BMG just got significantly bigger.

That’s one take on yesterday’s news of a merger between Bertelsmann‘s music company and Concord.

The newly combined company will be 67% owned by Bertelsmann and carry the BMG brand, but sit above two entities: Concord Records and BMG Publishing.

As reported earlier, Bob Valentine, currently CEO of Concord, will become CEO of the new entity, with Thomas Coesfeld – currently CEO of BMG, and soon to be CEO of Bertelsmann – becoming its Chairman.

In their official confirmation of the merger, the companies didn’t disclose a valuation for either (i) Concord itself or (ii) the combined entity.

But they did give us some breadcrumbs. Here are a few quick thoughts on the deal, and its financial significance.

1) A combined BMG and Concord is worth around $15 billion. That’s big.

The run-up to this deal was marked by rumor and speculation about its commercial detail.

Bloomberg, which broke the news of talks in January, reported that Concord could be valued “as high as $7 billion.”

Billboard came out of the traps next, and was more conservative, suggesting the deal might value Concord at “more than $6.6 billion.”

My own well-placed sources suggest that the agreement gave Concord an enterprise value of $7.4 billion–$7.6 billion, and that the combined entity is now worth close to $15 billion.

When you look at the numbers BMG released today, this is no great surprise.

“if Concord and BMG each make up half of that $730 million figure this year, then a 20X multiple would get us to $14.6 billion.”

According to the official press release, BMG and Concord forecast that, combined, they will generate over $730 million in EBITDA this year.

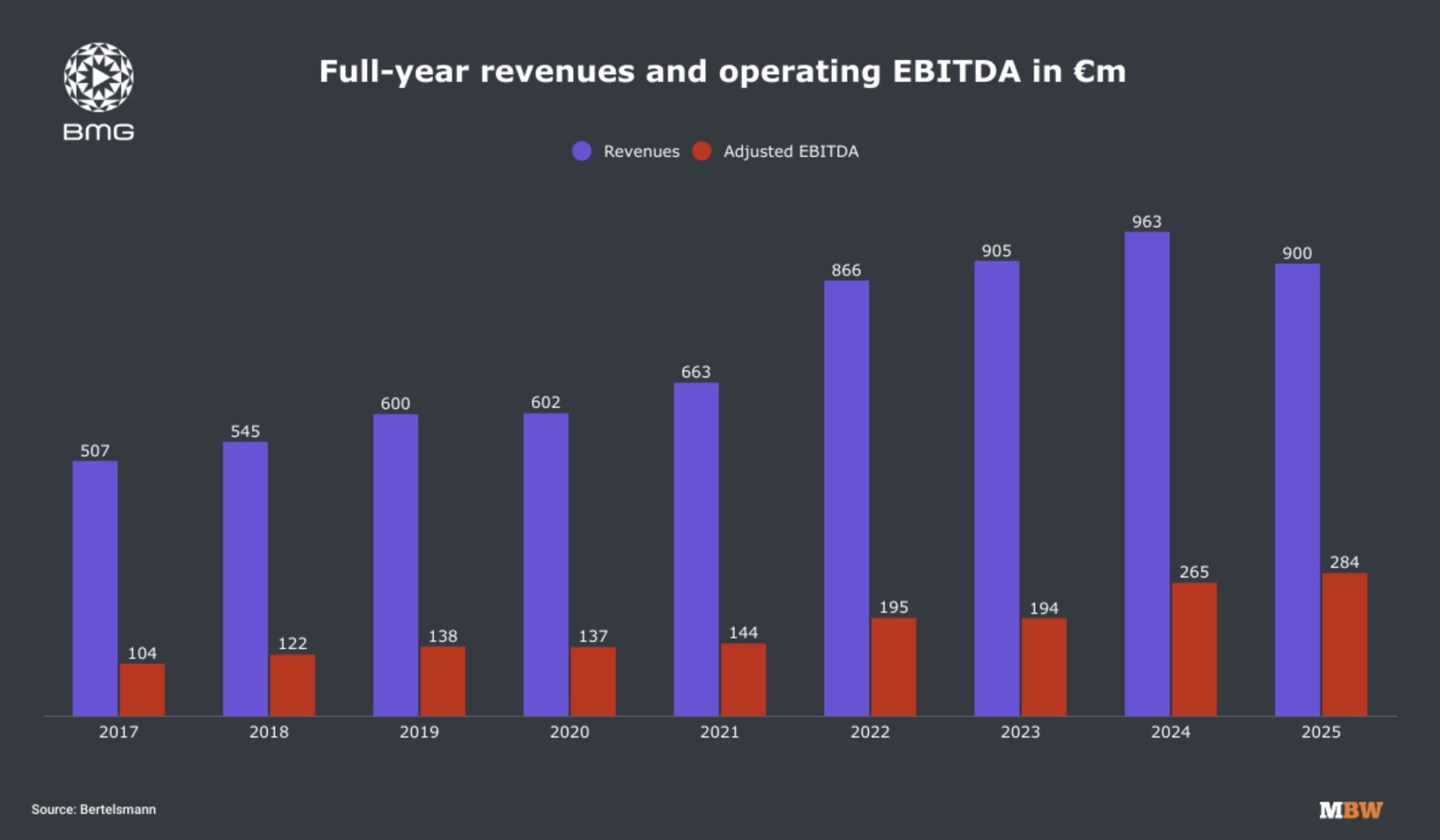

Sources close to the situation suggest that BMG and Concord’s profitability is “surprisingly similar” as things stand, and we already know BMG generated EUR €284 / USD $321M in adjusted EBITDA last year (see below).

So if Concord and BMG each make up half of that $730 million figure this year, then a 20X multiple would get us to $14.6 billion.

My sources suggest that (complete with the 20X multiple) is in the ballpark of what went down.

The combined company will be controlled by Bertelsmann, with investment management company Great Mountain Partners and its affiliates owning the other 33%.

Helping Great Mountain and those affiliates (including the Michigan Pension Fund) swallow a minority seat at the cap table: a $1.16 billion cash payment from Bertelsmann to sweeten the deal.

Most of the value of this ~$15 billion merger, therefore, seems wrapped up in a stock swap. But, in paper value terms, it’s still one of the biggest deals in music industry history.

Other big swingers that come to mind: a consortium led by Tencent swooped for 20% of UMG in 2020–2021, for around $7 billion (UMG was valued at approx. USD $37 billion at the time). Len Blavatnik acquired all of Warner Music Group for USD $3.3 billion in 2011, while other ten-figure deals, such as UMG’s acquisition of EMI Music (2012) and Sony‘s acquisition of EMI Music Publishing (2018), also warrant mention.

The mac-daddy probably remains Seagram buying PolyGram from Philips for over $10 billion in 1998 – 80% in cash – effectively creating the company we now know as Universal Music Group. Seagram later merged with Vivendi in an all-stock deal.

2) No, the ‘new’ BMG won’t be rivaling Warner Music Group for scale. Profitability? That’s another question.

As mentioned, the press release today noted a projected “pro forma EBITDA of over $730 million” for the combined BMG+Concord company.

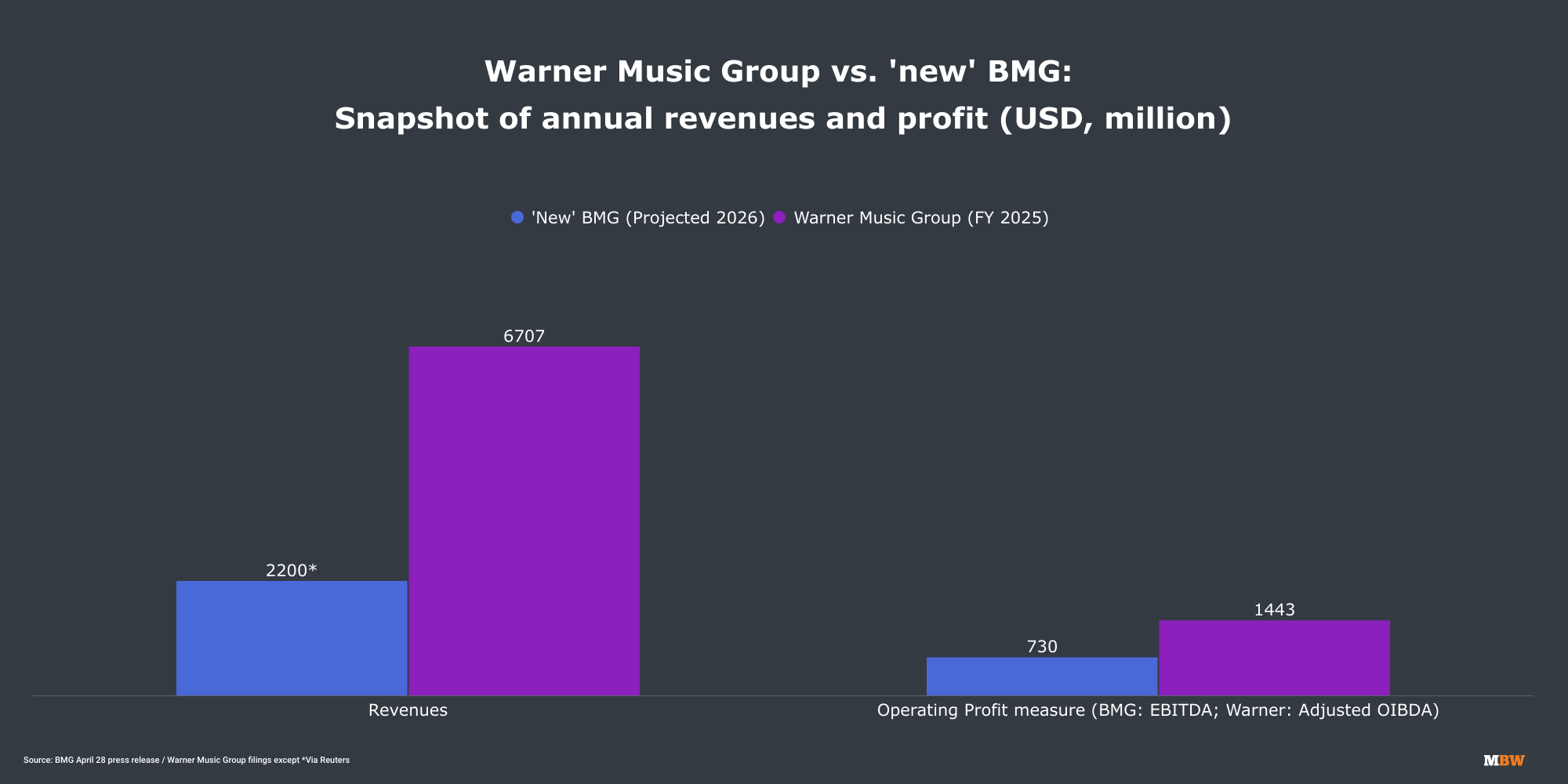

Reuters suggests this is expected to be achieved from an annual turnover of $2.2 billion, putting BMG/Concord’s EBITDA margin at 33%+.

Again, this fits with what we already know of BMG, whose profit margin under Thomas Coesfeld reached a record 32% in 2025.

Coesfeld told me in an interview set to publish shortly that he sees three types of music rights companies: (i) Distributors/administrators; (ii) Catalog owners; (iii) Hybrid music firms, who can use their operational power and reach to drive revenues for their catalog.

BMG and Concord are both in game (iii), he suggests, but have been unusually rigorous in keeping their profit margins high for shareholders. With further acquisitions, industry growth, and combined efficiencies ahead, that margin may yet creep higher.

“If Coesfeld and Valentine can achieve their aim – nearly doubling profit while maintaining strong 30%+ margins – expect public investors in major music companies to take note.”

The combined BMG+Concord is now comfortably the world’s fourth biggest music rights company. However, it won’t be challenging the world’s third biggest – Warner Music Group – for reach any time soon.

In its FY 2025, to end of September last year, WMG generated $6.71 billion in topline revenue – around three times the size of BMG+Concord’s expected revenue in 2026. (Worth noting: Some $835M of these WMG revenues came from ‘artist services and expanded-rights’ – areas that Coesfeld has deprioritized at BMG as he re-focuses the company on the “core” of recorded music and publishing.)

WMG’s preferred profitability metric – adjusted OIBDA (Operating Income Before Depreciation and Amortization) – stood at USD $1.44 billion in FY 2025, a margin of around 21.5%.

Eagle-eyed readers will have spotted that WMG’s annual profitability there ($1.44B) isn’t far away from the yearly EBITDA number that BMG+Concord says it is now targeting in the “mid-term”: $1.2 billion.

WMG will almost certainly also grow its bottom line in that “mid-term” period too, of course.

But if Coesfeld and Valentine can achieve their aim – nearly doubling profit while maintaining strong 30%+ margins – expect public investors in major music companies to take note.

3) BMG is proud of its direct digital distribution strategy. Will it bring the same to Concord?

Today’s story isn’t just about who ‘acquired’ Concord – it’s about who did not.

Universal Music Group has long been Concord’s exclusive global distributor for recorded music.

Yet on this occasion, UMG declined to acquire Concord – potentially wary of regulatory scrutiny following a bruising ride from the European Commission over its Downtown buy.

There are advantages to distributing via UMG for Concord: UMG’s global infrastructure, its platform-level negotiating leverage, and its access to, for example, Spotify marketing tools represent strong additive value.

“Don’t be surprised to see BMG now migrate Concord’s digital distribution onto its own direct infrastructure over time – replicating the margin-boosting playbook.”

Yet one of Thomas Coesfeld’s first major moves as BMG’s CEO, back in late 2023, was to end the company’s long-running distribution deal with Warner Music Group/ADA and take streaming distribution in-house, going direct with Spotify and Apple Music.

The results have been notable and have played a material role in BMG’s EBITDA margin hitting that record 32% in FY 2025.

Don’t be surprised to see BMG now migrate Concord’s digital distribution onto its own direct infrastructure over time – replicating the margin-boosting playbook.

Physical distribution, though, is a different matter.

For Concord’s overwhelmingly catalog-heavy repertoire – some 85% of its revenue derives from catalog, per Valentine’s previous disclosure – vinyl, CD, etc. is a vital revenue engine.

BMG already runs its physical recorded music business through Universal. I now expect that relationship to deepen, rather than dissolve.Music Business Worldwide