Who wants to play a game of “Sorry, I Don’t Speak Finance”?

I’ll start!

Earlier today (February 20), Universal Music Groupannounced the $240 million acquisition of a 25.8% stake in Chord Music – a portfolio of around 60,000 songs (or, more accurately, cuts in songs), most of which were once owned by a sister-fund of Kobalt’s.

Chord owns stakes in a flurry of pop hits from the likes of Ryan Tedder and John Legend, as well as smash songs from The Weeknd, Lorde, and Diplo that were originally developed by Matt Pincus, Ron Perry, andCarianne Marshall at SONGS Music Publishing (before that catalog was sold to Kobalt in 2017).

As a result of the new deal, Chord Music’s assets (when their current distribution/administration deals expire) will become distributed via UMG’s Virgin Music Group and administered via Universal Music Publishing Group (UMPG).

However, this – UMG’s new quarter-ownership of a bundle of sweet music assets – is just part one of this story.

Part two is arguably much bigger.

And it’s at this point we get to play “Sorry, I Don’t Speak Finance”.

In a press release issued this afternoon, Boyd Muir, CFO and EVP of Universal Music Group, was quoted as saying that UMG’s investment in Chord “provides us with an efficient vehicle for future catalog acquisitions, without significant capital allocation through a combination of leverage and partner equity capital”.

Did you just press your “Sorry, I Don’t Speak Finance!” button?

If you did, congratulations! Here’s your prize: a translation of Muir’s quote that even a five-year-old could comprehend… “Universal Music Group is now able to buy more stuff without spending too much of its own money.”

You see, UMG only has one partner in Chord Music – and it’s a partner who isn’t afraid of recognizing the value of hit music by spending large sums on it.

“Universal Music Group is now able to buy more stuff without spending too much of its own money.”

Dundee Partners, aka the investment office of the Hendel family, now owns the other75%-ish of Chord Music… having teamed with UMG to buy out Dundee’s previous majority-partner in the fund, KKR.

In addition to soaking up the market share from Chord’s existing assets, Universal says that its new “long-term partnership” with Dundee will see the two companies “acquire additional catalogs via Chord in the future”.

Judging by Chord’s new setup, UMG will make its presence felt at the negotiating table for these acquisitions… but will only be expected to fund a minority piece of each deal (with the rest being funded by “partner equity capital”).

Here are three more key observations on today’s game-changing deal, and what it might mean for the wider industry…

1) Dundee Partners just became a real player in the music business

What ties together Chord Music, Kobalt Music Group, Partisan Records, music rights investment platform JKBX, AI music platform Boomy, the Broadway hit musical, Fela!, and Knitting Factory Entertainment?

All of them have received investment from the Hendel family, aka Dundee Partners.

Two generations of investors are behind Dundee: Father Stephen Hendel – the man whose money and determination pulled Fela! to broadway – and son Sam Hendel (pictured inset), who has led Dundee’s investments into the likes of Chord and JKBX.

To date, Dundee’s activity in the music business has been impactful, rather than blockbuster.

For example, Dundee has owned a minority stake in Kobalt Music Group following the latter company’s majority sale to Francisco Partners in 2022.

Today’s Chord announcement explodes the scale of Dundee’s investment in music.

The new deal, says UMG, values Chord Music at $1.85 billion (including debt). This means Dundee’s 75%-ish stake in Chord is worth… significantly more than a billion dollars.

Can you think of any other private families that are ‘all in’ on music rights to that kind of scale today?

2) Universal just ‘did a Tempo’. Will it get better results?

The Chord Music deal is the first time that Universal Music Group has partnered so publicly with outside finance to acquire music catalogs.

This is a highly significant development.

First of all, UMG has a strict internal policy RE: the catalog acquisitions it’s willing to make autonomously. On a March 2023 earnings call,Sir Lucian Grainge said in no uncertain terms: “UMG… is not in the passive rights business.”

Grainge was borderline dismissive of companies who bought income streams/fractional rights and then suffered from the “inability to acquire all the rights necessary to actively manage anything”.

“We see almost everything,” said Grainge of UMG’s view of assets for sale in the marketplace. “We pass on most of it.”

His point: Universal Music Group, as a rule, only buys rights that give it full control over the commercial exploitation of the music involved.

Problem is, that kind of stringency locks UMG out of acquiring lucrative and useful, but ultimately passive, assets in music. (For example: when it comes to long-term UMG artists looking to sell their future recorded music royalties.)

The Chord deal with Dundee Partners enables UMG to participate in this world of buying fractional rights for the first time – something that might help the company compete more aggressively for catalog offerings that don’t meet its core UMG acquisition criteria.

Another important point: UMG’s total spending on catalog acquisitions in recent years has shrunk.

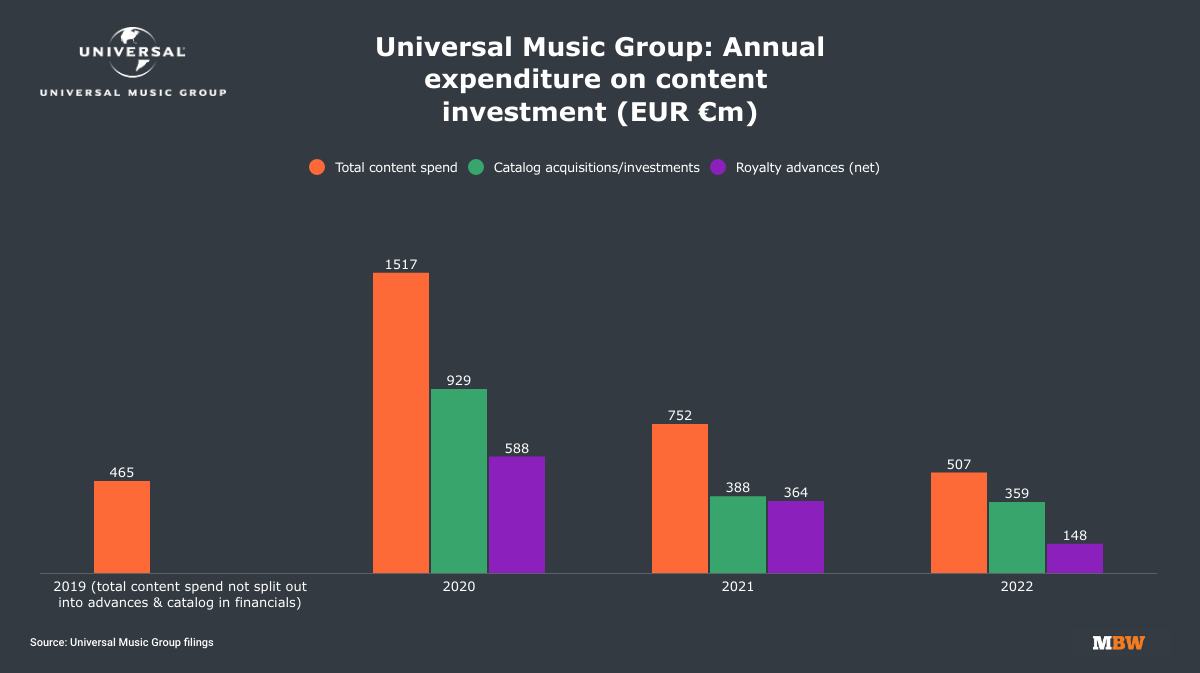

In 2022, UMG spent EUR€359 million on catalog music acquisitions, according to its financial records. That was around a third of the amount it spent on the category in 2020 (€929 million), a year when it paid a nine-figure sum for Bob Dylan’s publishing rights (see below).

Playing into this annual reduction in Universal’s catalog acquisition spending: The natural tension between UMG delivering cash to investors… and spending cash on catalogs.

As MBW has previously explained, since floating on the stock exchange in Amsterdam in September 2021, UMG has promised its investors a payment of at least 50% of its net income each year in dividends.

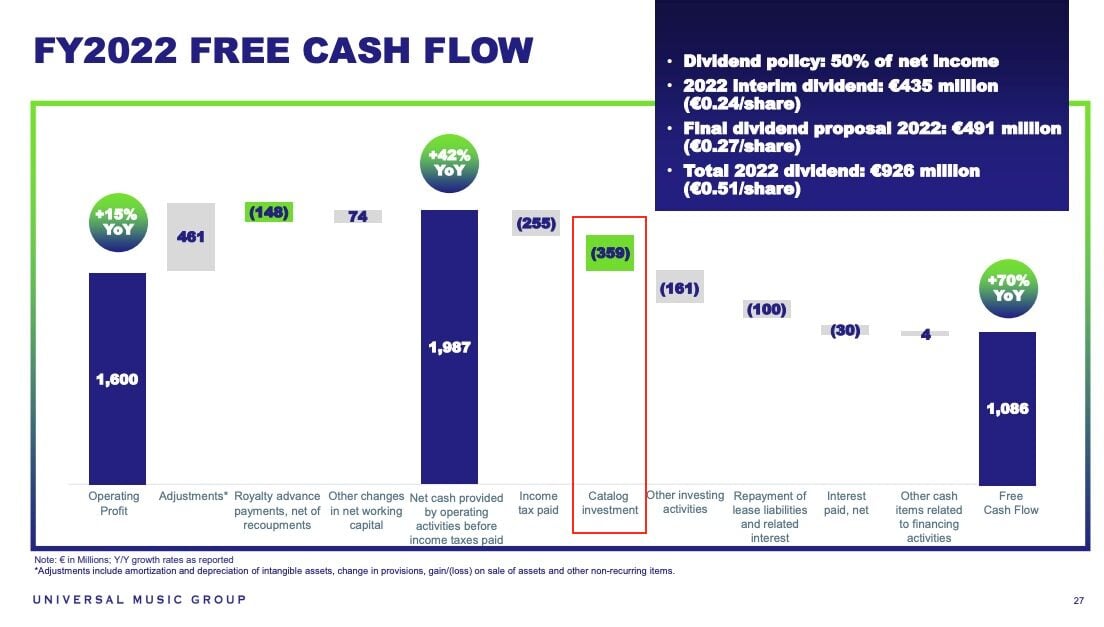

In 2022 (the last full year we have on record), UMG paid out a whopping EUR €926 billion in dividends to shareholders.

Spending large sums of cash on catalog acquisitions would negatively affect Universal’s Free Cash Flow (FCF), a source for the annual dividends the company pays its shareholders.

A slide showing UMG’s FCF in 2022, and the negative impact of €359m of catalog investment in the year (source: UMG 2022 annual report)

This idea gets especially interesting if Universal was ever fighting to acquire a huge, iconic music catalog – like Queen’s music rights, for example, which are still thought to be on the market for a $1 billion-plus price-tag.

Right now, to execute a deal that size, UMG would presumably have two choices: Spend a bunch of cash, reducing its FCF, or rack up a load of debt (complete with long-term interest payments).

UMG’s investment in Chord Music gives it a third option: So long as Dundee Partners is willing to majority-finance a catalog deal (even at a splashy multiple), UMG would only be on the hook for a minority of the price.

UMG would then benefit from the upside of being said catalog’s long-term distributor/administrator… and not having to watch that distribution/administrative market share go elsewhere in the industry.

(This logic could also apply when an artist or songwriter’s long-term licensing agreement with UMG is expiring, and the owner is looking to sell their catalog. UMG can now keep the distribution/administration market share if Chord acquires the asset.)

Universal Music Group isn’t the first major music company to see sense in partnering with outside finance for these reasons.

(Rumors of Tempo’s portfolio being on the block for a sale have circled the company in recent years.)

In 2022, Warner pulled a similar move again, this time partnering with BlackRock-backed Influence Media Partners, which struck a nine-figure deal with Enrique Iglesias at the end of 2023.

More recently, Kobalt Music Group (to date the publishing administrative publishing partner of Chord Music) announced in November that it had partnered with Morgan Stanley.

3) KKR bows out of music rights… again. Will it live to regret it… again?

Here’s a lesson in the language of Wall Street.

In October 2021, KKR issued a press release announcing Chord Music. At the time, Chord was majority-owned by KKR, minority-owned by Dundee Partners, and had just sealed a $1.1 billion acquisition of rights from a Kobalt fund.

The press release stated that the $1.1 billion deal “connects the works in the [Kobalt] Portfolio with long-term owners”.

Just twenty-seven months later, KKR has now sold up. “Long-term owners” indeed!

(In contrast, Dundee Partners, by doubling down on Chord, has arguably come good on the PR’s promise.)

Interestingly, this isn’t the first time KKR has jettisoned a collection of music rights.

Universal Music Group’s current market cap value on the Euronext is EUR €49.15 billion;

That is approximately 24-times the size of UMG’s EBITDA in 2022 (€2.03bn);

This 24-times multiple infers that BMG’s fair valuation today, based on its 2022 EBITDA, would be somewhere in the region of USD $4.9 billion.

Reminder: KKR sold 51% of BMG for around $1 billion eight years ago.

Also interesting: In the past few years, KKR and BMG have operated a joint fund to buy music assets. Acquisitions have included John Legend’s songbook and the “music interests” of ZZ Top. According to today’s press release on Chord Music, KKR now appears to have moved its assets from these deals into Chord… and sold them to Dundee/UMG.

So… will KKR regret selling its majority stake in Chord down the line, just as it likely regrets its premature exit from BMG?

That all depends on how bullish you’re feeling about the long-term value story ahead for premium music rights.

We’ve just witnessed a period of uncertainty at the blockbuster end of music’s catalog acquisition market (see: the story of Hipgnosis Songs Fund‘s share price) primarily caused by interest rates bouncing upwards.

Yet interestingly enough, after something of a chill wind in the big-money catalog acquisition game in H2 2022 and H1 2023, the past few months have seen the market’s heat rising:

A month later, that nine-figure Enrique Iglesias catalog sale to Influence Media Partners was announced;

Just last week, it was confirmed that Rod Stewart had sold his interests in his publishing catalog and recorded music, as well as some name and likeness rights, for around $100 million to Irving Azoff‘s Iconic Artists Group;

Rumors continue to bubble away out there about a major potential new catalog deal between Blackstone/Hipgnosis and Shakira;

And the Michael Jackson estate reportedly reached an agreement with Sony in recent weeks to sell the company a 50% stake in MJ’s song and recorded music portfolio for somewhere upwards of $600 million.

All of the purchasers in these deals – just like Dundee Partners and Chord Music – believe that the boundless revenue growth story for premium music rights has many more chapters to go.

If you asked any of these buyers if they think the likes of Spotify and YouTube Music should further increase their subscription prices in 2024?

I’m sure you could guess the answer.Music Business Worldwide