Earlier this week, MBW reported on news from the Nordics that has re-sparked the debate around “fake artists” on Spotify – a story we’ve been following since way back in 2016.

Subsequent to us publishing that story, an anonymous (and clearly well-informed) MBW reader sent us an email that detailed every angle of what’s going on.

Today (March 30) we publish that email in full. Strap in.

Thanks to MBW for your commitment to covering the music industry and trying to dig out stories where others fail.

I have a pretty extensive background in the music business working for both rightsholders and retailers. For the fear of losing my job I need to remain anonymous; feel free to disregard any of my comments for that reason alone.

But I wanted to provide some context to your article on Spotify’s “fake artists”

1) Background:

First of all, “mood music” is one of the largest growth segments of the music industry. This makes sense because an increasing share of the hundreds of millions of people who pay for these streaming services are not really music fans.

More importantly, since there is no longer any cost to access a single piece of content, music for more niche use cases like meditation, working, reading, studying or putting your baby (or yourself) to sleep are becoming important habits. It turns out, most people have more time in their day for these activities, then for actively looking for and listening to Thom Yorke’s recent single. In fact, most users who come home from work just want “something chill” to listen to and could not be bothered what artists will be part of that session.

On Amazon Music around 70% of all activity is happening on Alexa devices and the vast majority of streams are passive sessions where the user is listening to pre-curated stations or playlists, all made by Amazon since unlike Spotify they do not feature user generated playlists.

Across all streaming services an increasing share of consumption is happening in areas of the product that is entirely controlled by the DSP, because as it turns out, most users prefer easy access to pre-curated experiences vs doing the work of actively finding what to listen to.

Prior to 2016 most of the millions of people who searched for “baby sleep”, “meditation” or “relaxing piano” would find poor quality music, released under search engine optimized pseudonyms. Many of which were already streaming and generating more revenues than significant mainstream pop artists at the time.

2) Major labels are also releasing music by “fake artists”

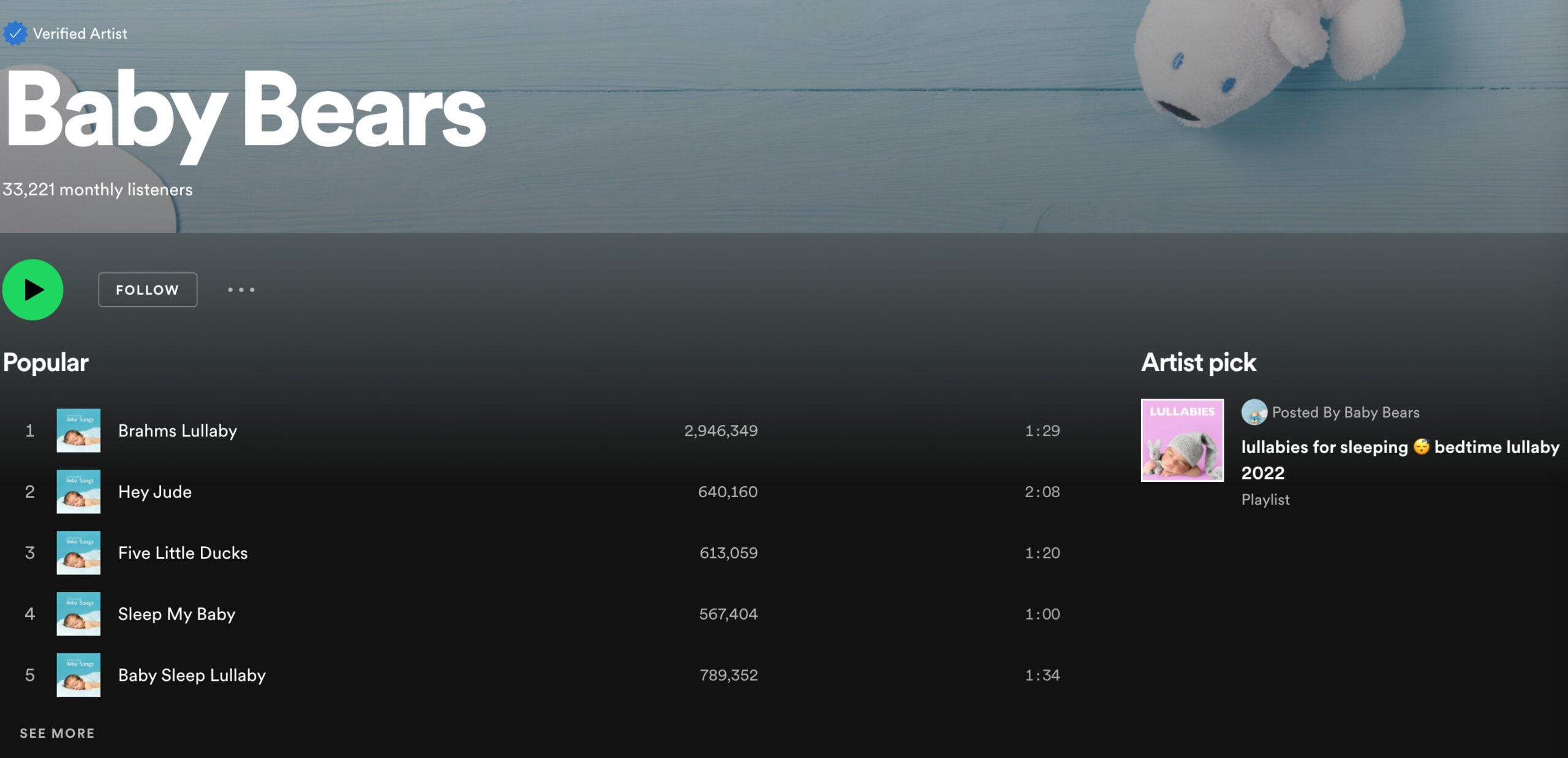

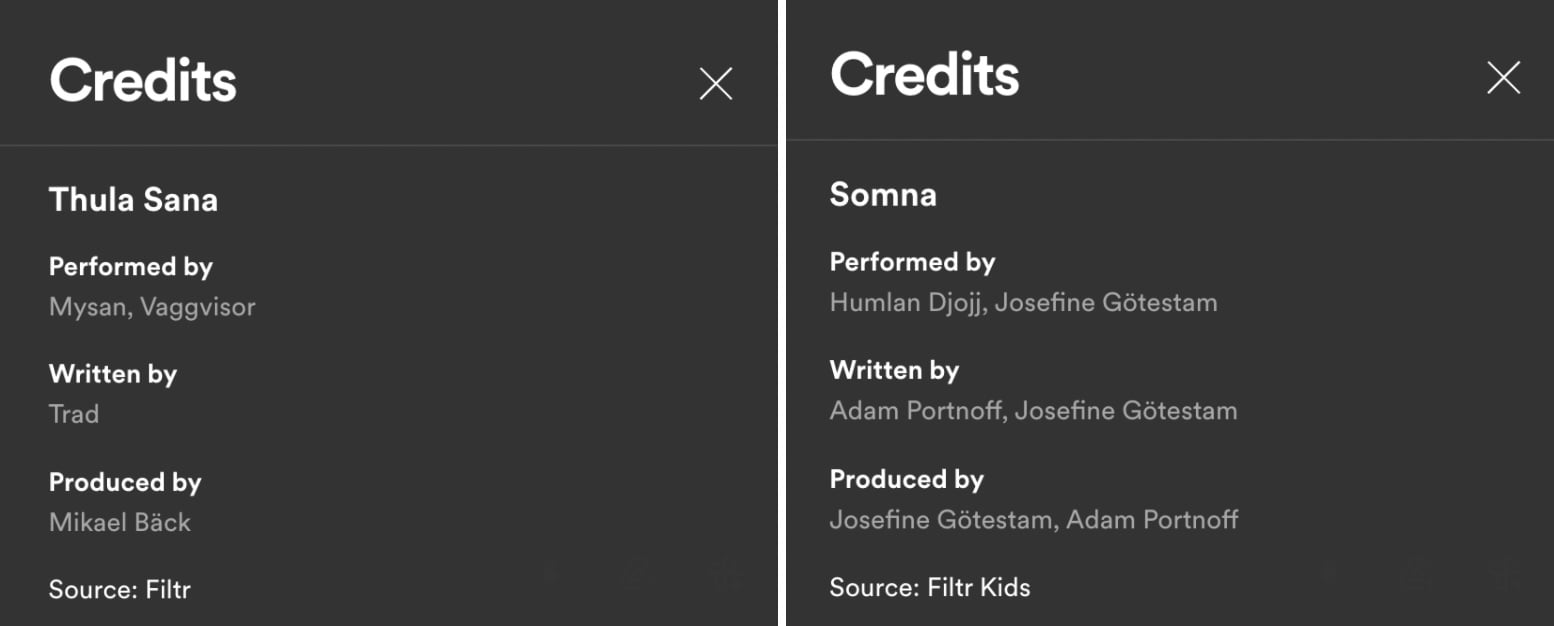

Long before your first article about fake artists in 2016 there was already a huge growth trend in people listening to mostly instrumental “mood music”. Even Sony and Universal Music created playlists for these types of use cases under their Digster and Filtr brands long before Spotify ever did. In fact many majors started releasing music by “fake artists” in the early 2010s and have continued to do so, for example check out these artists that are all Sony-owned with completely generic artist names which all come from the source “Filtr”.

There are hundreds of similar examples if you keep digging, and I should stress, not just by Sony but by all major groups (for example Warner‘s X5 group) and of course by thousands of (mostly low-quality) independent/DIY labels.

Interestingly, all of these “artists” are all discovered on Sony-controlled playlists with very generic search-optimized titles, and millions of followers if you add all the small niche playlists together.

If you look into the songwriter credits of these songs it turns out they are written or produced by writers/producers with names completely different than the search engine-optimized pseudonyms they are releasing music under.

You can imagine that it’s a pretty healthy business for a major label if they can generate significant usage of these releases just by placing them on their own and operated playlist brands (which they have been able to promote freely on streaming platforms thanks to the free ad credits received as part of their agreements with streaming platforms).

Most of these works are “work for hire” where the label has paid a small one time fee for the recordings and then collects the full royalty, but there are also examples where the people behind the pseudonyms are paid a (low) royalty rate.

3) Indies

While majors are invested in this space, there are many extremely profitable and more successful independent companies doing the same.

These players have figured out how to game search on platforms like Spotify, but also YouTube, by creating cleverly named playlists and channels, and promoting them on social media. Their content also features mostly instrumental music by producers and writers releasing under lots of pseudonyms.

The main difference is that they usually combine multiple artist pseudonyms and release hundreds of songs on each profile because this is another way to generate bulk streams via the streaming services algorithms. Strange Fruit for example use combinations of their “artists” Lofi Fruits Music and Chill Fruits Music with a third artist pseudonym, because this generates streaming activity not only via search but also algorithmic programming like Release Radar and Daily Mix on Spotify.

The songwriters and producers of these tracks are either paid a fixed fee per track or a combination of a low advance and reduced royalty rate and it works because these “labels” can guarantee millions of streams through their own network of search engine optimized DSP playlists and YouTube channels.

4) DSPs

So we’ve established that pretty much all significant stakeholders in the industry have identified “mood” or “lifestyle” music as a strategic opportunity. So what are the DSPs approach? First of all, they realized that this is a significant enough segment that it’s worthy of their time and resources. Meaning, a really significant enough share of streams is already being generated by so called “mood content”.

Second, DSPs clearly have an incentive to clean up the poor quality SEO/Fake stream generated content that has been driven by click farms and other semi-fraudulent activity for years. Because, just like with label owned playlists, it turns out that DSPs believe the user experience will improve if they curate their own Hits and Genre playlists as opposed to letting the major labels do the job for them because of their inevitable bias for their own content. It inevitably also gives DSPs leverage because if they control what people listen to, rightsholders will be more dependent on them. Certainly, licensing negotiations in 2022 would be very different if major labels were still the main playlist influencers on platforms like Spotify.

Clearly Spotify, Amazon, Apple, Deezer, Anghami and YouTube feels it is important enough to have their own playlists and channels for things like “Sleep”, “Lofi Beats” and “Relaxing Piano” – because as it turns out, a lot of people love to listen to this music, and just as with Rap or Pop, DSPs feel they know best in terms of which music should be featured in official playlists or radio stations.

Now, DSPS have to pay royalties for every stream that happens on their platforms because the deals with majors are structured in a way so that they cannot compete directly with majors and own their own recordings. But it is of course common knowledge that the major labels are paid a little bit more than large independents and certainly the DIY aggregators that most of the millions of “artists” who release music. So already, DSPs can improve their margins by shifting consumption from expensive major label content to cheaper independent content. As it turns out, shifting consumption from X to Y is a lot easier to do if you control most of the consumption on the platform.

Recently, Spotify announced their Discovery Mode program. This allows labels to discount selected parts of their catalog in return for increased promotion via Radio and Autoplay and provides another way for the DSP to improve their overall profitability (or lack thereof).

It seems obvious at this point that other DSPs will follow, just imagine if Amazon or Google offered a promotions program where you could get your songs distributed to people who ask their Alexas or Google Home for generic requests like “play something chill” or “play party music” in return for a discounted royalty rate.

A label like Epidemic Sound has a different royalty structure altogether (none of their writers are represented by collecting societies) which enables them to offer more “creative” pricing for combined master and publishing rights. A consequence for that could of course be that while they might potentially earn less than their competitors per stream, DSPs are effectively reducing their royalty costs every time their content is consumed.

This doesn’t mean DSPs are going to put Epidemic Sound tracks in their biggest playlists or promote them widely to all users, because whatever slight margin improvement would never be worth disrupting the user experience. But if Epidemic and others like them can create lofi beats or ambient music that is at least on par with what other labels in that category are delivering, there is of course incentive to feature them more.

Make no mistake, all DSPs are engaging in the above. Spotify is taking more heat because they are the largest and most transparent, whereas Apple, Amazon, Deezer and Tencent makes it much more difficult for journalists like yourself to see what is happening since there are no stream counts, writer or even label credits.

These days there are hundreds of companies like Firefly of different sizes. Firefly and Epidemic are in the spotlight because they were early entrants and among the bigger ones based on market share, but mostly because they insist on using their label name in the p/c line and feature the same composers on many different works whereas others simply use the artist as the label name.

The reality is this market is becoming a real part of the music industry and more established investors and label groups are starting to look at buying into the space. I am confident that in 5 years majors will have VPs of “Lifestyle Music” etc because inevitably they cannot afford to stay on the sidelines in their effort to protect their declining market share as they represent a smaller and smaller fraction of releases every week.

Just recently Universal has started releasing lo-fi beats music under the artist alias uChill putting out lo-fi remakes of UMG catalog tracks at bulk which is an indicator that majors are starting to realize there is a real market here.

5) The fake artists

At the end of the day, fake artists are of course real songwriters, instrumentalists and music producers with varying degrees of talent.

These are people who have always tried to find ways to make a living off their music, you might be a pianist or guitarist who is used as a work-for-hire by bigger artists and paid a fee per hour, per track or live show. You might be a somewhat successful pop producer or songwriter with a decent cut rate even working with big artists.

You might be a promising bedroom electronic/hiphop producer who did a remix once for Deadmau5 or a successful touring electronic DJ getting into your 40s and starting to think about the next step. You might be writing tracks for K-pop acts knowing that usually about 10% of them gets picked up by an artist or label and actually starts generating royalties for you a year or two later.

Regardless of who you are, you are always going to be looking for new ways to make ends meet. And you probably are not primarily driven by becoming an “artist” or having a career playing live.

For these people, whether you are offered to make tracks for one of the majors’ secret mood music projects, by labels like Strange Fruits or by Firefly, they are all probably viable ways of making a buck. In fact, many of these people are doing not just one but multiple of these. And are probably better off as a result of it, because it gives them flexibility (without being locked to an exclusive label or publishing deal) and the ability to benchmark different ways of making a living off your talent as a musician.

One perspective here is that many musicians in this category are among the most fucked over in terms of the share of revenues they have received from their work in the past.

Finally. While it is easy to find labels, writers and producers who have fake artist pseudonyms with millions of streams, there are also tens of thousands of releases that have very unimpressive numbers and there are not really any guarantees that your track is going to do well. And if you decide to partner with labels who are great at gaming algorithms and search, there is of course the very apparent risk that your streams will quickly go down to zero once DSPs optimize their services to mitigate these exploits.

So who’s really losing in this equation?

Possibly, older out of touch-artists who think music should always be something meaningful and “culturally important” and are perhaps – just slightly – butthurt that no one cares, or that other people have figured out another way to be successful.

Perhaps major labels who are a bit late in the game and will likely have to acquire smaller labels to start competing (just like when Warner acquired Topsify when they realized UMG and Sony were way ahead in the label owned playlist-race).

And like you have pointed out in your articles, certainly Swedish labels and creators have benefitted more than their peers from other countries. This is perhaps not reflective of the current situation, there are certainly loads of non-Scandinavian companies growing rapidly in this segment, and others that are investing their way into the space, but this entire category (just like label playlisting, playlist apps and well, streaming in general) clearly over-index towards the Nordics because it’s where it all began. This was also true for mainstream Swedish EDM and pop acts that grew to global fame because of the Nordics relative impact over the global streaming charts at the time, but will get “fixed” over time.

It’s not a coincidence that there have been no new Kygos, Aviciis or Swedish House mafias in the last 5 years. After all, all the Heads of Content at all the main DSPs are American so I am sure that eventually we will go back to the normalcy of North American dominance 😉

It’s certainly an interesting time to be alive in the industry 🙂 For me personally, Discovery Mode and similar promotional schemes are perhaps more controversial than the mood music space because it presents a viable threat – or opportunity – depending on which side you’re on, to really change the way pricing works in the streaming era. It is after all, an anomaly that all music is monetized at the same rate and it seems inevitable that rights holders will start to discount parts of their catalogue in return for more visibility as they always have in the best whether it was via discounted iTunes albums, CDs or compilations.

Major labels have an inclination to give away their content for free if they believe it can grow their market share and naively believe they will benefit because of course in the end the real winner is the DSP who don’t care who ends up with more market share as long as their overall royalty rates are moving down. Hoping to read more about your perspective on this topic in the future.

Best of luck,

Anonymous MBW reader

MBW offers a right to reply to anyone referenced – or who feels referenced! – in the above article. Please contact us either officially or anonymously at enquiries@musicbizworldwide.com

UPDATE: A previous version of this article referenced Sweden-based LoudKult Records. Within this section of the article, MBW’s anonymous reader suggested that some independent labels were using “click farms and bots to increase the search visibility for their content”.

MBW would like to make it clear that we have seen no evidence linking LoudKult to the use of click farms, and retract any suggestion in the article that the company may have done so.Music Business Worldwide