Recent weeks have brought with them big news for the independent sector of the recorded music industry: overall indie market share of the IFPI-measured $17.3bn global market last year was bigger than any other party. Below, Alison Wenham (pictured) – CEO of the Worldwide Independent Network – responds to the figures…

Is this a tipping point? Is the genie out of the bottle for the music industry?

The global music industry has a lot to be upbeat about after the release of two major reports confirmed a sharp upturn in revenues from recorded music over the last twelve months.

Midia/Mark Mulligan’s ‘Recorded Music Market 2017’ report and The IFPI’s ‘Global Music Report 2018’ both conclude that for the first time in many years recorded music revenues are experiencing sharp growth – and the distribution end of the value chain is both vibrant and competitive.

Global recorded music revenues are up 8.1% to $17.3 billion, says the IFPI.

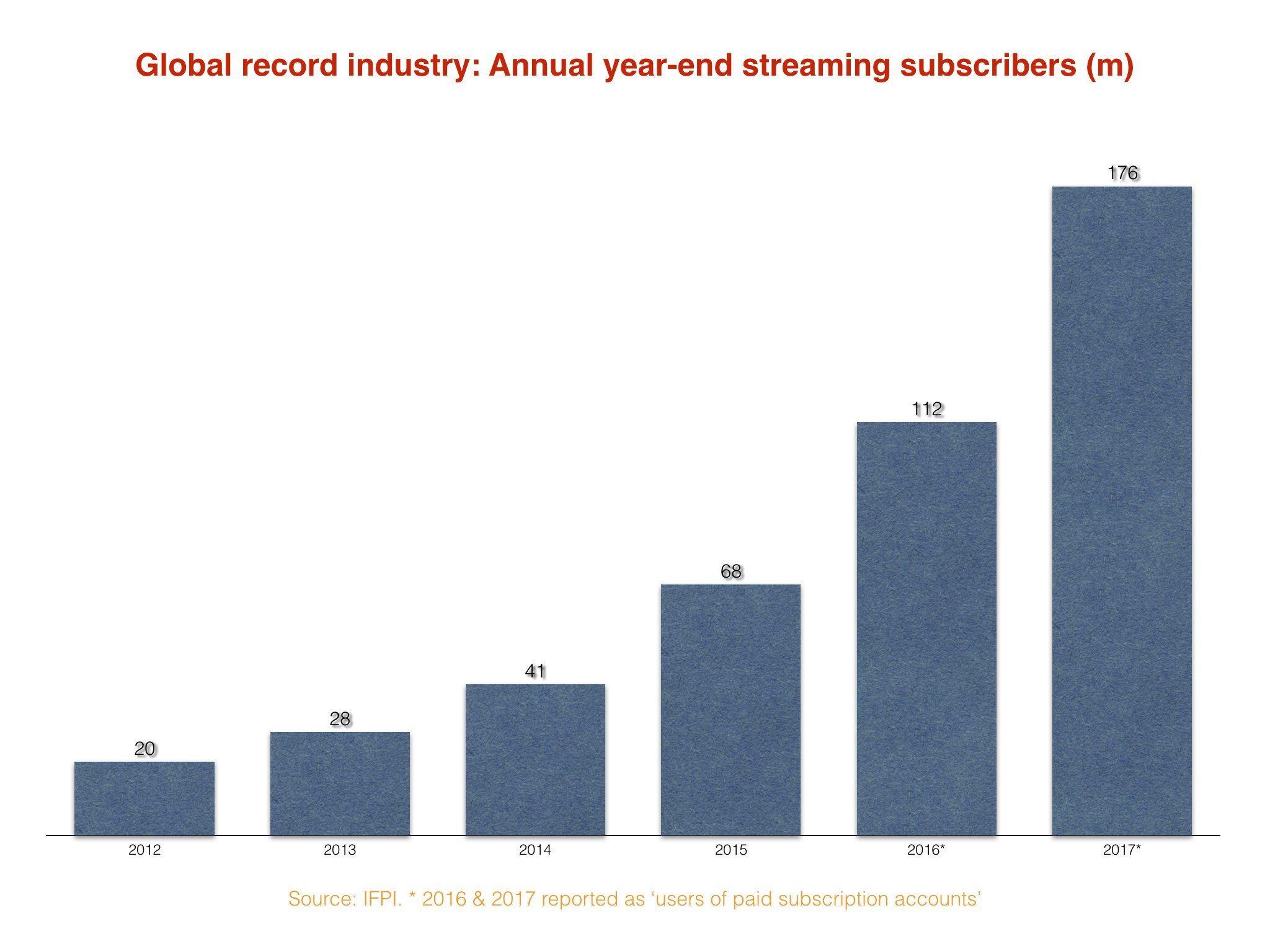

Of course, streaming at the heart of this good news – following a third consecutive year of growth driven by 176 million users of paid subscription accounts after fifteen years of continuous decline.

A noticeable slow-down in legacy format decline has also further strengthened these figures.

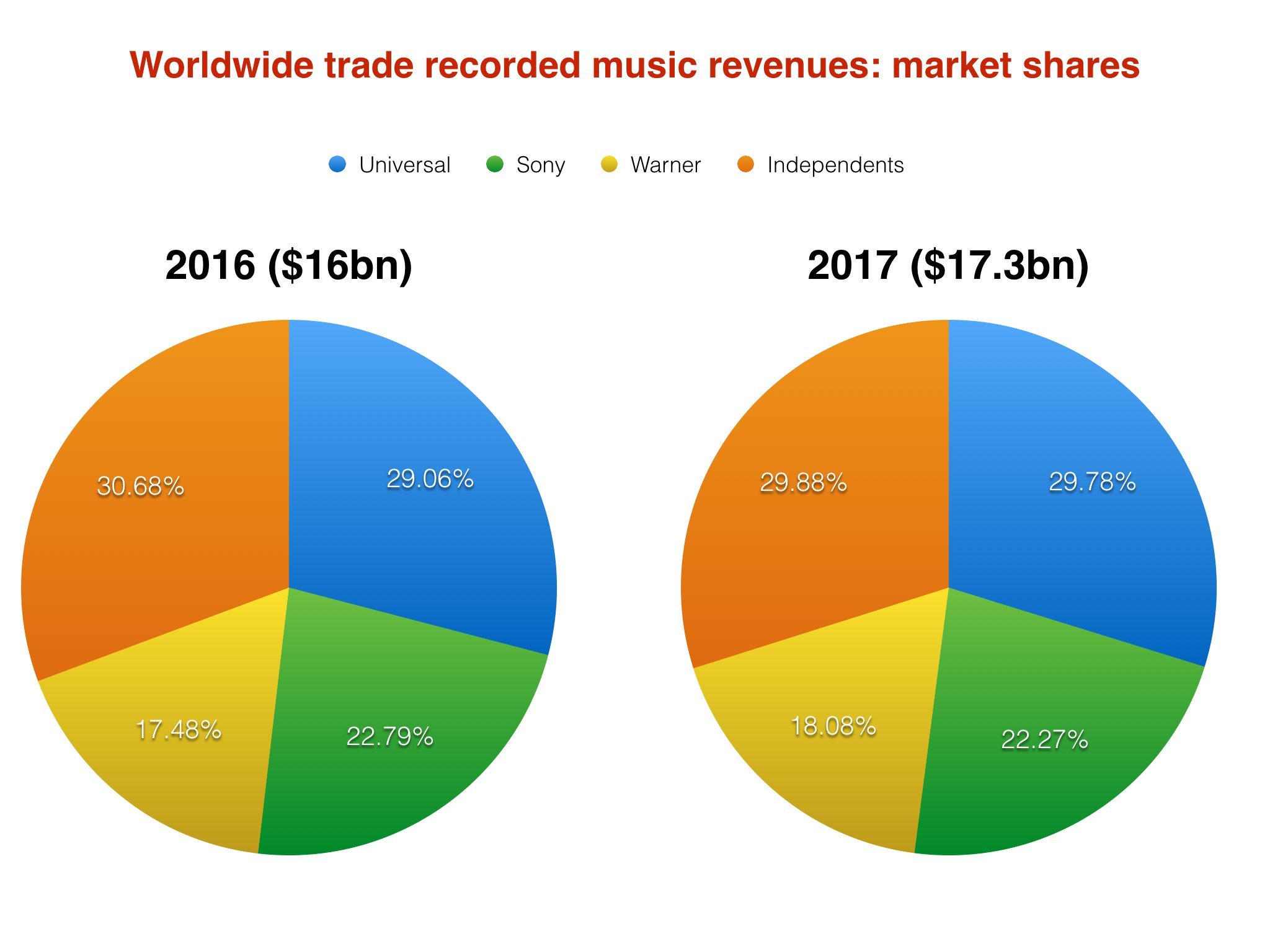

The major labels still collectively dominate market share but this is, of course, calculated on a distribution basis – meaning that any independent company distributed by a major label has their market share bundled into that of the major label.

This is just one way of measuring the market and we at WIN have long held that market share should be calculated on content and rights ownership, not merely on the route to market which as a service is interchangeable.

That is why we now publish our own annual WINTEL report which provides the most accurate figure of the independents’ true market share.

One of the key findings from the data published this month (via MBW’s analysis) is that even though Universal Music remained the largest major label group in 2017 with annual revenues of $5,152 – followed by Sony Music ($3,852) and Warner Music ($3,127) – independent artists and independent record companies combined represented nearly 30% of all revenues in 2017.

In total, the independent sector’s 2017 revenues stood at $5.2 billion – making the ‘long tail’ the largest market share owner of all.

I firmly believe that we are at the dawn of a golden age of music making and discovery, with access to music more democratized than ever – and the old gatekeepers all but gone.

The major labels still have an important part to play in the evolution and growth of our industry. Their global reach and well-resourced marketing and distribution capabilities mean that the commercial end of the market will still be well catered for as these multinational organisations continue to focus on the mass market, something they do very well.

“music fans have more choice and access to all types of music than ever before and are consuming music in a way that truly levels the global playing field.”

But what is becoming ever clearer is that music fans have more choice and access to all types of music than ever before and are consuming music in a way that truly levels the global playing field – try it, like it, share it. Simple.

Music discovery is both fun and rewarding, and takes no notice of origin or marketing budget.

As the independent artists numbers demonstrate, the long tail is no longer vanishingly thin, but is beginning to fatten up nicely as discovery drives consumption.

The growth of independent label services and distributors/aggregators has given content owners and creators more choice and more routes to market than ever before.

New business models have evolved to give more options beyond what we might call the ‘traditional’ record deal and there are now many more ways to fund, collaborate, access and reach audiences.

All this means, of course, that measuring the market in the future is going to get ever more complex. Even in this month’s new numbers, we are probably missing significant revenues and that trend will continue as new technologies drive innovation to a point where data capture will be ever more opaque.

And long may innovation thrive.

As markets around the world open and share their cultures and histories though music, the art and act of music making will become a truly global multi-cultural phenomenon.

Bring it on.

Music of different cultures, different languages, different instrumentation, different tonal origins will collide to create music of fascination. And it is highly likely that all of this will live happily in the long, ever-fattening tail.

Add to this the fact that the emerging markets are almost exclusively independent and you can see the future is bright for our sector.

“the independents operate in an environment that is becoming increasingly difficult to measure.”

As the largest market share producers in the world, the independents operate in an environment that is becoming increasingly difficult to measure, so it is incumbent on us as an industry to figure out new ways to accurately report an authentic overview of our global business.

Let’s ensure that we continue to look at our WHOLE industry when calculating our success in future and properly give credit where credit is due.

As is correctly pointed out by Mark Mulligan this month, “the rights side of the recorded music market is undergoing transformation, with (independent) artists the big revenue trend to surface in 2017”.

What is missing from the recent reports is the organic revenue that happens when an independent artist prints their own CDs and sells them at the merch table at a gig. This is a critical source of revenue for artists to live on while tour and generally these unit sales are not reported to services like Nielsen.

In the US, an independent disc manufacturer like Disc Makers is still making discs for independent artists, 40 million last year. Assume just half of those sold last year outside of traditional retail and at venue at an average price of $10 and there you have a couple hundred million dollars of missing revenues occurring in the industry.

Mulligan points out that independent artists were the biggest gainers in 2017, growing by 27.2% to reach $472 million in revenues.

Remarkably, the true market share of the global independent sector might well be higher than even the 30.3% (MIDiA) or 38.4% (WINTEL) figures quoted , as we know that data capture is incomplete and that many countries are not yet contributing to any market analysis.

When they do, the independent sector will be the big winners.Music Business Worldwide