The MBW Review gives our take on some of the music biz’s biggest recent goings-on. This time, we consider the power of new music makers on Spotify – and whether the streaming platform itself could ever really threaten the majors. The MBW Review is supported by FUGA.

“If Spotify owns the rights to the music it streams, it’s who earns the royalty payouts. That’s why Spotify has discussed traditional record label-style deals with artists. Musicians who cut these deals could get a cash advance in exchange for Spotify owning a percentage of their recording revenues.”

Is the music business really ready for Spotify Records?

As tensions mount over whether the major labels will ink new licensing deals with the service, Techcrunch put a rather incendiary spin on things this week.

The site – naturally tech-friendly, but with regularly solid sources – understands that Spotify is considering ‘becoming a label’ by signing ‘inclusive deals that aligns [it] with artists’ long-term success’.

Such a disruptive move, it suggests, is one of many examples of how ‘Spotify is finally gaining leverage over record labels’.

(With that headline, you’d almost think it was Universal, rather than Spotify, which desperately needs its suppliers to accept lower-than-market-rates.)

There’s no doubt that Spotify participating in artist rights would cause a fair bit of turbulence over at Sir Lucian‘s desk.

But there’s added complexity here.

Not least because the market share of ‘frontline’ artists on Spotify – like those described by TechCrunch – remains massively dwarfed by ‘catalogue’ music’s revenues.

And guess who controls the majority of that money…

Ever since Warner Music Group CEO Steve Cooper (pictured) uttered this sentence in an earnings call in August last year, it’s stuck in my mind.

To the great benefit of their bottom lines, the major labels are seeing ‘old’ (or, more accurately, ‘older’) music increasingly outpace the revenues of ‘new’ blockbuster music.

Yes, even the mighty Drake can’t hold back the mushrooming appeal of the entire history of recorded music.

Further stats bear this fact out.

Every year, Nielsen Music’s annual report offers insight into the commercial power of ‘new’ versus ‘old’ music in the US.

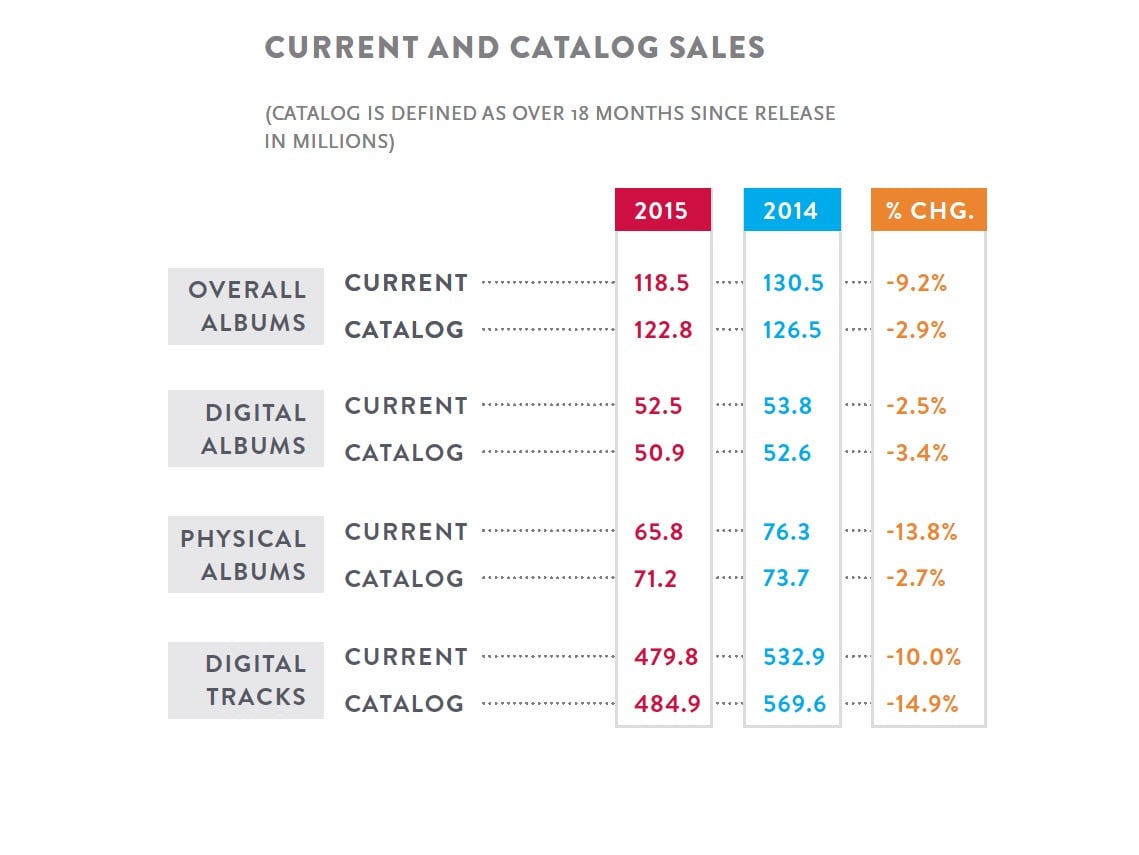

As MBW previously reported, across total ‘album consumption’ by volume in the States – including sales and track downloads, but not streaming – catalogue overtook new releases for the first time in history in 2015.

This trend was true in both physical albums and digital track downloads, with ‘new music’ still just edging it when it came to digital albums.

You’d assume that, in 2016, this pattern only worsened. (That’s ‘worsened’ from the perspective of a frontline label A&R exec.)

But we don’t know.

Because, for some reason… Nielsen decided to omit these stats from its annual report this year.

According to our label friends, there is a Nielsen figure out there for the portion of on-demand streams in the US market in 2016 defined as ‘catalogue’.

Want to take a guess?

73%. That’s 73% of the plays and, therefore you’d reasonably assume, 73% of the revenues.

So which music actually counts as ‘catalogue’ (or ‘catalog’ for our US readers)?

According to Nielsen’s system, any records released over 18 months ago.

That could be anything from Bieber to The Beatles, Ed Sheeran to Engelbert Humperdinck.

Let’s try and get a little bit more specific.

Nielsen’s main rival in the US number-crunching space is BuzzAngle.

Their annual report covering 2016 delivers a more granular picture of the stranglehold which ‘old’ records have on the marketplace – including on streaming platforms.

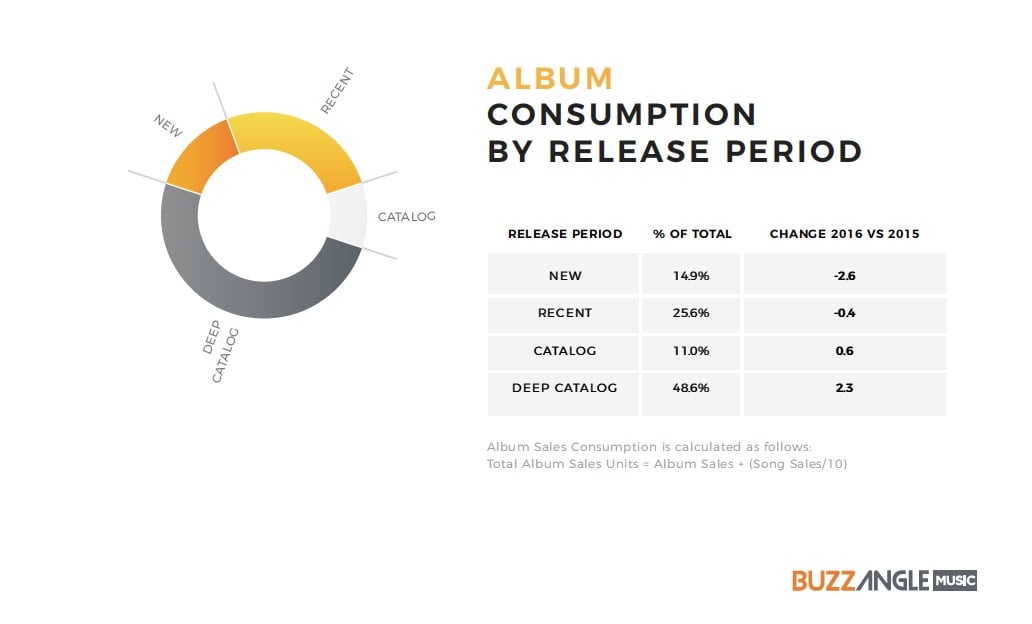

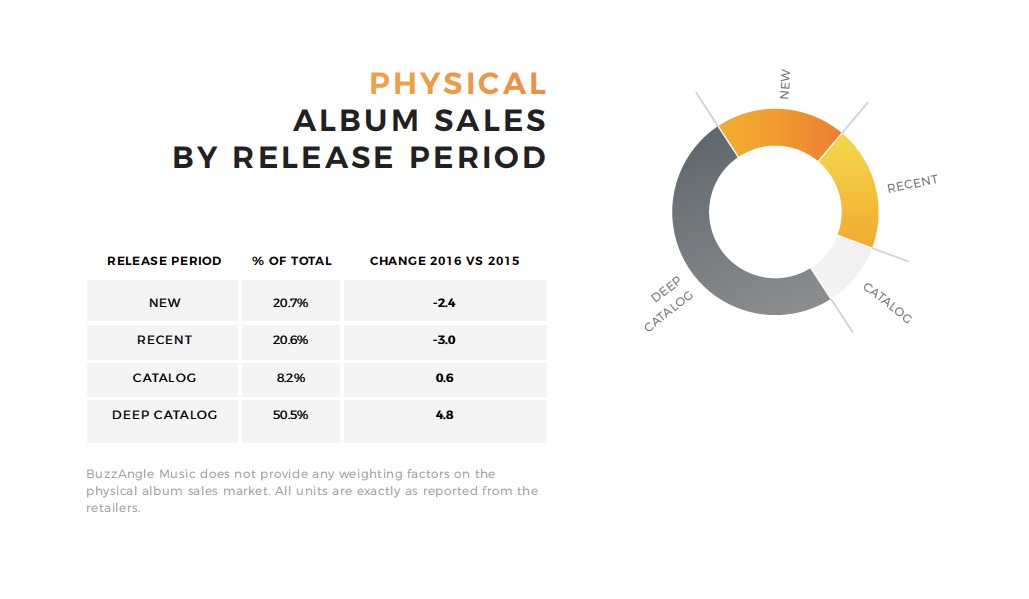

First, the small print: BuzzAngle counts ‘catalogue’ as anything over 78 weeks old. It further segments out ‘deep catalogue’, which it considers music released over 156 weeks (or three years) ago.

According to BuzzAngle’s data, total US music consumption last year – across digital and physical LP sales, plus track download and streams – was 11% catalogue, with an additional 48.6% ‘deep catalogue’.

Combined, that’s a market share of 59.6%.

What’s more, ‘deep catalogue’ grew its market share across all of the following formats: total consumption, digital albums, digital tracks and physical album sales.

In fact, on physical albums, ‘deep catalogue’ increased its market share by a sizable 4.8%, up to 50.5%.

You start to see why the likes of Concord, BMG and Capitol Music Group have been spending so big on prized catalogues of late (like Capitol with the Bee Gees, pictured).

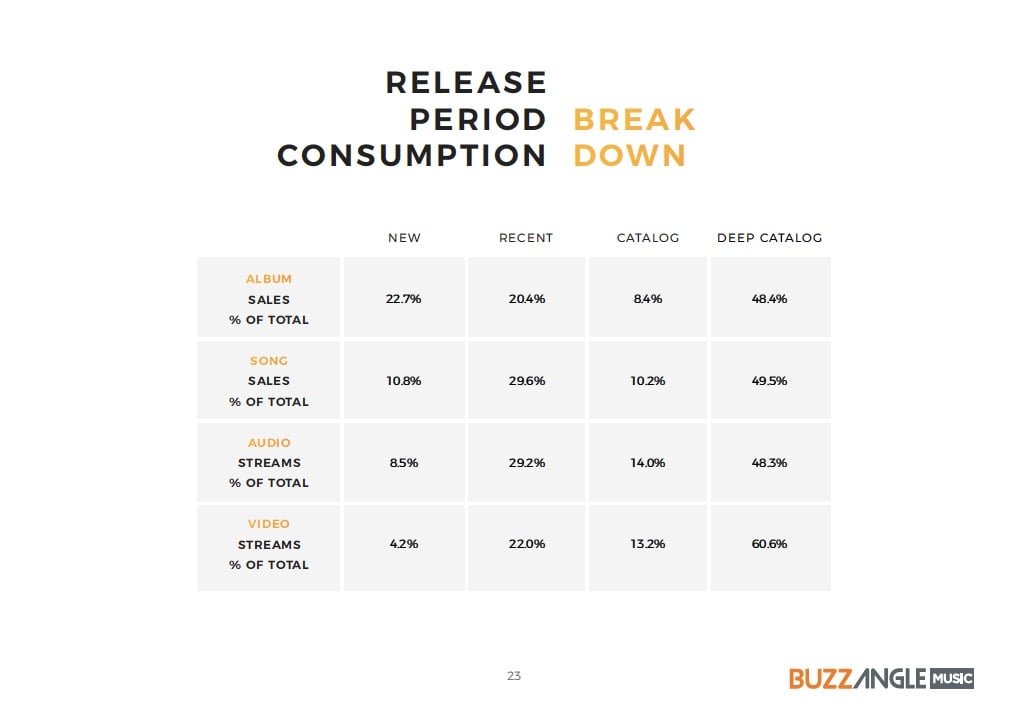

Interestingly, streaming was the only area where catalogue lost market share to newer recordings in the US in 2016 – but not by any greatly significant margin.

According to BuzzAngle, ‘deep catalogue’ took a 48.3% market share of audio on-demand services (-1.8%), while ‘catalogue’ claimed 14% (-1.2%) – jointly taking home a 62.3% market share.

Across the globe, label insiders tell MBW, this combined figure is closer to 70%.

BuzzAngle’s figures also cover video streams in the US last year – inclusive of both ‘premium’ YouTube music videos and tracks used on user-generated content.

Here ‘deep catalogue’ tracks claimed 60.6% of all plays, with ‘catalogue’ on 13.2% – a market share total of 73.8%, or nearly three-quarters of all plays, for ‘old’ music.

Some important caveats: ‘deep catalogue’, remember, is any music which is 3+ years old.

The image of The Bee Gees, The Beatles and James Brown etc. which this description may conjure is therefore likely to be a bit misleading. (Consider that modern superstar artists in Spotify’s Top Ten most-played acts in history – including Drake, Ed Sheeran, Rihanna, Calvin Harris and Sia – were all releasing big albums in this period.)

Yet these figures certainly challenge the idea of ‘Spotify Records’ significantly reducing pay-out to the major labels by the streaming platform.

The majors love owning catalogue not only because it’s a banker in terms of market dominance, but also – as Warner Music Group’s quarterly earnings filing attests- “sale of [catalogue] material is typically more profitable than that of new releases, given lower development costs and more limited marketing costs”.

Even with runaway successes, doing battle with labels in the world of frontline A&R is only ever going to mean paddling in the shallow end of the entire commercial music business.

If Daniel Ek really wanted to scare the major record companies, he should set his sights on stealing premium catalogues from years gone by.

That would really put the cat amongst the pigeons – so long as Spotify has the money, that is.

Word of warning: in a growing music business, ‘deep catalogue’ inevitably requires ‘deep pockets’.