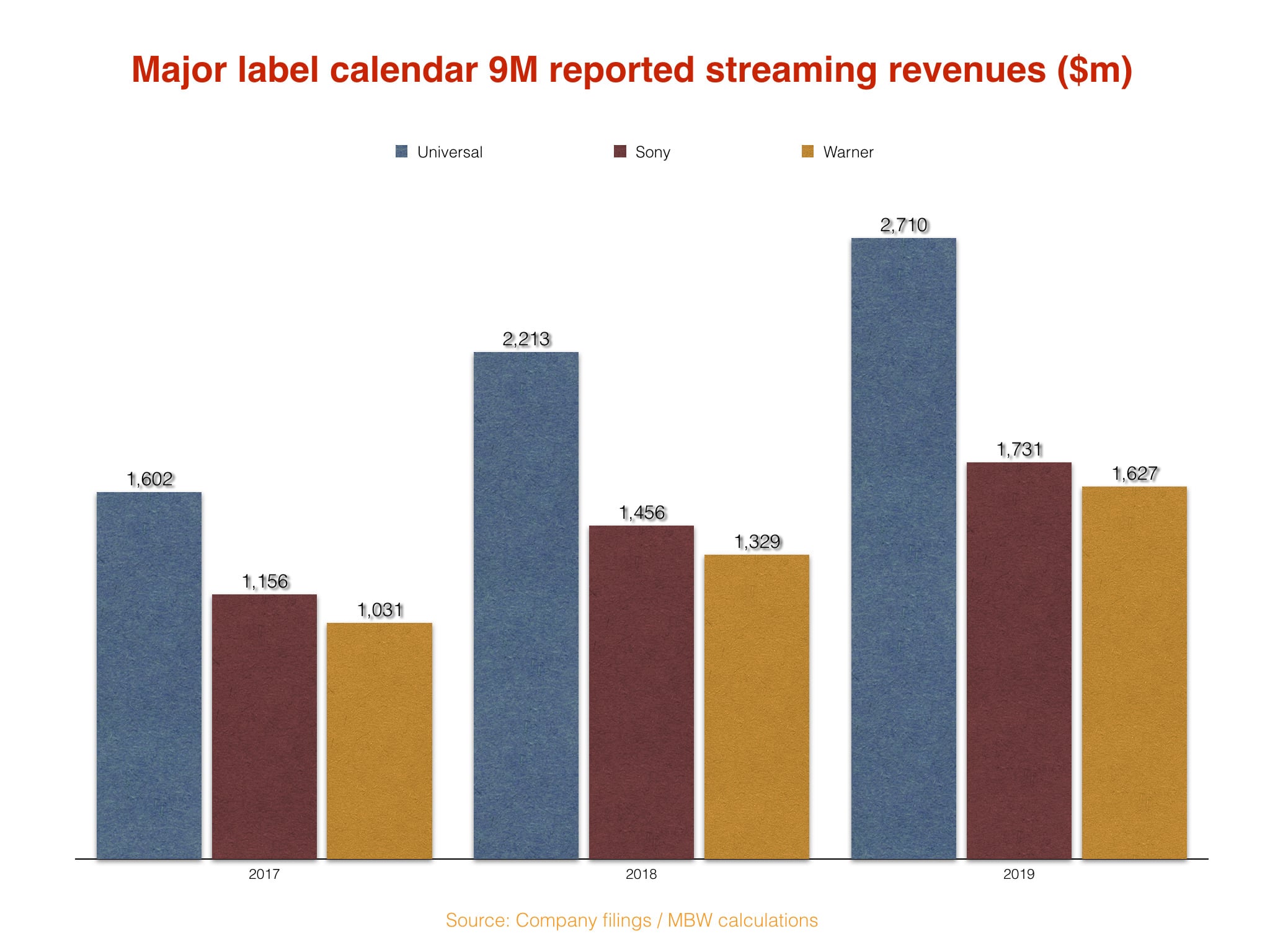

The majority of the major labels’ $10.29bn revenues in the first nine months of 2019 were derived from the likes of Spotify: Universal, Sony and Warner generated $6.07bn from streaming platforms in the 9M period to end of September, up by over a billion dollars on the $5.0bn they collectively generated from streaming in the same period of 2018 – a 21.4% YoY rise.

(Note: it’s understood that net revenue collected for indie labels via The Orchard is not included in Sony Corp’s results; in contrast, Universal and Warner are believed to include all revenue collected for indie label distribution partners in their results.)

Perhaps the most memorable stat to emerge today: in calendar Q3, the three majors collectively generated an average of $22.9m every day from streaming – a number which suggests that at some point very soon, Universal, Sony and Warner’s labels will be jointly raking in more than a million dollars every hour from Spotify, Apple Music et al.

Alongside these super-positive figures, however, there is a slight cause for… well, if not concern, then certainly conversation.

Because as the world’s biggest streaming territories mature, and the ARPU of certain platforms continues to tumble, one thing looks certain: the majors should prepare themselves for a deceleration in streaming revenue growth in 2019… and beyond (unless emerging markets, or emerging services, can pick up the slack).

So: the collective streaming revenue of all three majors in the first nine months of this year ($6.07bn) was up by $1.07bn on the $5.0bn generated in the same nine months of the prior year (2018).

Yet that $1.07bn figure was down by around $140m on the equivalent 9M year-on-year growth margin the majors saw from streaming services in the same period of 2018 (vs. 2017), which stood at $1.21bn.

Breaking this trend down further:

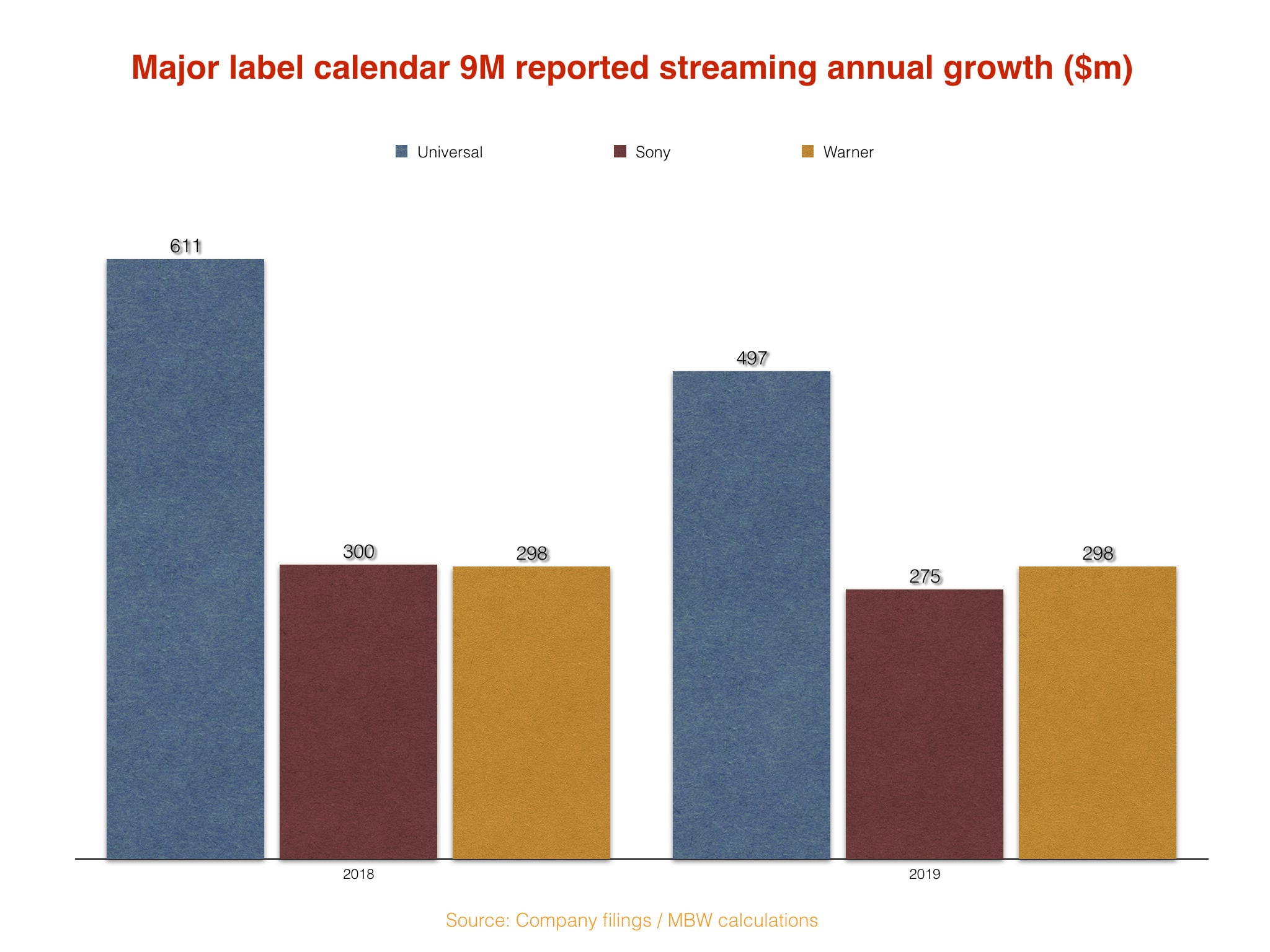

- Universal’s YoY recorded music streaming growth in the first nine months of 2019 (vs. 2018), according to MBW’s calculations, was $497m; in the same period of 2018 (vs. 2017) that figure was $114m bigger, at $611m;

- Sony’s YoY recorded music streaming growth in the same nine months of 2019 was $275m, down by a more modest $25m on the $300m it saw in 9M 2018;

- Warner bucked the trend (just); in the first nine months of 2019 vs. the same period of 2018, WMG’s recorded music streaming haul grew by $298m; in the first nine months of 2018 vs. the same period of 2017, it grew by exactly the same figure (see below).

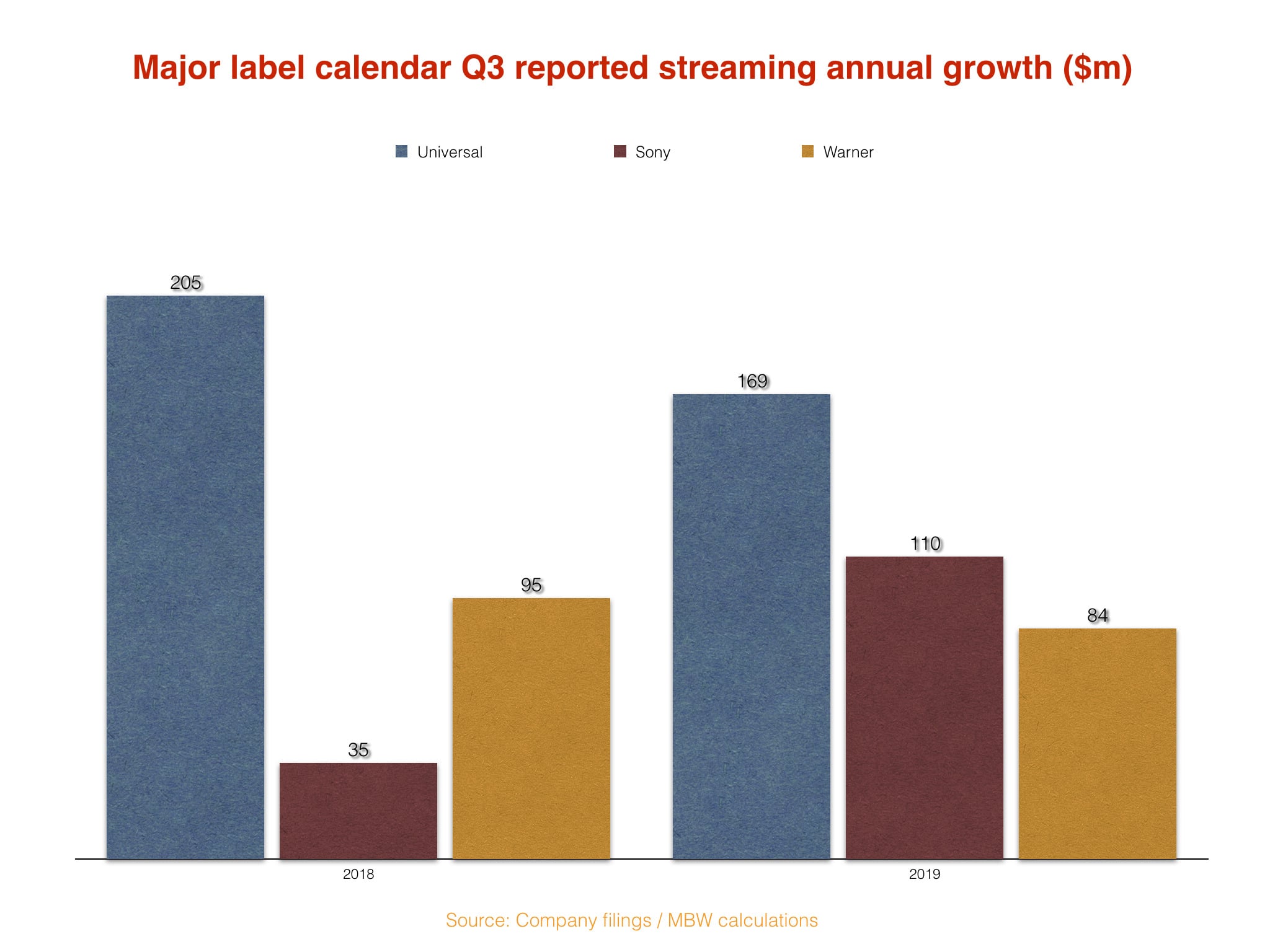

If we focus solely on calendar Q3 (the three months to end of September), we can see that Universal and Warner both saw a deceleration in YoY recorded music streaming growth – with UMG’s down from $205m in Q3 2018 to $169m in Q3 2019 and Warner down from $95m in Q3 2018 to $84m in Q3 2019.

Interestingly, looking at Q3 alone, Sony was the only the major to see its labels’ streaming growth accelerate in the period: it collected $110m more in calendar Q3 2019 than it did in the prior year; the equivalent figure in Q3 2018 was up by just $35m.

What does all of this tell us?

Well the first thing to say is, it’s hardly a disaster: remember, the majors will comfortably post more than $1bn in additional annual streaming revenue this year.

That number looks certain to be smaller than the equivalent figure from 2018… but, hey, a billion dollars is a billion dollars.

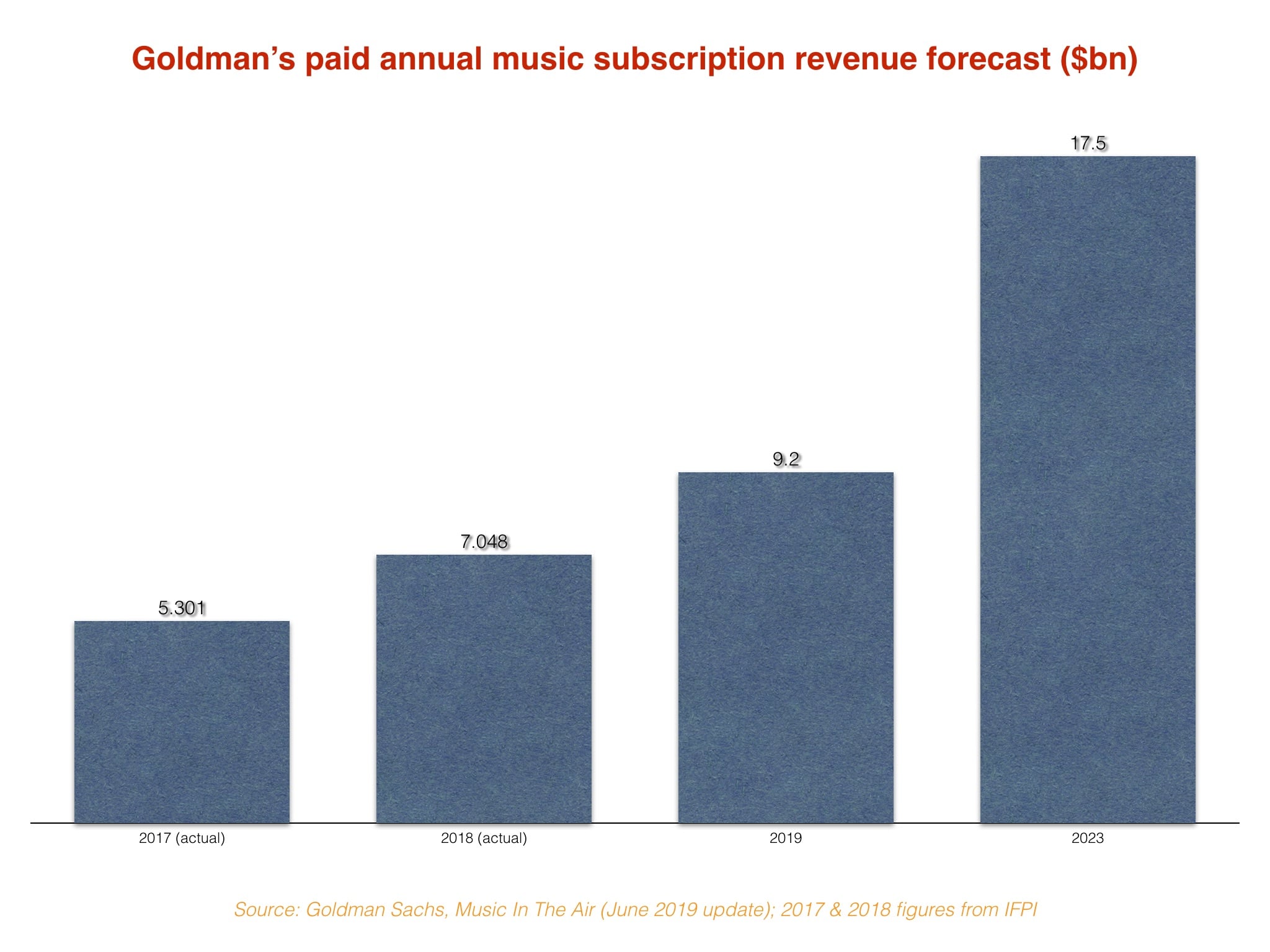

Yet cast your mind back to those dreamy Goldman Sachs headlines – and the financial company’s highly influential, very rosy predictions for the recorded music business’s future.

One of those predictions, found within Goldman‘s Music In The Air report, is that global paid subscription revenues for the record industry will climb from $7.05bn in 2018 to $9.2bn in 2019.

That’s a rise of $2.15bn YoY, which in turn represents a significant acceleration, rather than a slowdown, in annual streaming revenue growth for the worldwide business in 2019. (According to IFPI data, global subscription streaming revenues grew by $1.75bn last year.)

This must mean that one of two things is about to happen: (i) either Goldman is right, meaning that the major record labels will, as a consequence, concede streaming market share to the independent sector in 2019; or (ii) Goldman is not right, in which case the entire industry may follow the major label trend of posting smaller streaming growth this year than it did in 2018. Or both.

The majors, of course, are very aware of these trends, and are looking to the likes of India, China and Africa – not to mention new services from TikTok and others – to kickstart accelerated streaming revenue growth in future years.

And yet, within the recent annual filing of Warner Music Group, the following reference to a worst-case-scenario sticks out – echoing the sentiment, no doubt, across the world’s biggest music rights companies: “If growth in streaming revenues levels off or fails to grow as quickly as it has over the past several years, our recorded music business may experience reduced levels of revenues and operating income.”