There have been a lot of eyes on Hipgnosis Songs Fund (HSF) this year. The UK-listed fund, once the most active acquisitive entity in music rights, has paused its buying of catalogs over the past 12 months, and hasn’t raised any new share capital for rights buyouts during this period.

HSF’s financial results, therefore, give us a handy indication of the organic strength of the company’s catalog, which covers rights/income streams in 65,413 songs, according to company documents.

Today (December 8), HSF has announced its half-year results for the six months to end of September 2022, with a number of positive signs, both for HSF investors and for the music rights business at large.

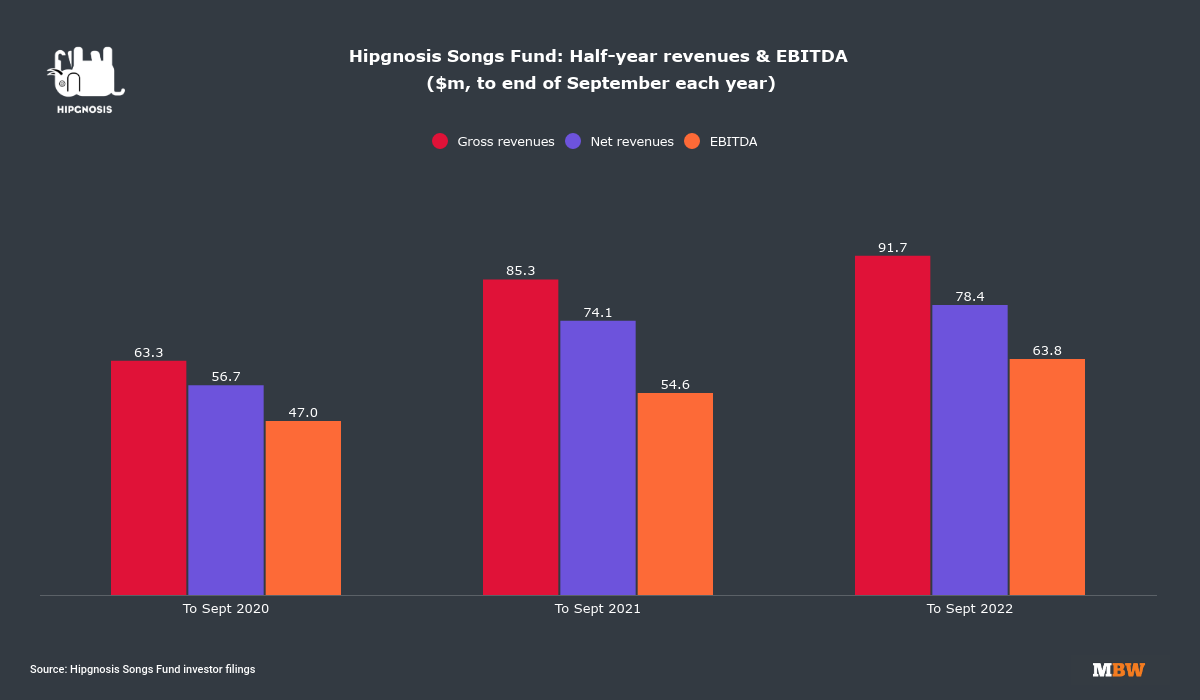

Gross revenue at HSF stood at USD $91.7 million in the six-month period, up 7.5% YoY on the $85.3 million generated in the equivalent prior year period.

Net revenue of $78.4 million increased by 5.8% year-on-year (six months ended 30 September 2021: $74.1 million), after royalty cost deductions of $13.3 million.

Stripping out adjustments such as RTI [‘Right To Income’ accounting] plus a one-time retroactive payment for the CRB III decision in the US, said HSF, shows that its underlying net revenue also grew 5.8% YoY in the 2022 half-year period to $65.1 million.

Half-year EBITDA increased 16.9% YoY to $63.8 million (six months to 30 September 2021: $54.6 million) due to growth in revenue and reduced operating costs.

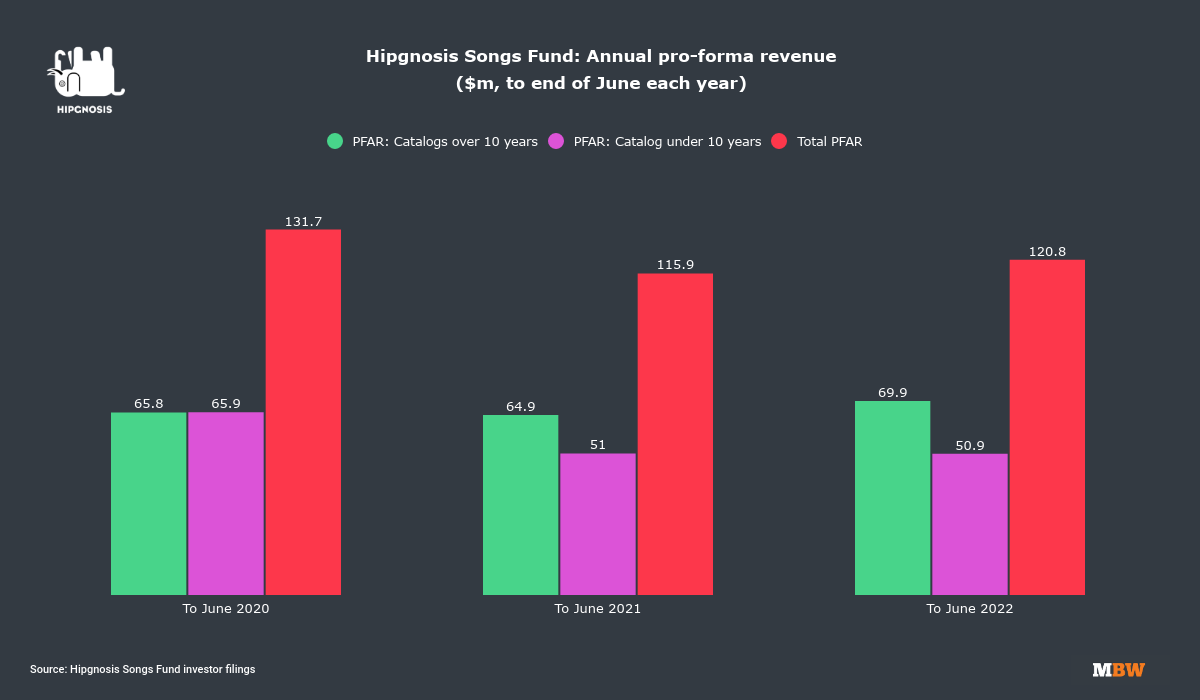

One important metric published by Hipgnosis Songs Fund is its Pro-Forma Annual Revenue (PFAR), which specifically shows royalty revenue earned in a given period.

HSF’s PFAR figure has recently attracted scrutiny from some quarters because it fell slightly YoY in calendar 2021.

That raised questions about the commercial durability of HSF’s acquired catalog. But the company blamed this decline on the impact of Covid-19 lockdowns on HSF’s performance income (from concerts, plus music played in restaurants, bars etc.), and the fact that collections of this income can take anywhere up to 12-18 months to ‘wash through’ to a music rightsholder via the global PRO system.

Somewhat vindicating that argument from HSF, today the company revealed that its PFAR in the 12 months to end of June 2022 switched back into growth – increasing 4.2% YoY to USD $120.8 million, “despite currency headwinds as a result of dollar strength impacting the value of non-US dollar denominated source income”.

The PFAR of catalogs over 10 years old at HSF grew 7.7% YoY in this period (12 months to end of June 2022) to $69.9 million, while the PFAR of catalogs less than 10 years old were flat YoY at $50.9 million (see chart below).

HSF explained to investors today why it felt this under/over-10-year breakdown is so important. Catalogs over a decade old, it reasons, should be growing year-on-year as streaming subscriptions continue to increase.

But catalogs under 10 years old are usually expected to undergo a ‘decay curve’ whereby they are losing popularity from the peak of their release-year ubiquity.

HSF is proud that revenues from its catalogs younger than 10 years are now flat year-on-year – evidence, it suggests, that it’s been picking the right acquisition targets for long-term value.

Said Hipgnosis founder, Merck Mercuriadis: “Our younger catalogs continue to demonstrate that they are reaching the end of their forecasted decay curves and we have particularly focused on synch opportunities where the expected life cycle of a catalog means that it moves on from ‘new music’ radio stations, but is not yet mature enough for ‘Gold’ stations.”

Speaking of synch, Hipgnosis Songs Fund’s catalog saw a 32.0% YoY rise in synch revenues in the six months to end of September (fiscal H1 2022), up to $9.78 million.

Mercuriadis attributed that rise to “the tireless efforts of [Hipgnosis’] synch team to get songs placed into adverts, television shows, films and video games alongside new revenues from emerging platforms such as TikTok”.

There was also a substantial rise in the six months to end of September for HSF’s streaming revenues, which rose 15.8% YoY to $23.6 million (fiscal H1 2021: $20.4 million).

HSF’s overall PFAR in the six months to end of September 2022, said Mercuriadis, was up 7.8% YoY to $58.5 million.

These figures pleased JP Morgan, which said of HSF’s latest results this morning: “Underlying H1 income is ahead of [JPM’s expection], with a strong performance from streaming and synch, though currency has been a bigger headwind than we expected, and the underlying portfolio valuation is broadly flat”.

Added the JP Morgan note: “We remain optimistic about the asset class, which benefits from the structural growth of paid music streaming subscriptions, and we think SONG offers an attractive mix of a high current dividend yield (6.6%) and strong capital growth potential from the underlying assets combined with potential for a narrower discount.”

“Underlying H1 income is ahead of [JPM’s expection], with a strong performance from streaming and synch, though currency has been a bigger headwind than we expected… We remain optimistic about the asset class.”

JP Morgan research note on HSF published today

HSF has continually informed its investors that acquisitions at its company are – for the time being – being halted amidst a difficult set of macroeconomic conditions.

(Hipgnosis Songs Capital, a separate and private fund in partnership with Blackstone, has been spending this year: It’s splashed over $300 million buying catalogs in 2022 from the likes of Justin Timberlake and the Leonard Cohen estate).

However, Hipgnosis has raised a little bit more debt this year, having locked in a new USD $700 million revolving credit facility (RCF) in October, which brought with it stable interest rates. (Around $600 million of debt was already fully leveraged at Hipgnosis prior to this RCF being secured; it effectively added $100 million of spending power to the company.)

Following a series of share buybacks since that debt raise, Hipgnosis Songs Fund today confirmed that it was sticking with its plan to pay shareholders a target dividend at 5.25p per Ordinary Share for the financial year 2022-23.

Hipgnosis also told investors today that Citrin Cooperman had carried out a valuation of HSF’s catalog at the end of September, landing on an “aggregate fair value of $2.67 billion… in line with the prior year”. That valuation was calculated using an 8.5% discount rate.

HSF further explained that HSF’s board, at some point in the prior year, “appointed Kroll Advisory Limited (“Kroll”), an independent valuation firm, to consider and advise on the reasonableness of certain assumptions commonly employed in the valuation of music Catalogues based on data provided by the Company…. the results of the analyses by Kroll provide, in the Board’s view, additional support as to the reasonableness of assumptions employed in arriving at the Fair Value of the investments”.

Merck Mercuriadis (pictured inset) wrote a comprehensive take on Hipgnosis Songs Fund’s half-year performance within the firm’s HY report today, which you can read in full below.

In a very challenging environment, I’m proud that in our work to establish Songs as an asset class, everything we have told our investors from IPO has either become reality as stated or been exceeded. That includes the growth of streaming, our ability to establish Song Management as a new paradigm and manage the Songs better to add value, bringing efficiencies to revenue collection, advocating on behalf of songwriters to get a bigger slice of the pie and making Hipgnosis the preferred buyer of the songwriting community, enabling us to acquire well.

This strategy has delivered a Total $ NAV Return to Shareholders as at 30 September 2022 of 11.8% per year, 60.0% in aggregate since the IPO on 11 July 2018 (including 19.0p per share of dividends).

Our thesis has always been that Songs of extraordinary success and cultural importance produce long-term and reliable income streams, making them highly investable assets.

We built Hipgnosis Songs Fund as an asset-backed investment vehicle with iconic Songs at its heart to deliver value for our Shareholders off the back of this thesis.

We therefore assembled a Portfolio of Songs that is unrivalled for its extraordinary success and cultural importance and which are in high demand. It is a generally accepted theory that most music companies make their money on 10% of their Songs. I’m confident that our Catalogue would represent the top 10% of any music company’s portfolio.

“In a high inflation environment, it is arguable that there is no better value than c.£/$10 per month for a premium music streaming subscription service.”

We demonstrate this by co-owning nearly a quarter of the Songs in the “Spotify Billions Club” (Songs streamed over a billion times on Spotify) and over 10% of Rolling Stone’s The 500 Greatest Songs Of All Time.

Only last month, the Official Chart Company, on behalf of the BBC, identified the most streamed Songs released in each of the last 70 years. Hipgnosis co-owns rights to nine of these. Songs like Don’t Stop Believin’ (Journey, 1981); Sweet Dreams (Are Made Of This) (Eurythmics, 1983); Livin’ On A Prayer (Bon Jovi, 1986); and Everywhere (Fleetwood Mac, 1988). You are likely humming at least one of those Songs as you read this paragraph.

Some of you will hopefully go onto Spotify, Apple Music or YouTube today to hear these Songs. Others will be prompted to add them to a playlist. Many, many more will have done so when the BBC played them all to celebrate its 100th anniversary. Each time this happens a payment is earned by Hipgnosis Songs Fund.

Importantly, people continue to listen to and pay for music irrespective of the challenges of today’s macro-economic conditions. We often say that when people are living their best lives they are doing so to a soundtrack of great Songs. Equally, when they are experiencing life’s challenges, they are taking comfort and escaping with great Songs. Either way, our iconic Songs are being consumed and are generating revenue.

Indeed, recently published research from the IFPI, who represent the global record industry, shows that people around the world are engaging with music in 2022 more than ever, with average listening up to 20.1 hours each week – an increase of 1.7 hours since 2021.

According to Luminate, as of 26 November, music audio streams in the United States are now over the one trillion mark for the first time ever in a single year. That’s already an increase of 11.9 billion compared to the previous year. It is also seven times higher than in 2015. This report also included the Top 5 most streamed Songs of the year so far; At No.2, Glass Animals’ Heat Waves generated 493 million on-demand US audio streams. This is administered by Hipgnosis Song Group (HSG) in the US. That’s the second most streamed Song of the year in the world’s biggest paying market.

In a high inflation environment, it is arguable that there is no better value than c.£/$10 per month for a premium music streaming subscription service.

Paid for streaming – and its utility-like revenues – continues to grow with more than 523 million premium paid subscribers globally. In recent months, we have seen Spotify Premium Subscribers reach 195 million, a 13% increase year-on-year despite the macro-economic environment. Looking at the wider music market, the RIAA reported US revenues for recorded music in the first half of 2022 rising 9.1% year-on-year. Apple Music has recently increased prices beyond the 9.99 per month price point in the US, UK and continental Europe. This emphasises the incredible value that music streaming represents and shows that one of the most commercially successful businesses in the world recognises the pricing power that great music gives their platform. We expect other streaming platforms will follow Apple‘s move. Increased revenue to the Digital Service Providers means increased revenues for Hipgnosis.

We promised investors that we would deliver a new, responsible approach to Song Management, one where we have the resource and bandwidth to manage our great Songs to their full potential – and in doing so add significant value.

All the Small Things performed by Blink-182 reached Number six in the Billboard Hot 100 and Number two in the UK on release in 2000. This Christmas, it’s almost impossible for anyone in the UK not to be familiar with a new version which is the soundtrack to the seasonal ritual that is the John Lewis Christmas advert. This is a great example of our approach in action – our Synch team saw the potential of the Song and took it to John Lewis, then did everything they could to make it as efficient as possible for them to choose and use our Song.

“The results we publish today show the strength of our Portfolio.”

Along with the Superbowl, the John Lewis Christmas advert is arguably the most coveted synch in the world. In our early days of meeting potential investors we promised we would procure this and we have delivered as we said we would.

The results we publish today show the strength of our Portfolio.

Gross revenue in the period increased by 7.5% year-on-year to $91.7 million (six months to 30 September 2021: $85.3 million), while our Operative Net Asset Value per share remained steady at $1.8312 (31 March 2022: $1.8491). When translated into GBP, at a Sterling to Dollar exchange rate of $1.2223, our Shareholders benefitted from the strong dollar, with an equivalent GBP NAV of 149.82p as at 6 December 2022 (31 March 2022: 140.79p).

Like-for-like pro forma (PFAR) revenues in the first half of the calendar year were $58.5 million, a 7.8% increase on the comparative period in 2021.

Our PFAR shows that our Streaming performance is strong, up 15.8% to $23.6 million (H1 2021: $20.4 million) – while the tireless efforts of the Synch team to get Songs placed into adverts, television shows, films and video games alongside new revenues from emerging platforms such as TikTok, have resulted in Synch revenue growing by some 32.0% year-on-year to $9.78 million (H1 2021: $7.41 million) year-on-year.

Our younger Catalogues continue to demonstrate that they are reaching the end of their forecasted decay curves and we have particularly focused on Synch opportunities where the expected life cycle of a Catalogue means that it moves on from “new music” radio stations, but is not yet mature enough for “Gold” stations.

Data from the US, shows that vintage music is an ever increasing proportion of consumed music – now making up three quarters of Songs enjoyed, up from a little over a half in 2017. In part, this is due to the consumer being able to choose what they want to listen to on demand. We are also seeing the positive impact of older demographics adopting paid streaming and Songs boosted through strategic Synch and Playlist placements. This reminds people of great Songs they can now listen to at will. Last year, we had four Songs that were released prior to 2010 in the Spotify Billions Club; this year we have 11!

The Song is the currency of our business; without the Song we simply have no music industry. Yet for too long the songwriter – who delivers the most important component to the success of a record company, digital service provider, music merchandiser or live promoter – is the lowest paid person in the economic equation.

I have always been clear that our motive is to establish Songs as an asset class and to provide a great return for our investors. Concurrently our “ulterior” motive is to use our success to help take the songwriter from the bottom to the top of the economic equation. We advocated for, and welcome the moves by the US Copyright Royalty Board (CRB) and the wider music industry in the US to increase the rates paid to songwriters and publishers. CRB III provided for a 44% increase in the headline rate of DSP revenues paid to songwriters and Publishers, reaching 15.1% in 2022. The joint industry proposals for CRB IV would see that proportion rising incrementally to 15.35% in 2027, while the royalty payable on a physical sale or download would rise from 9.1 cents to 12 cents with additional inflationary increases.

There is still a long way to go before songwriters are fairly remunerated, but these are important steps in the right direction. The joint CRB IV proposals show there is increasing acceptance – as a result of our work – across the music industry that songwriters should be fairly rewarded for their work. Whilst the increase is more modest than the CRB III rises, we support it as it will provide a background of stability at the highest streaming rates ever paid in the context of which we can continue our advocacy efforts. Our ultimate goal is for songwriters’ pay to be determined by the free market, not legislation.

When a Catalogue is acquired, our Shareholders sit directly in the shoes of the songwriter so there is complete alignment between the songwriting community and our Shareholders. What is in the best interest of the songwriter is also in the best interest of the Company.

Despite our successes, I share the disappointment of Shareholders that the true value of our iconic Songs is not reflected in today’s share price. As Songs are a new asset class, we understand that the market has concerns about both valuation and discount rate, particularly when our NAV is stable in a macroeconomic environment in which the value of many other assets are declining.

It’s important to remember that the music industry went through a prolonged period of decline for 15 years, between 2001 and 2016, when technological disruption in the form of illegal downloading almost killed it off. The only good thing to come out of that era is that it left these great Song assets at attractive prices, just as the technology evolved into streaming, which made it more convenient for consumers to once again listen to and pay for music legally.

We started buying assets in 2018 when paid US music streaming subscribers were less than 10% of the 523 million global subscribers there are today. YouTube had barely paid $2 billion to rights holders in 2018 compared to the $6 billion it has paid in 2022. Whereas previously, almost all consumption of music was unpaid for, today, almost all consumption of music is paid for and music has changed from a discretionary purchase to a utility.

These are all positive factors in our NAV.

As a result of our success in establishing Songs as an asset class, we are flattered that many other investors have come into the market.

“Despite our successes, I share the disappointment of Shareholders that the true value of our iconic Songs is not reflected in today’s share price.”

While Hipgnosis Songs Fund is currently fully invested, Hipgnosis Song Management (HSM) remains active in the market, which gives us access to incredible amounts of transactional data and first-hand knowledge of this growing marketplace. This information is shared with the Hipgnosis Songs Fund Board who, as a result of the robust co-investment policy between Hipgnosis Song Management and its clients, sees everything that HSM sees.

Many Private Equity funds, some of the most successful long-term investors in the world, are today making high-profile Catalogue purchases at multiples that reinforce the Fair Value of our Portfolio and reassure us that we have bought well.

The Fair Value of the Portfolio was calculated by the Portfolio Independent Valuer, Citrin Cooperman, at $2.67 billion, in line with the prior year. They have a team of leading experts in music valuation who have been involved in many recent high profile music catalogue purchases. For the current NAV, they have continued to use a discount rate of 8.5%. This Fair Value enables us to calculate the Operative NAV which remained stable at $2.2 billion. To provide investors reassurance, the Board also appointed Kroll Advisory Limited (“Kroll”), an independent valuation firm, to consider and advise on the reasonableness of certain assumptions commonly employed in the valuation of music Catalogues based on data provided by the Company. The results of the analyses by Kroll provide, in the Board’s view, additional support as to the reasonableness of assumptions employed in arriving at the Fair Value of the investments. This gives us, and should give investors, great comfort over the Fair Value of our Songs and therefore the incredible investment opportunity the current share price represents.

An increase in the discount rate from 8.5% to 9.0% would reduce the Operative NAV by $212 million. Our current share price is trading at a discount to the Operative NAV of over 45%, which implies a discount rate of nearly 12%. There is considerable upside.

We go into the second half of the year positioned strongly. Our re-financed Revolving Credit Facility, interest rate hedges and currency hedges for our Sterling dividend payments, finalised post period end, give increased certainty on costs, while the recent confirmation from CRB that it will enforce the increase in revenues from US streaming, as proposed in its CRB III settlement, is further boosting revenue. Additionally, the return of Performance revenues to pre-COVID-19 levels is yet to be seen in our revenues.

The statistics continually demonstrate the importance of Music in all of our lives as a great and affordable source of comfort, nourishment, sustenance and joy. I’m delighted that it is Songs owned by Hipgnosis that people are listening to and that are amongst the most consumed Songs throughout the world.

You are pioneers in establishing an exciting new asset class and we do not take your belief in the Company lightly. We therefore take our responsibility to you, our Shareholders, very seriously. I therefore hope that the information we are sharing in these results will give you belief in our Fair Value and we are firmly committed to ensuring that the Company’s incredible value is recognised in the market.

I would like to pay tribute to the incomparable Christine McVie who passed away last week at the age of 79. She wrote iconic songs that propelled Fleetwood Mac into one of the biggest artists of all time. She was our Songbird and it’s one of Hipgnosis’ greatest privileges to forever be the custodians of her special songs. It is clear from the live chart data that millions of people are streaming her hits with Fleetwood Mac’s Rumours having already returned to the Top 10.

“You are pioneers in establishing an exciting new asset class and we do not take your belief in the Company lightly.”

This week Mariah Carey’s All I Want For Christmas Is You is heading for the UK Number One slot and is already Number One on the Billboard Global 200 chart. Meanwhile, Michael Buble’s Christmas Album is set to be back in to the Top 10, Hipgnosis Songs Fund has an interest in both and there’s another three weeks to go before the big day. The Company has co-owned All I Want For Christmas Is You since 2020, one of the seasonal greats. In our first full year of ownership we saw a 78% increase in revenues compared to the average of previous three years – buying well, proactive Song Management and strong market growth delivering once again. Further to this Fleetwood Mac’s Rumours is back in the Top 10 UK album chart and Heat Waves by Glass Animals has just been named Billboard’s Number 1 Hot 100 song of the year.

It remains only for me to thank you for your support as well as that of the incredible songwriters that have entrusted us with their iconic work.

Wishing you, and your loved ones, all the best for a Merry Christmas, wonderful holidays and a happy, healthy and prosperous 2023!

Music Business Worldwide