MBW Views is a series of exclusive op/eds from eminent music industry people… with something to say. The following comes from Annabella Coldrick, Chief Executive of the UK-based Music Managers Forum.

During my recent conversations with music managers two of the main issues that come up (beyond the tough but rewarding business of investing in and partnering with artists), are the impacts and implications of Artificial Intelligence, and an urgency to reform how streaming revenues are distributed.

Interestingly, the two issues have become increasingly conflated.

In recent months, the major labels have all presented concerns about AI running rampant, and fears that investment-heavy, human-created music will soon be pitted for survival against a sluice of low-value generative ‘content’.

These concerns are probably justifiable.

If 120,000 tracks are already uploaded daily to streaming services, and if the majority of those tracks are barely listened to (or not listened to at all), and fraud is rife, then just imagine when the AI-farms start churning out copycat versions of current hits.

High-value repertoire could be lost in a sea of what Sony Music CEO Rob Stringer describes as “flotsam and jetsam”.

For UMG’s Chair & CEO, Sir Lucian Grainge, the antidote is to deliver a new kind of revenue distribution model – an “artist-centric” model – that delivers a greater share of the pie back to high-quality music at the top of the listening pyramid.

In the IFPI’s recent 2023 Global Music Report, Sir Lucian writes: “As we enter our industry’s next exciting chapter, we must remain focussed on our shared goal: a robust, growing and sustainable music ecosystem. This is an environment in which great music is not drowned out by an ocean of noise, where music is easily and clearly accessible for fans to discover and enjoy, and an environment in which the creators of all music content – whether in the form of audio or short-form video – are fairly compensated and can therefore thrive for decades to come.”

Picking up on the theme, last month, Warner Music Group CEO, Robert Kyncl, also questioned why high-value music content wasn’t rewarded with a greater share of streaming revenues. “It can’t be that an Ed Sheeran stream is worth exactly the same as a stream of rain falling on the roof,” he said, describing the current dominant music streaming royalty model – the ‘label-centric’ model effectively created by the industry – as “misaligned”.

These developments, while highly significant, also represent a clear change of direction by the majors.

In the UK, we’re still in the midst of an industry-wide process to make music streaming more equitable and transparent – and particularly so for artists, songwriters, producers and musicians.

While some progressive record labels and music publishers have made welcome concessions to reform, the prevailing tone from rightsholders representatives has been to leave the boat unrocked.

Streaming is delivering growth, they say. Any tinkering with the current model would have unforeseen consequences and could reduce investment. Their favoured course of action is to retain the status quo.

“Rather than pointless infighting, the music business should unite instead and grow the pie.”

Rather than pointless infighting, the music business should unite instead and “grow the pie”.

That message is palpably different to the ones now being delivered by the labels themselves. From the heads of the majors, there is widespread consensus that the way in which streaming revenues are distributed needs urgent reform.

From the perspective of the MMF – and the artists, songwriters, producers that our members represent – we couldn’t agree more.

However, concerns about protecting and remunerating artists and songwriters against the flotsam and jetsam of AI bots and hobbyists would suggest that the music on streaming services is already treated equally. To paraphrase Robert Kyncyl, that a globally successful artist like Ed Sheeran is being paid at the same rate as someone releasing the sound of rain water.

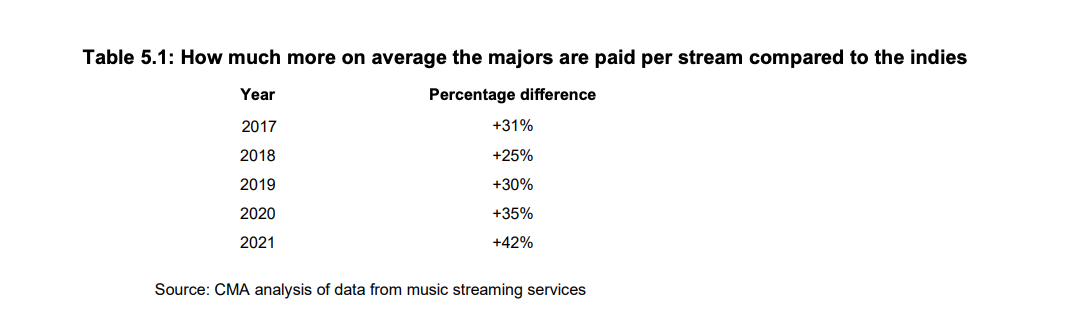

But there is a potential flaw with this prognosis. Because according to the UK’s Competition & Markets Authority, there is currently a vast disparity in how much revenue is paid per stream to different rights holders. And the disparity is growing.

Buried deep in the CMA’s intensive 2022 study of the UK streaming market (or, more specifically page 111, Table 5.1) is a remarkable data table, which estimates the majors are already receiving 42% more per stream for their repertoire than indie labels or DIY artists – up from 25% in 2018.

(This may also help explain the current discontentment of indie label group IMPALA about their own members’ share of the streaming pie.)

The MMF has been attempting to get the above figures verified for the past 6 months.

Some of our members think they sound broadly correct, as do some of the accountants we have spoken to. Nobody else in the recorded music business – either major or indie – appears to have challenged the CMA’s findings.

If true, it means that the majors are currently receiving significantly more revenue per stream than other rights holders. Those concerns about rainmakers appear to be misplaced. And if labels can extract even more of the pie, in the form of “artist-centric” licensing, then surely these existing disparities will become even more pronounced.

That would be a more worrying scenario. It’s also distracting from the handful of market changes that artists, songwriters, composers, musicians and producers actually want to see.

In the UK, these have all been succinctly laid out by the Council of Music Makers in a unified 5-point strategy that we believe would recalibrate the current streaming model, and deliver a far more coherent and future-proofed approach to reform.

These include more root and branch changes, such as modern digital royalty rates for all music-makers (both current and legacy), the ability to revisit and revise outdated contract terms, and ensuring all relevant rights data is uploaded before music is made publicly available.

According to IPO research many of these market interventions are commonplace in other countries (certainly in the US and across the EU) and all are being actively discussed as part of a long-running Government-backed process at the Intellectual Property Office (IPO).

In the past fortnight we have already seen two small, but significant, steps forward to reaching these goals with the announcement of a new industry-wide agreement on music streaming metadata and the establishment of an expert working group to explore solutions around fair pay for creators.

It was especially pleasing to have the ringing endorsement of UK Minister of State, Sir John Whittingdale MP, about this progress, and particularly his statement that the British music industry’s continued success and fair remuneration for existing and future creators are complementary aspirations – not opposing goals as some might allude to.

I certainly hope that the wider music industry recognises the opportunity that’s been presented by the UK Government to address these real issues and that we get constructive engagement in the discussions from all quarters. If we need to tackle the very present AI challenge as a unified industry and speak with one voice, then here is an opportunity to truly align our interests.

A genuine pan-industry approach, where music makers and their representatives are involved in the decision-making, is the only way forward. If everyone agrees that the pie needs to be redistributed, then it’s vital we all have a hand on the carving knife – not just those who, according to the CMA, are already receiving the lion’s share of revenue.

Music Business Worldwide